{kind=link}

DISCLAIMER: This isn’t Funding recommendation. PLEASE DO YOUR OWN RESEARCH !!!!

Lots has occurred since I printed my Rocket Web write-up from the top of January. Simply as a refresher: I discovered Rocket Web fascinating, regardless of some Governance points because the “sum of the half” worth was considerably greater than the share worth again then and that it supplied some related & discounted publicity to Elon’s SpaceX IPO.

However earlier than we begin, I’d advocate to click on on the next hyperlink and get David Bowie’s Area Oddity as a pleasant background sound for studying this put up:

David Bowie – Area Oddity (Official Video)

As I write, SpaceX has simply launched its S-1 filing and plans to go public on June tenth. That is what I wrote again then:

My time horizon for this may be both the (Rocket) AGM or the precise SpaceX IPO. On Polymarket, the percentages are 60% for an IPO earlier than finish of Q3 2026

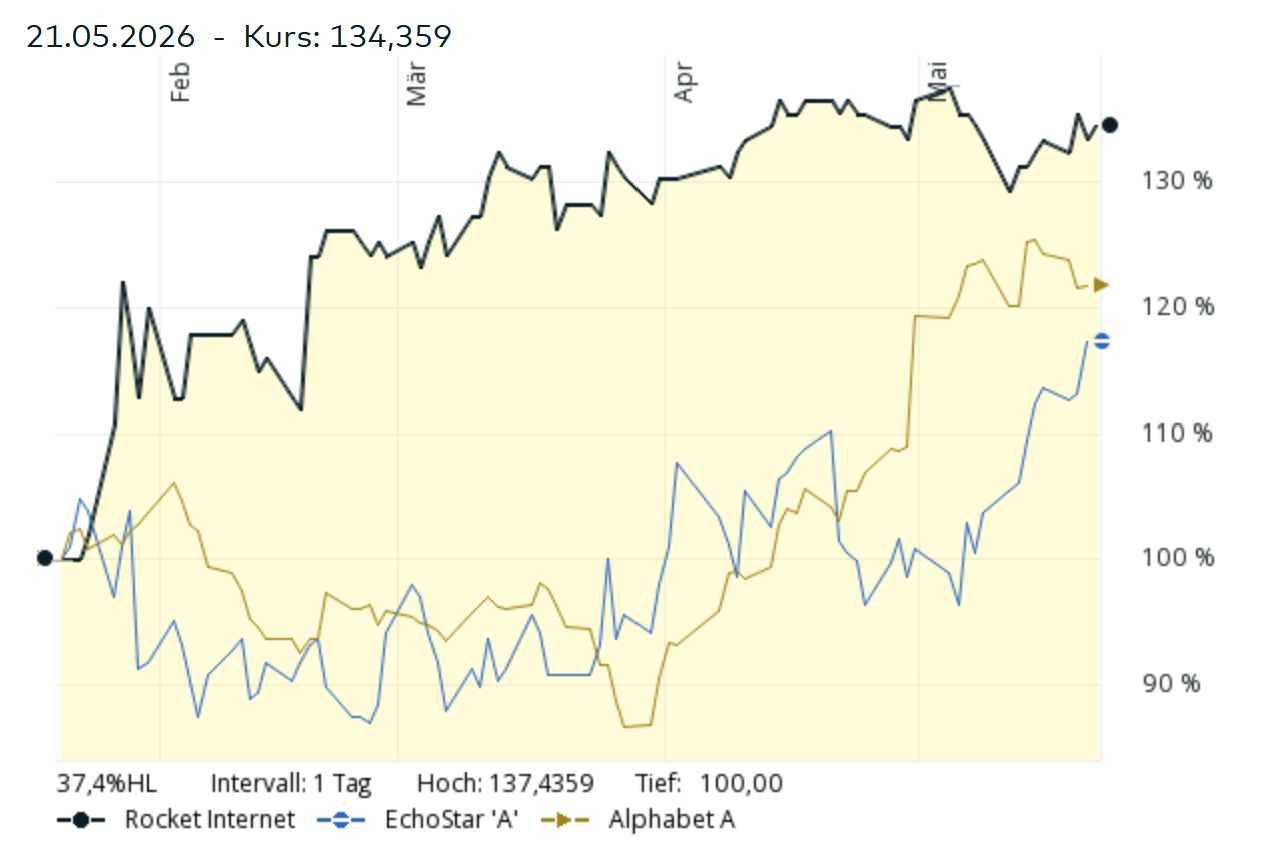

In contrast with two different “SpaceX Proxies” that I discussed, EchoStar & Alphabet, Rocket truly did fairly OK if we have a look at the chart:

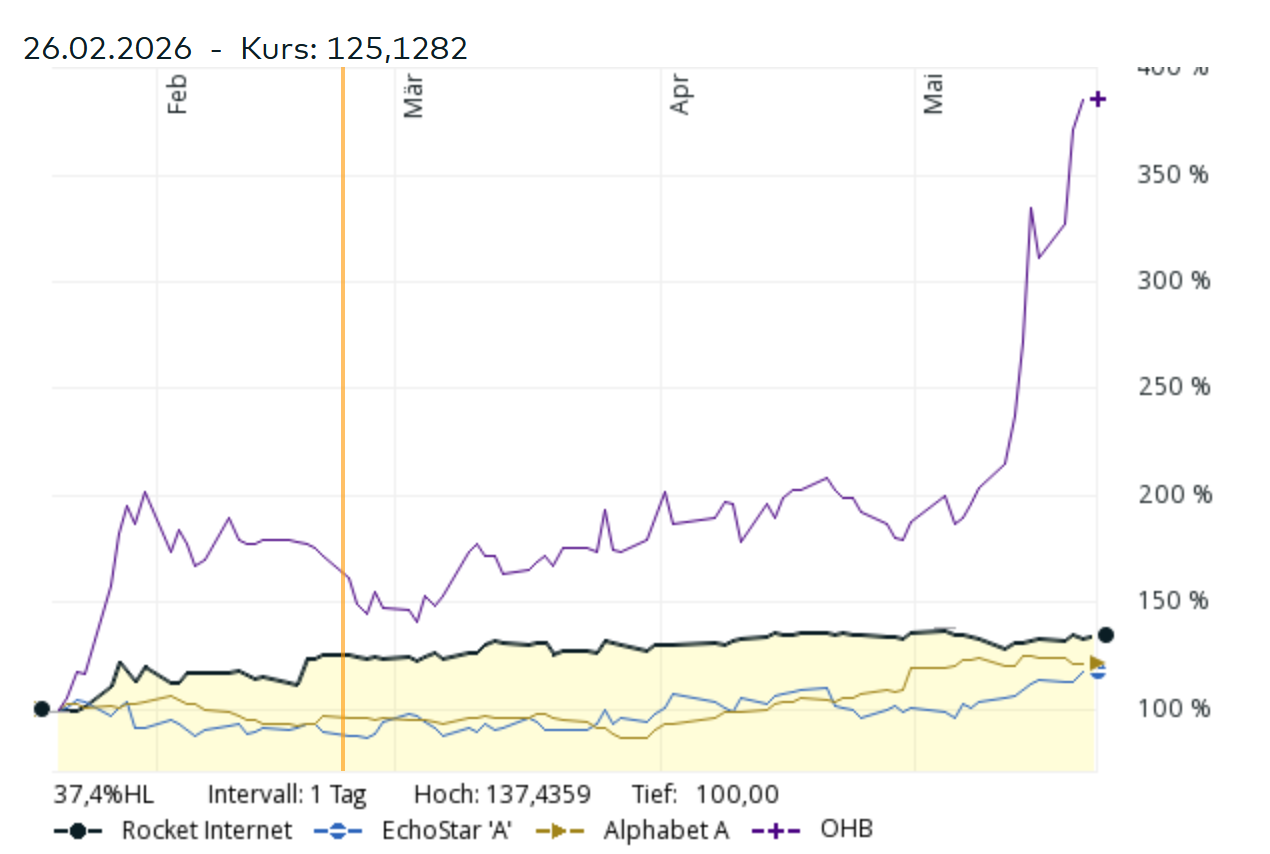

The actual Area Celebrity: OHB SE

Nevertheless, the true “Efficiency Rocket” would have been one other German inventory referred to as OHB:

OHB, a German/Bremen primarily based Satellite tv for pc producer went parabolic regardless of having a extremely small free float after KKR acquired a good portion of the minority free float at 44 EUR in 2023. Initially they needed to delist however then stored the itemizing.

The primary cause for this enhance appears to be that OHB is included in a very talked-about ETF referred to as Tema Area Innovators ETF with the nice Ticker NASA.

This ETF is among the quickest rising ETFs ever and presently has a 5% allocation in OHB. At round 1,4 bn AUM, that’s round 60 mn EUR in OHB. As many of the OHB shares are held by the founding Fuchs household and KKR (collectively ~94%) and a few specialised “Squeeze out” gamers, there appears to be a reasonably laborious squeeze on the few remaining shares.

I additionally guess that you just can’t brief OHB shares. Operationally, OHB has been doing okayish, however nothing that will justify a 130x P/E.

In any case, it is a monster deal for KKR who (clearly) plan to exit whereas its “sizzling”. I’m fairly certain that after that exit, OHB shall be a kind of “Christmas Tree” charts that we all know from the Covid occasions.

Again to SpaceX

Elon appears to focus on a valuation of 1,75 tn USD, that will be the higher vary of what I assumed in my January sum-of-the half valuation. Nevertheless, “previous” SpaceX shareholders from the start of the 12 months have been diluted by ~20% after the “merger” of SpaceX with XAi, so we’ve got to take this under consideration.

I’m certain that Matt Levine will write and say a lot smarter issues than I do concerning the SpaceX IPO, so listed below are just a few observations:

- The S1 prospectus comprises some very nice photos of rockets

- There are already loads of write-ups & observations about a number of facets of SpaceX. A reasonably good thread may be discovered as an example on Bluesky.

- Total, SpaceX is clearly rather more resembling a large “Elon Enterprise Fund” than a traditional firm. I believe I learn this in one in every of Matt Levine’s newsletters about Tesla. Elon has assembled a comparatively loosely related group of corporations (XA, Twitter, SpaceX, Starlink, possibly Cursor) with which he can roughly credibly leap on any new hype that may come his manner.

Just like the VC giants Sequoia or A16Z, he has two skills: To lift funding and to draw (a sure sort) of tech folks with which he can at the very least create the looks of using the following huge factor.

If Ai hits a brick wall, Elon finds one thing else like possibly Quantum computing or he’ll merge Neuralink into SpaceX or turn into the No 1 in weight problems tablets.

His hardcore followers aren’t in search of earnings however to trip the following hype

- Lots has been already stated concerning the “whole Addressable Market” figures from the deck which equal the US GDP.

The beauty of each, the socalled “Area financial system” and in addition AI is, that each in the mean time appear to have indefinite TAMs. Mathematically, even a small slice of one thing indefinite is price an indefinite sum of money.

In order that’s clearly significantly better than one thing like earth certain EVs the place there’s a clear ceiling or humanoid robots that simply don’t work and the place the Chinese language are clearly significantly better.

I’m fairly certain, Cathy Wooden or somebody related will provide you with an “evaluation” that SpaceX is price 100X from wherever it’s buying and selling.

- A pleasant contrarian take may be discovered on the “Wertegang” Substack with the good title : SpaceX is a Zero. Right here, my pal Dirk argues that the SciFi bestseller “The three physique drawback” clearly reveals that reaching to the celebrities is fairly dangerous from a cosmic perspective (Darkish Forrest idea). However I’m fairly certain that if wanted, Elon may even promise to fabricate Pocket Universes in one in every of his Gigafactories.

- What I’m actually interested in is, if Elon manages to essentially hype two corporations, Tesla and SpaceX on the similar time. Additionally, how will the standard “Elon retail hardcore supporter” react ? If he/she is an actual Elon fan, he/she can have all of their cash already in Tesla (plus possibly some extra). However after all, they need to have SpaceX publicity, too. So will they promote their Tesla shares to get a 50/50 allocation ? I believe this shall be fascinating to watch.

Anyway, the SpaceX IPO is nice monetary leisure and may solely be topped by an OpenAI IPO in autumn.

Rocket Web Replace

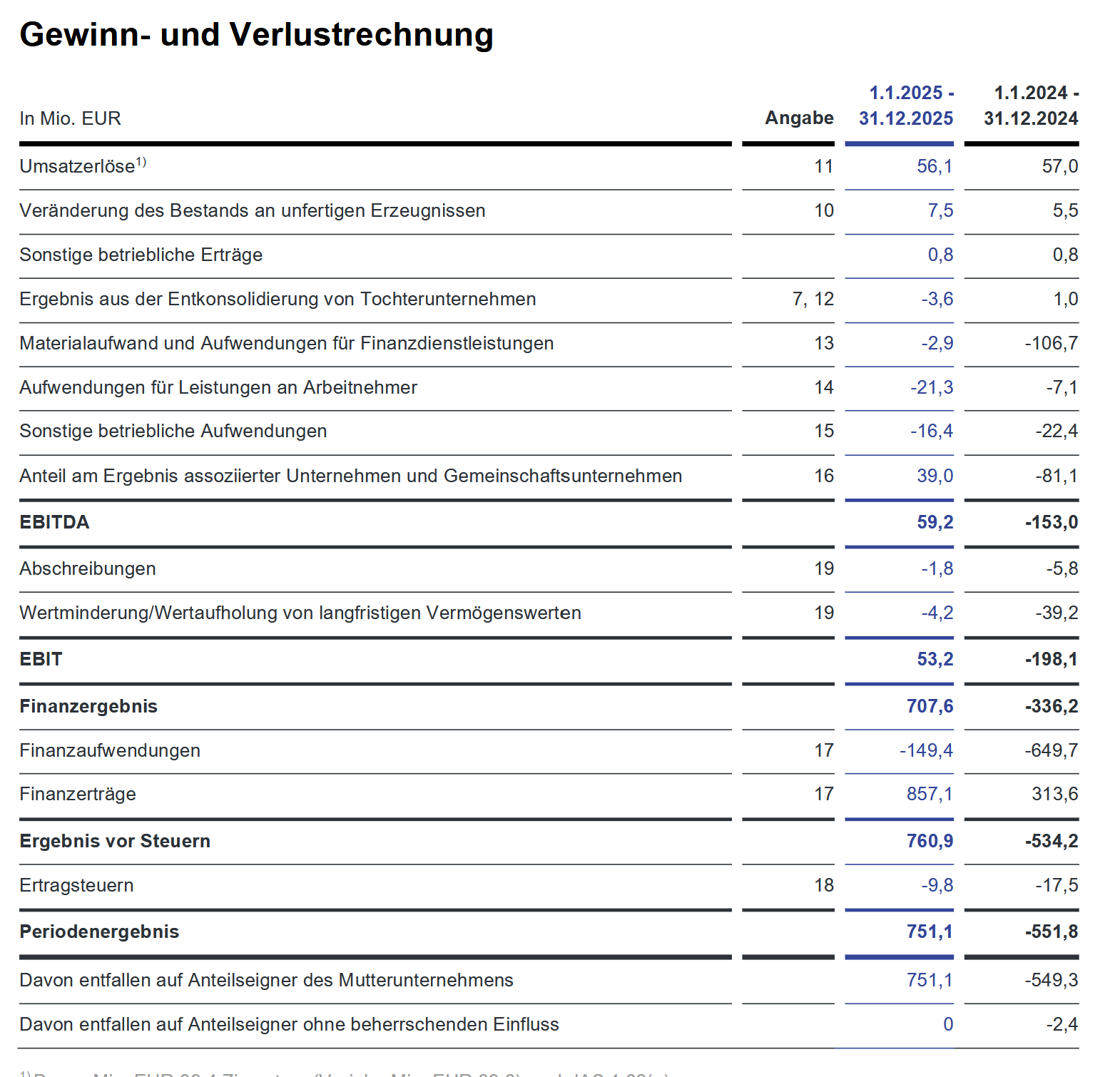

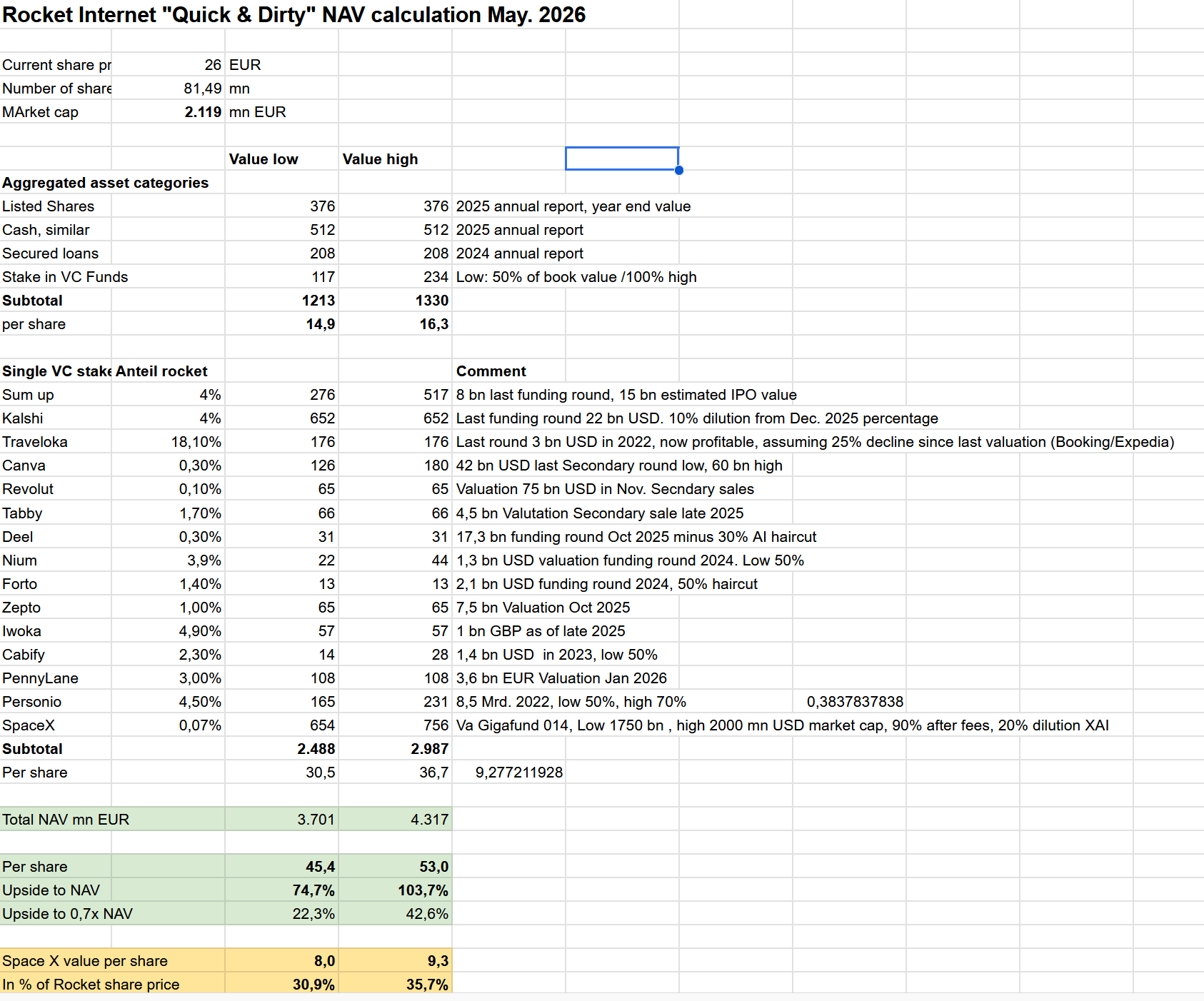

Within the meantime, Rocket Web has “printed” its 2025 annual report. Curiously they did revaulue their participations upwards to a sure extent. After a lack of -550 mn EUR in 2024, they now present a revenue of 750 mn EUR. It appears that evidently the letter from Scherzer AG to the auditors did have some results.

If I’d be within the Microcap Inventory promotion sport, I’d possibly put up one thing like: “Hidden Perfromance Rocket buying and selling under NAV at 3x P/E ratio”, however economically the proven revenue is fairly meaningless.

On the adverse facet, there shall be no giant money distribution and Rocket appears to mean to make the corporate even much less clear going ahead.

In any case, I up to date my valuation sheet, together with some “bug fixes”. Once more, it is a fast and soiled train and positively not funding recommendation !!!

Right here is the brand new sheet:

The primary modifications that I made have been some haircuts on Software program corporations andTraveloka and adjusting Kalshi and SpaceX for the newest values. For SpaceX I incorporatedthe 20% dilution from XAi and a brand new vary of 1750 to 2000 mn USD as valuation. For Kalshi I used the 22 bn valuation and implying an additional dilution of 10% from the YE 2025 quantity.

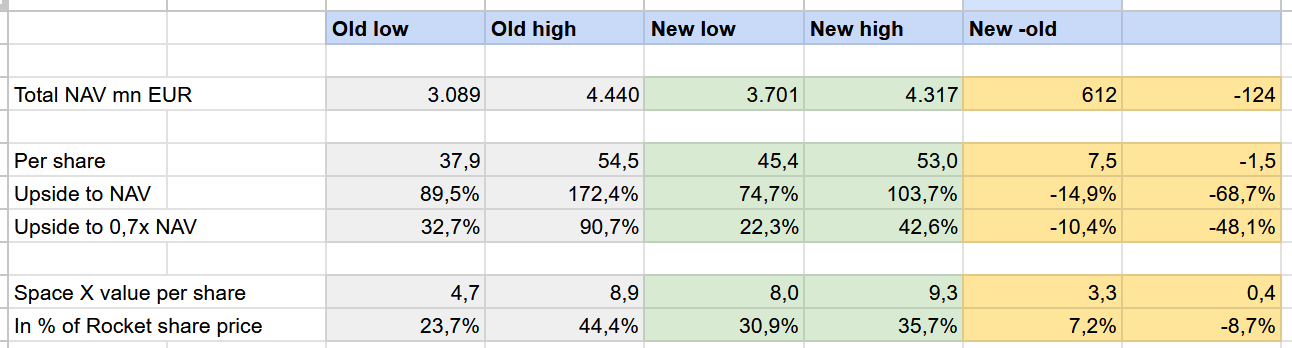

It is a fast comparability between my previous and the brand new train:

We will see that the Upside NAV is kind of the identical at 53 EUR per share vs. 54,5EUR regardless of the “haircuts” utilized to Software program, however the draw back valuation is singinifcantly greater, primarily due to the anticipated valuation of SpaceX at theIPO and the latest Kalshi spherical which was solely a hearsay in January.

The upside to the NAV is after all decrease, because the shares gained ~+30% because the write-up.

As talked about to start with, I’ll hold the shares till the IPO hoping for some extra irrational exuberance across the SpaceX IPO. Except I’ll change my thoughts earlier 😉