{kind=link}

Life occurs, and typically even essentially the most accountable folks can take a success to their credit score, by no actual fault of their very own.

You’ll be able to funds correctly, pay your payments on time, and nonetheless end up in hassle.

My buddy is an ideal instance. She had her bank card set to autopay, pondering every little thing was beneath management. However the system tried to drag cash from the unsuitable account. When the cost failed, her bank card firm instantly shut the account down and reported a missed cost to the credit score bureaus. Her credit score rating dropped, quick—and all due to a glitch she didn’t see coming and had no management over.

Tales like hers are extra widespread than you would possibly assume. And if it’s occurred to you, know this: you’re not alone, and also you’re not with out choices.

As a private finance author with over a decade of expertise, I’ve seen how simply credit score issues can sneak up—and how one can bounce again .

In immediately’s submit, I’ll stroll you thru how you can:

- Perceive what occurred to your credit score

- Take motion to cease additional harm

- Rebuild your rating with sensible, doable steps

Let’s take the stress out of the unknown and change it with a transparent plan to maneuver ahead.

Understanding the Affect of a Credit score Setback

Credit score setbacks can sneak up in on a regular basis life. You would possibly miss a cost, carry a excessive stability, or have a bank card closed—typically with out warning. These widespread points can damage your credit score rating shortly.

Even one missed cost can keep in your report for years. A closed account can shrink your out there credit score, elevating your utilization ratio. And excessive balances? They make you look riskier to lenders.

How Your Credit score Rating Is Calculated

To know the potential harm, it helps to know the way your credit score rating is constructed:

- Cost Historical past – Do you pay on time? (35% of your rating)

- Credit score Utilization – How a lot of your credit score are you utilizing? (30%)

- Size of Credit score Historical past – How lengthy have your accounts been open? (15%)

- Credit score Combine – Do you employ each bank cards and loans? (10%)

- New Credit score – Have you ever utilized for lots of latest credit score not too long ago? (10%)

When one thing goes unsuitable—like a missed cost or a closed account—it may well hit a number of areas directly.

Your credit score rating displays how dangerous you might be to lenders. One misstep can ship the unsuitable message.

The Domino Impact on Your Monetary Life

A credit score setback isn’t only a quantity. It might result in:

- Larger rates of interest on bank cards or loans

- Mortgage functions getting denied

- Decrease credit score limits in your present playing cards

And the consequences aren’t simply monetary. Many individuals really feel embarrassed or anxious, even when the problem wasn’t their fault. It’s simple to lose confidence when your rating drops.

However the excellent news is that understanding the impression is step one in taking again management.

Actual-Life Instance: When Autopay Goes Unsuitable

Auto-pay is usually a useful gizmo, when it really works. However when it fails, the harm could be fast and painful.

Take the instance of my buddy earlier, autopay didn’t work appropriately and her credit score rating took a tough hit in additional methods than one—all with out warning and thru no fault of her personal.

Sadly, she’s not alone. One Reddit person shared an identical story. That they had loads of cash of their checking account, however Goal claimed a cost was returned as a consequence of “non-sufficient funds.” Later, Goal mentioned the account “didn’t exist.” The identical financial institution information was used later for a profitable cost, and their financial institution confirmed no cost was even tried the primary time. Nonetheless, Goal shut down the account and reported it to the credit score bureaus—with out a lot as a heads-up.

“Due to the returned cost that was Goal’s personal fault, they’re cancelling my account totally and reporting it to credit score bureaus. Not a cellphone name or any ‘warning’ and it was their very own mistake.” – Reddit person

These tales spotlight simply how simply technical glitches can turn out to be monetary disasters. When methods fail, the fallout lands in your credit score report—not on the corporate that made the error.

Fast Steps to Take After a Credit score Setback

A drop in your credit score rating can really feel overwhelming. However the sooner you act, the extra management you’ll regain. Right here’s the place to begin:

Assessment Your Credit score Experiences

Your first step is to determine precisely what modified. Get a duplicate of your credit score report from all three main bureaus—Experian, Equifax, and TransUnion. You’ll be able to request them totally free yearly from AnnualCreditReport.com.

Search for:

- Missed or late funds

- Closed accounts

- New accounts or exercise you don’t acknowledge

It’s also possible to use free instruments like Credit score Karma to maintain tabs in your rating and get alerts when one thing adjustments. It received’t present every little thing, however it’s nice for recognizing purple flags quick.

Dispute Any Errors

In the event you see one thing unsuitable, take motion. Dispute errors straight with the credit score bureau on-line or by mail. The Shopper Monetary Safety Bureau (CFPB) gives an in depth information right here: Learn how to dispute an error in your credit score report.

Right here’s what you’ll want:

- A brief, clear rationalization of the error

- Copies of any supporting paperwork (e.g., financial institution statements or emails)

- Screenshots or proof if the problem was a technical glitch

Preserve copies of all communication and comply with up in the event you don’t hear again in 30 days.

Contact Collectors Straight

If a creditor reported the issue, don’t hesitate to contact them. You could possibly:

- Negotiate a cost plan

- Request a goodwill adjustment (particularly for a one-time difficulty)

Be trustworthy and calm. Clarify what occurred, particularly if it wasn’t your fault. Many collectors are keen to work with prospects who attain out.

“You’ll be able to’t repair what you don’t face. Begin small—one name or one report at a time—and momentum will construct.”

Methods to Rebuild Your Credit score

As soon as you determine what occurred to mess together with your credit score, it’s time to take motion to rebuild your credit score. Whereas we’d all like to quickly repair every little thing, the reality is gradual and regular is what works. With constant effort and a wise plan, you possibly can increase your rating and regain monetary confidence.

Construct a Constructive Cost Historical past

Since Cost historical past makes up the most important a part of your credit score rating, it is a good spot to focus first.

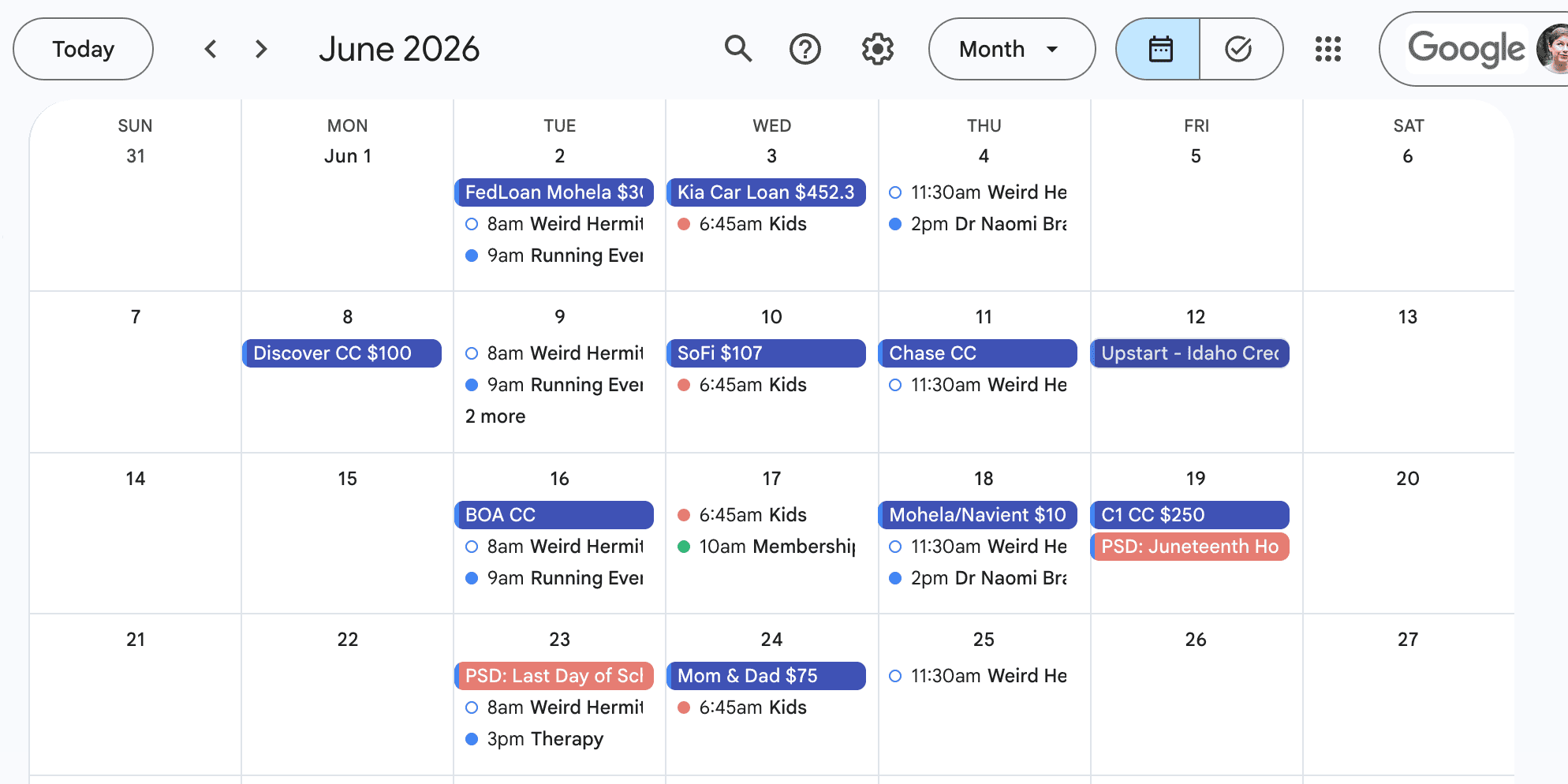

- Arrange cost reminders in your calendar or budgeting app. I love to do recurring occasions in my calendar and add a test emoji when it’s been paid:

- Use autopay correctly, and double-check your account hyperlinks to keep away from previous points. Personally I wish to automate financial savings, however maintain debt reimbursement pretty guide so I keep on prime of every little thing.

- Take into account secured bank cards in case your present accounts are restricted.These playing cards are designed that will help you construct/rebuild credit score, not entice you in charges. Simply remember to pay the stability in full every month.

Handle Your Credit score Utilization

Attempt to use lower than 30% of your out there credit score. Decrease is healthier.

In case your credit score limits have been decreased as a result of setback, don’t panic. One sensible transfer: name your bank card firm and ask them to revive your outdated restrict. Clarify what occurred. In the event you’ve resolved the problem and your document was strong earlier than, they might say sure.

The worst they’ll do is say no, and also you’ll nonetheless have taken a step to advocate for your self. Even when that doesn’t work there are different steps you possibly can take:

- Pay down excessive balances strategically (begin with the cardboard closest to its restrict).

- If attainable look right into a credit score consolidation mortgage, even when the rate of interest is excessive, comparable to 15% that’s doubtless nonetheless decrease than you present bank card rates of interest

- Take into account a stability switch to assist pay down balances quicker – however be cautious whereas many of those will supply 0% curiosity, in the event you don’t repay the stability by the top of the promotional window, the excessive rate of interest could be retroactive. Ensure you absolutely perceive the phrases earlier than doing a 0% stability switch.

Instruments and Sources to Help in Credit score Restoration

Rebuilding your credit score is simpler once you’ve acquired the appropriate instruments. These sources can assist you observe your progress, keep organized, and continue to learn as you go.

Credit score Monitoring Companies

Holding tabs in your credit score is important, particularly after a setback. These instruments allow you to catch points early and watch your rating enhance over time:

- Credit score Karma – Free credit score rating monitoring, alerts, and customized ideas.

- Experian – Provides real-time rating monitoring and the power to spice up your rating utilizing on-time utility and streaming funds.

Many of those companies can even warn you to new accounts or adjustments to your credit score report.

Budgeting Instruments

Sturdy cash administration helps credit score restoration. These instruments enable you to plan your spending and ensure payments receives a commission on time:

- YNAB (You Want a Funds) – A proactive budgeting software that helps you give each greenback a job. Nice for staying on prime of funds.

- Rocket Cash – Helps you discover and cancel unused subscriptions, observe spending, and set monetary targets.

Utilizing a budgeting app takes the guesswork out of staying on prime of payments, particularly when life will get busy.

Stopping Future Credit score Setbacks

When you’ve began rebuilding, the aim is to remain on strong floor. Just a few sensible habits can defend your progress and enable you to keep away from surprises down the highway.

Do Common Monetary Examine-Ups

Identical to your well being, your funds want common check-ins. Put aside time every week to overview:

- Your financial institution and bank card accounts

- Upcoming invoice due dates

- Any adjustments to your credit score report

One easy software: a private finance calendar. Mark all of your invoice due dates, paydays, and auto-draft expenses. You should use a paper calendar, Google Calendar, or a budgeting app. This makes it simple to remain forward of deadlines and keep away from missed funds.

It’s also possible to set reminders for quarterly opinions—like checking your credit score studies or rebalancing your funds.

Often Requested Questions

How lengthy does it take to rebuild credit score?

It relies on your place to begin and the way constant you might be. In the event you take regular steps, like paying payments on time and reducing bank card balances, you would possibly see enchancment in a couple of months. However rebuilding absolutely can take 12 to 24 months or extra, particularly after critical setbacks.

Be mindful: credit score restore is a marathon, not a dash. Deal with progress, not perfection.

Can closed accounts be faraway from credit score studies?

Not often. If the data is correct, closed accounts will keep in your credit score report for:

- 7 years for unfavourable accounts (like missed funds)

- 10 years for optimistic, paid-off accounts

Nonetheless, if the account was closed in error or contains incorrect info, you possibly can dispute it with the credit score bureaus.

Is it higher to repay debt or lower your expenses first?

Ideally, do each, however it relies on your scenario. Begin by constructing an emergency fund (even $500 helps) so that you don’t depend on credit score for shock bills. Then deal with high-interest debt, like bank cards.

Use a technique just like the debt snowball (smallest stability first), debt avalanche (highest curiosity first), or my favourite the debt nor’easter to make regular progress.

Conclusion: Empowering Your self for Monetary Resilience

Credit score setbacks can occur to anybody, even essentially the most cautious amongst us. However what issues most is the way you reply.

Let’s recap the steps you possibly can take:

- Perceive what occurred by reviewing your credit score studies and figuring out the problem.

- Take fast motion by disputing errors and contacting collectors straight.

- Rebuild your credit score with on-time funds, low credit score utilization, and sensible credit score use.

- Use the appropriate instruments like credit score monitoring apps, budgeting platforms, and academic sources.

- Keep proactive with common monetary check-ups and a dedication to studying.

The highway again would possibly really feel lengthy, however every sensible step you’re taking builds momentum. And each cost, each corrected error, each greenback saved is proof that you just’re shifting ahead.

Having navigated my very own monetary challenges, I understand how powerful it may be, however I additionally know the liberty and confidence that include taking management.

You’ve acquired this.