{kind=link}

In the event you’re at present the proud proprietor of a mortgage, you’ve undoubtedly heard of a cash-out refinance, one which permits you to faucet into your property fairness.

They have been fairly widespread throughout the early 2000s housing increase, when owners serially refinanced and concurrently pulled “money” from their houses whereas property values skyrocketed.

You’ll have additionally heard the phrase, “utilizing houses as ATM machines.”

Properly, the draw back to this seemingly profitable apply is that mortgage balances additionally develop once you refinance.

You don’t simply get free cash. In the event you refinance and pull money out, your mortgage quantity grows, no ifs, ands or buts about it.

This will finally result in points if it is advisable refinance once more sooner or later, and even if you happen to want to promote your property.

If sooner or later your excellent mortgage stability exceeds the property worth, you would wind up with an underwater mortgage.

Did You Run Out of Residence Fairness?

- Many debtors serially refinanced throughout the early 2000s housing increase

- And zapped all their house fairness within the course of

- On the identical time house costs dropped quickly

- Making it unimaginable to refinance by way of conventional channels

When the housing appreciation get together got here to a sudden finish round 2006, many of those owners turned the proud house owners of underwater mortgages – that’s, they owed extra on their mortgages than their properties have been value.

For instance, a house purchaser might have acquired their property for $400,000, then finally refinanced it at a price of $500,000.

In the event that they pulled out the utmost amount of money, which was typically 100% LTV/CLTV again then, any worth drop would imply they have been in a unfavourable fairness place.

Unique house worth: $400,000

Unique mortgage quantity: $400,000

New worth: $500,000

New mortgage quantity: $500,000

Newest appraised worth: $475,000

The situation above was fairly widespread again within the early 2000s. A house purchaser would buy a property with zero down financing, then finally apply for a cash-out refinance as the worth rose.

This was clearly unsustainable, and finally led to an enormous housing bubble and subsequent burst.

It additionally led to document low unfavourable fairness ranges, with hundreds of thousands holding underwater mortgages.

Sadly, you sometimes can’t even do a price and time period refinance if you happen to’re underwater in your mortgage, which means these searching for cost reduction have been successfully shut out.

Finally, packages got here alongside to handle the scenario, such because the Residence Reasonably priced Refinance Program (HARP), which had no higher restrict on LTV ratio. In different phrases, even if you happen to have been deeply underwater, you would nonetheless apply for a price and time period refinance.

Is It Time to Carry Again a Excessive LTV Refinance?

Occasions are rather a lot totally different in the present day, however with house costs seemingly plateauing in lots of cities nationwide, and even falling in others, an identical situation may unfold.

Whereas current house gross sales hit their lowest degree in practically 30 years, we nonetheless noticed about 4 million transactions happen.

There are additionally the new-builds, which have grabbed extra market share in recent times as affordability tanked with considerably larger mortgage charges.

This implies there could be a cohort of debtors who discover themselves in an underwater place if house costs don’t handle to eek out features, and as an alternative fall.

Whereas I’m optimistic we’ll keep away from a full-blown housing crash, it’s potential some would possibly fall into unfavourable fairness positions.

The HARP possibility is lengthy gone (it got here to an finish in late 2018), and replacements like Fannie Mae’s Excessive LTV Refinance Choice have additionally been briefly paused due partly to low quantity.

There simply hasn’t been a necessity for it recently. However may that change? And if that’s the case, what’s one other answer for these needing to refinance?

One Choice for the Underwater Home-owner is a Money-In Refinance

As famous, the high-LTV refinance choices have been been put to relaxation on account of a scarcity of want. Most householders are in an important spot in the present day.

A part of that is because of large house appreciation because the housing backside round 2012-2013. The opposite piece is the ATR/QM rule, which banned dangerous mortgage options like interest-only and 40-year mortgage phrases.

Debtors additionally elevated their down funds in recent times, typically to win a bidding struggle. And LTVs have additionally been massively diminished on cash-out refinances.

The top result’s the best quantity of house fairness on document, with few debtors actively tapping into it.

However as I mentioned, there could be instances for current house consumers, who might have seen costs fall since they bought a property.

Sadly, these identical consumers might have additionally been saddled with a a lot larger mortgage price, maybe one thing within the 7-8% vary on a 30-year mounted.

If and when charges fall they usually apply for a refinance, they might discover that they’re a bit of quick.

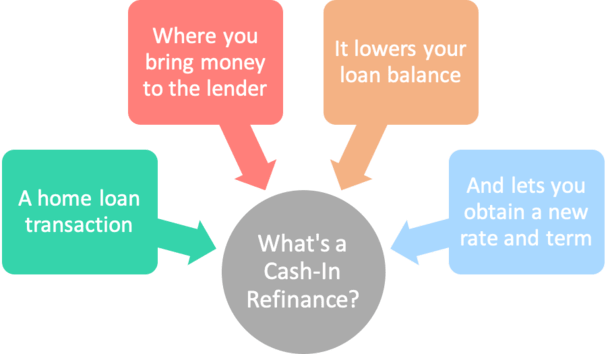

So what are they to do? Enter the “cash-in refinance.”

Merely put, a cash-in refinance is the other of a cash-out refinance. When owners apply for a cash-in refinance, they bring about cash to the closing desk to decrease their mortgage stability.

This enables them to fulfill any LTV limits and qualify for the mortgage. For instance, Fannie Mae has a most 97% LTV for a price and time period refinance.

So in case your mortgage stability is $502,000 and the house is simply appraised at $515,000, you’ll have an issue.

Let’s take a look at an instance of a cash-in refinance:

Buy worth: $525,000

Present house worth: $515,000

Mortgage stability: $502,000

Most mortgage quantity: $499,550 (97% LTV)

Think about a home-owner who bought a property for $525,000 with 3% down in late 2023 when mortgage charges peaked (hopefully) and in the present day, unbeknown to them, it’s value solely $515,000.

They see that mortgage charges are actually nearer to six.5% and apply for a price and time period refinance, utilizing an estimated worth of $540,000.

The house is appraised and the worth is available in low, at simply $515,000. The max mortgage quantity at 97% LTV is $499,550 they usually nonetheless owe $502,000.

The borrower should provide you with $2,450 (plus any closing prices) to make up the shortfall and attain the cash-in refinance.

Doing so would put their LTV at 97%, which is the max allowed for a conforming mortgage.

Assuming the borrower has the funds out there, they might deliver on this cash to get the mortgage quantity right down to an appropriate degree.

Why a Money-In Refinance?

- To decrease your mortgage quantity to an appropriate degree

- That’s at/under the max LTV allowed by the lender

- Or to maintain it at/under a sure threshold like 80% LTV

- To keep away from mortgage insurance coverage and acquire a decrease rate of interest

- Additionally to remain at/under the conforming mortgage restrict

Debtors may have a cash-in refinance for a number of totally different causes.

Most likely the commonest cause up to now decade needed to do with the underwater owners I simply talked about.

These quick on house fairness just about haven’t any alternative however to deliver money in to qualify for the refinance in query.

In different phrases, they received’t qualify except they pay down their mortgage stability to an appropriate degree.

Currently, this has been any degree at/under 97% LTV, which is the standard most allowed by standard mortgage lenders.

Be aware that FHA and VA debtors can make the most of a streamline refinance, which permits debtors to make use of the unique buy worth for the LTV and/or permits LTVs above 100%.

Nonetheless, cash-in refinances aren’t only for the distressed home-owner. Debtors can even make the most of them with a purpose to decrease their mortgage balances to allow them to qualify for a decrease mortgage price.

An instance could be a home-owner whose excellent mortgage stability places them at say 90% LTV.

If they bring about in one other 10%, their LTV drops to 80%, pushing their rate of interest decrease due to extra favorable pricing changes.

On the identical time, they keep away from the necessity for mortgage insurance coverage, which may value tons of per thirty days.

Bringing in money can even decrease your mortgage quantity, which equates to a decrease month-to-month mortgage cost and reduces the quantity of curiosity you pay all through the lifetime of the mortgage.

So it’s a triple win: smaller mortgage quantity, decrease rate of interest, and no MI!

One more reason to usher in money is to make sure the conforming mortgage restrict isn’t exceeded, thereby avoiding jumbo mortgage pricing.

It may be tougher to acquire a jumbo house mortgage, or the pricing may be much less favorable, so a borrower might select the sort of refinance to maintain prices down and enhance approval possibilities.

[Can you refinance with negative equity?]

Why a Money-In Refinance Might Not All the time Be the Finest Transfer

- Contemplate the alternate options to your money

- You would possibly be capable of earn extra elsewhere

- Equivalent to in a retirement account or one other funding

- Keep in mind to diversify your belongings and keep liquidity

All the above sounds fairly superior, proper? Properly, except it’s a must to herald money to qualify for the refinance, it may not at all times be the most effective transfer.

In case your cash will earn extra in an funding account, paying down your mortgage early received’t essentially be the best alternative. The identical primary precept applies right here.

However do the mathematics if you happen to’re near a sure LTV threshold, and the mortgage price might be a lot decrease. Particularly if you happen to’re near 80% LTV and might eliminate mortgage insurance coverage!

Simply notice that if house costs slip additional otherwise you want money for an emergency, having it locked up in an illiquid funding received’t do you a lot good.

Typically it’s finest to maintain much less cash tied up within the house, and maybe put extra time in looking for a extra aggressive price.

Learn extra: What’s a brief refinance?

Earlier than creating this web site, I labored as an account govt for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 19 years in the past to assist potential (and current) house consumers higher navigate the house mortgage course of. Comply with me on Twitter for decent takes.