{kind=link}

By Jeff Dunsavage, Head of Analysis Publications and Insights, Triple-I

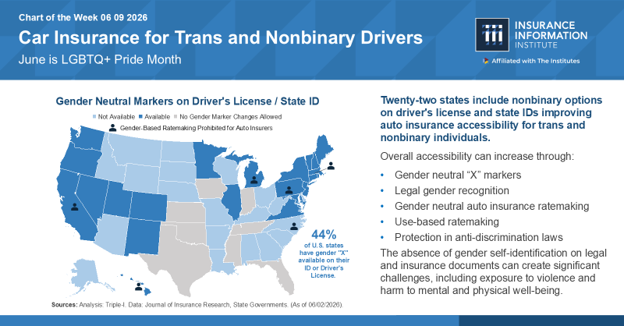

Gender is one in all many elements insurers contemplate when a driver’s danger profile, as permitted or prohibited by state legal guidelines and rules, utilizing the gender indicated on drivers’ licenses. Twenty-two states presently present – along with “male” and “feminine” designations – non-binary gender identification choices or don’t require gender to be listed in any respect.

What are the insurance coverage implications, if any and the place permissible by state regulation, of a non-binary gender marker or the absence of any gender marker on a driver’s license? The quick reply is that state-by-state variations within the related knowledge restrict the influence.

State use of gender markers

As of June 2026, 22 states permit an “X” gender marker on state IDs and driver’s licenses, representing 44 % of the nation. Interpreted in some states as a “not specified” gender, the X marker is extensively thought to be a gender-neutral choice for individuals who aren’t completely male (“M”) or feminine (“F”), which can embrace trans, nonbinary, and/or intersex people. Oregon grew to become the primary state to authorize the designation in 2017, following within the footsteps of comparable legal guidelines in a number of different nations.

Inside states that provide X markers, residents might replace their gender marker to F, M, or X with various levels of ease, relying on state course of necessities. Residents outdoors these states are restricted to F or M designations, with gender marker corrections on state IDs and driver’s licenses altogether prohibited in no less than eight states.

By inhabitants, 51 % of trans adults dwell in states that permit these F, M, or X marker updates. Twenty-two % dwell in states that bar these modifications, based on estimates from the Motion Development Undertaking. This determine might develop as laws proscribing the authorized recognition and rights of trans folks ramps up throughout the nation, with practically 800 such payments into consideration thus far this 12 months, 60 of which have handed. Multiple thousand have been thought-about in 2025, marking the sixth consecutive record-breaking 12 months for such proposals.

Threat-based pricing

“Threat-based pricing” is a fundamental insurance coverage idea that may appear intuitively apparent when described – but misunderstandings about it steadily sow confusion. Merely put, it means providing completely different costs for a similar stage of protection, primarily based on danger elements particular to the insured individual or property. If insurance policies weren’t priced this fashion – if, for instance, insurers needed to give you a one-size-fits-all value for auto protection that didn’t contemplate car kind and use, the place and the way a lot the automotive will probably be pushed, and so forth – lower-risk drivers would subsidize riskier ones.

Little uniform knowledge presently exists, nonetheless, on accident traits amongst trans and nonbinary drivers. Because of this, it’s unclear whether or not or how charges may be affected for these with an X gender marker or for these with out an up to date gender marker of any type.

Telematics can assist

A 2021 article from the Nationwide Affiliation of Insurance coverage Commissioners’ (NAIC) Journal of Insurance coverage Regulation, in addition to a 2024 Casualty Actuarial Society (CAS) examine, level to the promise supplied by telematics and usage-based applied sciences. The NAIC Journal article recommends abandoning gender as a ranking issue, arguing that “know-how has superior the chance to extra instantly measure precise driving conduct and publicity by means of different predictors.” The CAS examine suggests telematics can “considerably scale back the necessity to embrace age, intercourse, and marital standing within the claims frequency and severity fashions.”

Whereas acknowledging “not the entire delicate variables we examined could possibly be eradicated from the mannequin,” the CAS examine went on to say, “The evaluation exhibits there may be nonetheless worth in insurers testing the addition of telematics to their fashions to probably scale back reliance on delicate info that might end in precise or perceived bias.”

Dedication to equity

Truthful, correct pricing and underwriting are on the coronary heart of the risk-based method, and property/casualty insurance coverage trade is dedicated to making sure equity and selling belief throughout all of the communities it serves. Insurers and the actuaries and knowledge scientists that help them are nicely positioned to proceed serving to policymakers and decisionmakers perceive the complicated science of danger and play a constructive position within the coverage dialogue.

Be taught Extra:

LGBTQIA+ Homeownership Hole Could Be Fueling Insurance coverage Safety Hole

Variety and Inclusion within the Insurance coverage Business

Clarifying Drivers of Rising Auto Premiums

Allstate, Aspen Initiative Seeks to Ease Belief Hole

Human Wants Drive Insurance coverage and Ought to Drive Tech Options

Triple-I Points Temporary: Threat-Primarily based Pricing of Insurance coverage (Members solely content material)