{kind=link}

In imperial China, 3 p.c was the utmost authorized month-to-month mortgage charge; charging extra was punishable by 40 to 100 blows with the “gentle cane.” (Rockoff 2003) Centuries later, many U.S. states are imposing the identical cap (with out corporal penalties) on different credit score suppliers, akin to payday, installment, and auto-title lenders, with the objective of decreasing credit score prices and delinquency for the high-risk debtors that depend on these funding sources. A priority, nonetheless, is that lenders will merely refuse to lend to those debtors at decrease rates of interest. Our current Employees Report research how rate of interest caps have performed out in a number of states that not too long ago adopted them. Utilizing household-level knowledge from a significant credit score bureau, we discover that mortgage balances for the riskiest debtors declined considerably relative to counterparts in states with out caps. Regardless of taking over much less debt, these debtors didn’t expertise an enchancment in delinquencies.

The Resurgence of Usury Limits

Usury limits have waned over the centuries within the U.S, however their current resurgence on the buyer facet was triggered by payday lenders’ entry into the small greenback mortgage market within the mid-Nineteen Nineties (Rockoff 2003). In 2007, charges on loans to army workers had been capped at 36 p.c—marking the first-ever nationwide usury restrict within the U.S. A invoice at the moment earlier than Congress, the Predatory Mortgage Elimination Act, would lengthen the 36 p.c cap throughout all the U.S.

Saunders (2021) traces the 36 p.c normal again to credit score reform within the early twentieth century. Involved that prevailing usury limits had been too low, the Russell Sage Basis promulgated a Uniform Small Mortgage Regulation recommending the next cap of three.5 p.c per thirty days. Thirty-four states raised caps to between 36 and 42 p.c over the subsequent few a long time (Anderson et al. 2015).

Cheaper Credit score…or Much less Credit score?

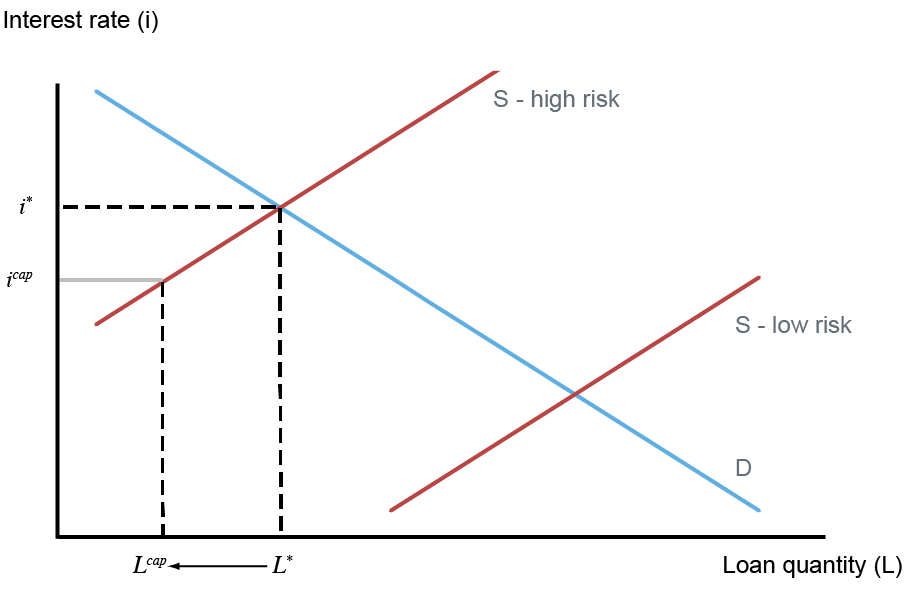

Opponents of charge caps predict that they are going to decrease the availability of credit score for riskier debtors reasonably than drive down the price of credit score. The textbook credit score mannequin beneath illustrates this impact. On this mannequin, lenders individually present credit score for high-risk debtors (sH) and low-risk debtors (sL). At market equilibrium, lenders cost high-risk debtors i*, which is greater than what they might cost low-risk debtors; lenders cost high-risk debtors the next rate of interest to compensate for greater anticipated mortgage losses. Nonetheless, a usury cap requires lenders to cost no greater than icap for curiosity, which is decrease than the equilibrium charge i*. Because of this, lenders contract the amount of loans provided, as proven. In actual fact, if earnings from loans to high-risk debtors don’t cowl the fastened value of offering them, lenders might completely refuse to make any loans to high-risk debtors, which is known as credit score rationing. That is significantly seemingly as much less creditworthy debtors are additionally usually extra prone to take out comparatively small loans.

Notice that icap is greater than the equilibrium rate of interest for low-risk debtors, and below normal mannequin assumptions, lending to lower-risk debtors doesn’t change. Nonetheless, below sure situations, the speed cap may even have implications for low-risk debtors, a state of affairs we study within the subsequent submit on this sequence.

Fee Caps Might Contract Credit score to Riskier Debtors

Notes: This chart exhibits a easy mannequin of shopper lending and illustrates how a usury cap would have an effect on the market. There are two sorts of debtors—high-risk and low-risk—and provide of credit score is individually decided for high- (sH) and low-risk debtors (sL). At equilibrium, high-risk debtors are capable of borrow L* {dollars} of loans, at an rate of interest of i*. Below the usury cap, lenders can solely cost icap, and in consequence cut back the amount of loans provided to Lcap.

Our Research

We examined how credit score modified in three states that enacted 36 p.c charge caps someday between 2016 and 2022 (Illinois, South Dakota, and North Dakota). Solely different lenders’ mortgage charges are capped; banks and credit score unions are exempt. Our knowledge are from the New York Fed Client Credit score Panel/Equifax (CCP), which tracks quarterly debt and delinquency for an anonymized, random subset of households coated by the Equifax credit score bureau. Comprising 5 p.c of Equifax-monitored households, the pattern contains over 35 million debtors.

Since charge caps usually tend to bind for riskier debtors, we sorted households into ten equal-sized teams (deciles) primarily based on their credit score scores (Equifax Threat Rating 3.0), with the lowest-scoring debtors within the first decile. The common mortgage delinquency charge for this group was over six instances greater than the typical throughout the opposite deciles.

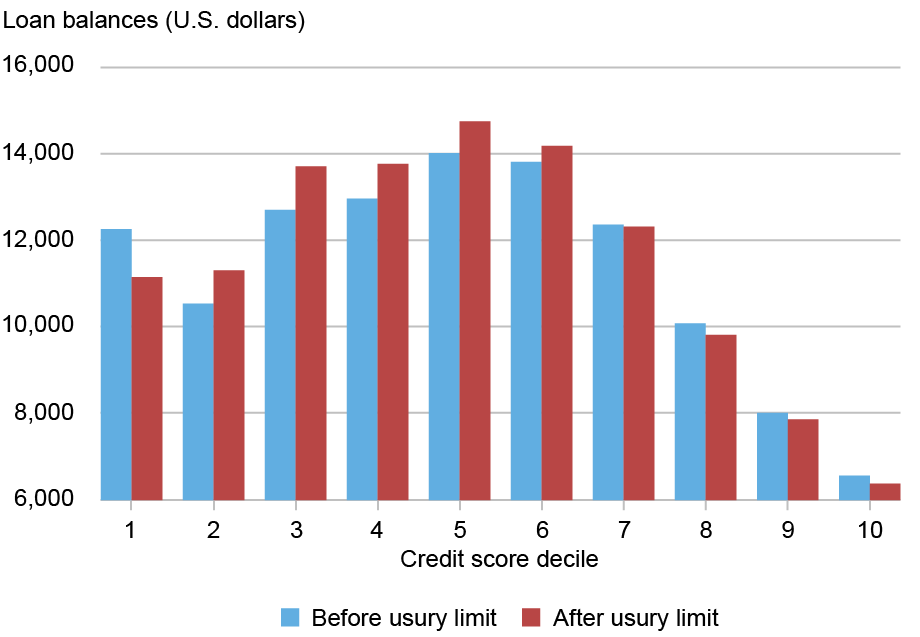

To get a way of the info, the chart beneath exhibits common mortgage balances for debtors within the states with usury limits (excluding mortgages and pupil loans) for every threat decile. Predictably, households with the bottom and highest scores owe much less. Extra related is that balances declined by about 8 p.c for the primary (riskiest) decile after charges had been capped; balances for safer debtors had been little modified total.

Mortgage Balances for the Riskiest Debtors Declined After Fee Caps

Notes: This chart exhibits how common mortgage balances for households in Illinois, North Dakota, and South Dakota modified after mortgage charges had been capped in these states. Households are stratified by credit score rating decile, with decile 1 containing these with the bottom scores. Mortgage and pupil loans are excluded.

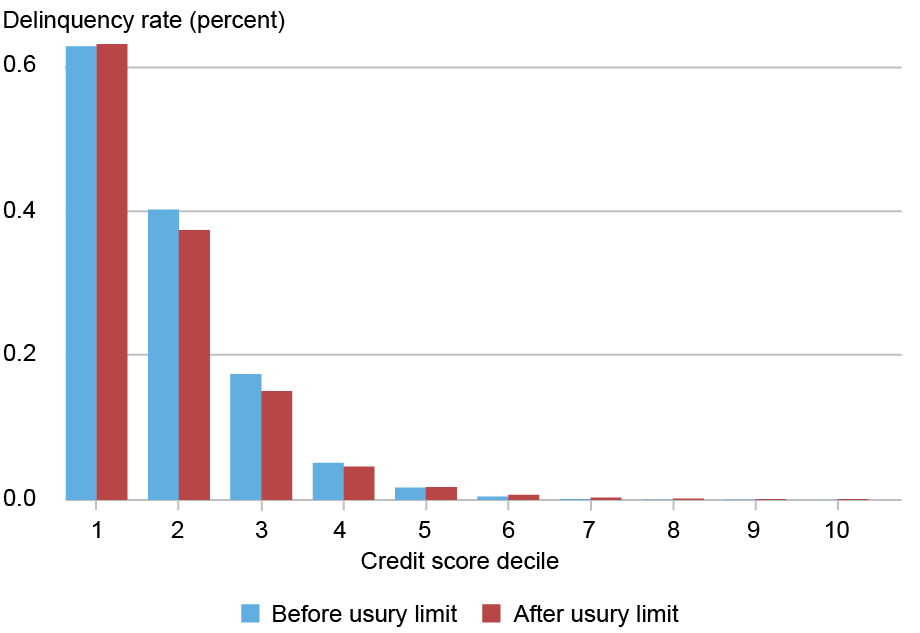

Decrease debt balances could be salutary in the event that they mirror that riskier debtors are avoiding “debt traps.” But charge caps didn’t result in fewer delinquencies for these debtors, because the chart beneath exhibits. Their share of delinquent accounts (90+ days overdue) was basically unchanged, whereas delinquency for considerably lower-risk households tended to fall.

Mortgage Delinquency Among the many Riskiest Debtors Did Not Decline After Usury Limits

Notes: This chart exhibits how delinquency charges for households in Illinois, North Dakota, and South Dakota modified after mortgage charges had been capped in these states. Households are stratified by credit score rating decile, with decile 1 containing these with the bottom scores. Delinquency is measured by the share of accounts which are 90+ days overdue. Delinquencies on all sorts of debt are included within the chart.

Cross-State Comparability

The charts above solely present adjustments in credit score for debtors within the states that capped charges. In our primary evaluation, we examine debtors in these states to counterparts in a set of management states that didn’t cap charges over the examine interval. Utilizing regression evaluation, we estimate how credit score for high-risk debtors within the handled states modified relative to counterparts after charge caps took impact, the place high-risk debtors are outlined as those that had been within the lowest decile of threat scores earlier than the usury restrict. Particularly, we estimate an event-study regression to look at how credit score market outcomes modified for high-risk debtors in states with usury limits, relative to regulate with no usury restrict. Importantly, these regressions enable us to regulate for adjustments over time taking place in every state which are unrelated to the usury restrict, and for variations between debtors unrelated to the usury restrict.

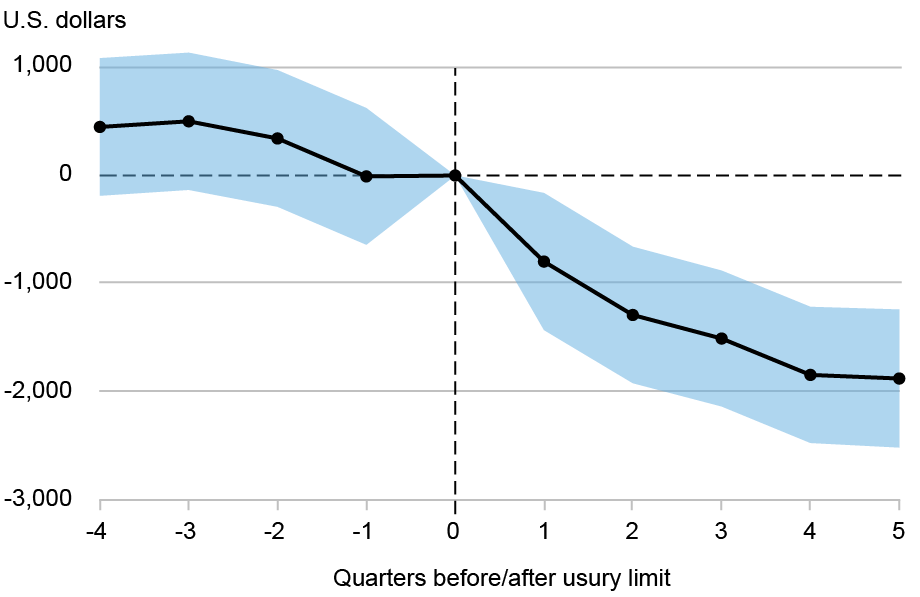

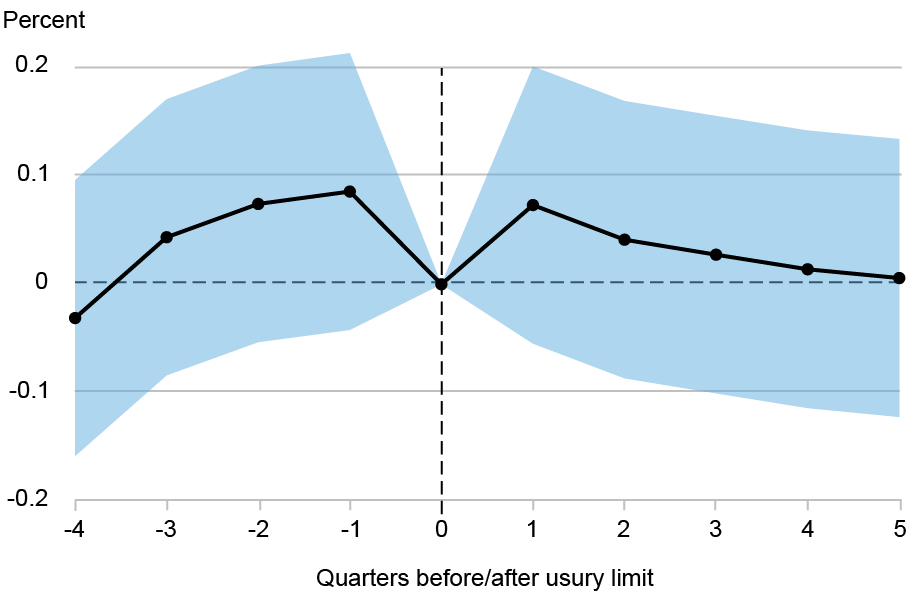

The estimates for mortgage balances are plotted beneath, together with confidence intervals. Relative to regulate state ranges, the typical mortgage balances of the riskiest debtors in rate-cap states weren’t considerably completely different earlier than these caps took impact, which signifies that the management teams used on this examine provide an affordable level of comparability. Nonetheless, they declined considerably afterward. The impact is substantial. Particularly, as of 5 quarters after charges are capped, debt balances of the riskiest debtors in these states fall by round $2,000, relative to the balances of the riskiest debtors in control-states.

Balances for the Riskiest Debtors Decline After Fee Caps Relative to Management States

Notice: This chart exhibits how the debt balances of high-risk debtors in Illinois, North Dakota, and South Dakota modified after the implementation of usury limits in these states, relative to the debt balances of their counterparts in management states.

The subsequent chart exhibits how relative delinquencies advanced. These estimates are much less exact (as mirrored within the broad confidence bands), however they definitely don’t level to a decline in delinquencies. Total, evidently there was no change in delinquencies for the riskiest debtors in states with usury limits relative to these in management states after the usury limits had been handed.

Delinquency Charges of Riskiest Debtors Maintain Regular Relative to Management States

Notice: This chart exhibits how the likelihood of getting a delinquent mortgage modified for high-risk debtors in Illinois, North Dakota, and South Dakota after the implementation of usury limits in these states, relative to delinquency charges for his or her counterparts in management states.

Summing Up

Usury limits, an historical sort of economic regulation, are resurgent within the U.S. Advocates anticipate charge caps to decrease borrowing prices for high-risk debtors whereas opponents predict that the end result might be much less credit score for these debtors. Our findings sq. higher with the latter view, calling into query the advantages of those legal guidelines for high-risk debtors. In our subsequent submit, we study whether or not lenders reallocate credit score to considerably lower-risk debtors in response to charge caps.

Rajashri Chakrabarti is an financial analysis advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Gabriel Leonard is a analysis analyst within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

On the time this submit was written, Donald P, Morgan was a monetary analysis advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group. He’s now retired.

Thu Pham is a analysis analyst within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Lee Seltzer is a monetary analysis economist within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

The right way to cite this submit:

Rajashri Chakrabarti, Gabriel Leonard, Donald P. Morgan, Thu Pham, and Lee Seltzer, “The Unintended Results of Curiosity Fee Caps: Credit score Rationing for Dangerous Debtors,” Federal Reserve Financial institution of New York Liberty Road Economics, June 3, 2026, https://doi.org/10.59576/lse.20260603a

BibTeX: View |

Disclaimer

The views expressed on this submit are these of the writer(s) and don’t essentially mirror the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the accountability of the writer(s).