{kind=link}

As a part of a broader advertising and marketing technique, RIAs may work with “solicitors” or “promoters” (e.g., accountants, on-line advisor matching platforms, and compensated bloggers) who refer potential purchasers in trade for compensation. Whereas the SEC’s Advertising Rule units forth guidelines requiring RIAs to reveal their compensation preparations with any paid promoters and the potential conflicts they entail, some corporations won’t notice that, relying on the connection between the RIA and the promoter and the extent to which the promoter supplies ‘recommendation’ to potential purchasers, disclosure alone won’t be sufficient for the RIA to be totally in compliance.

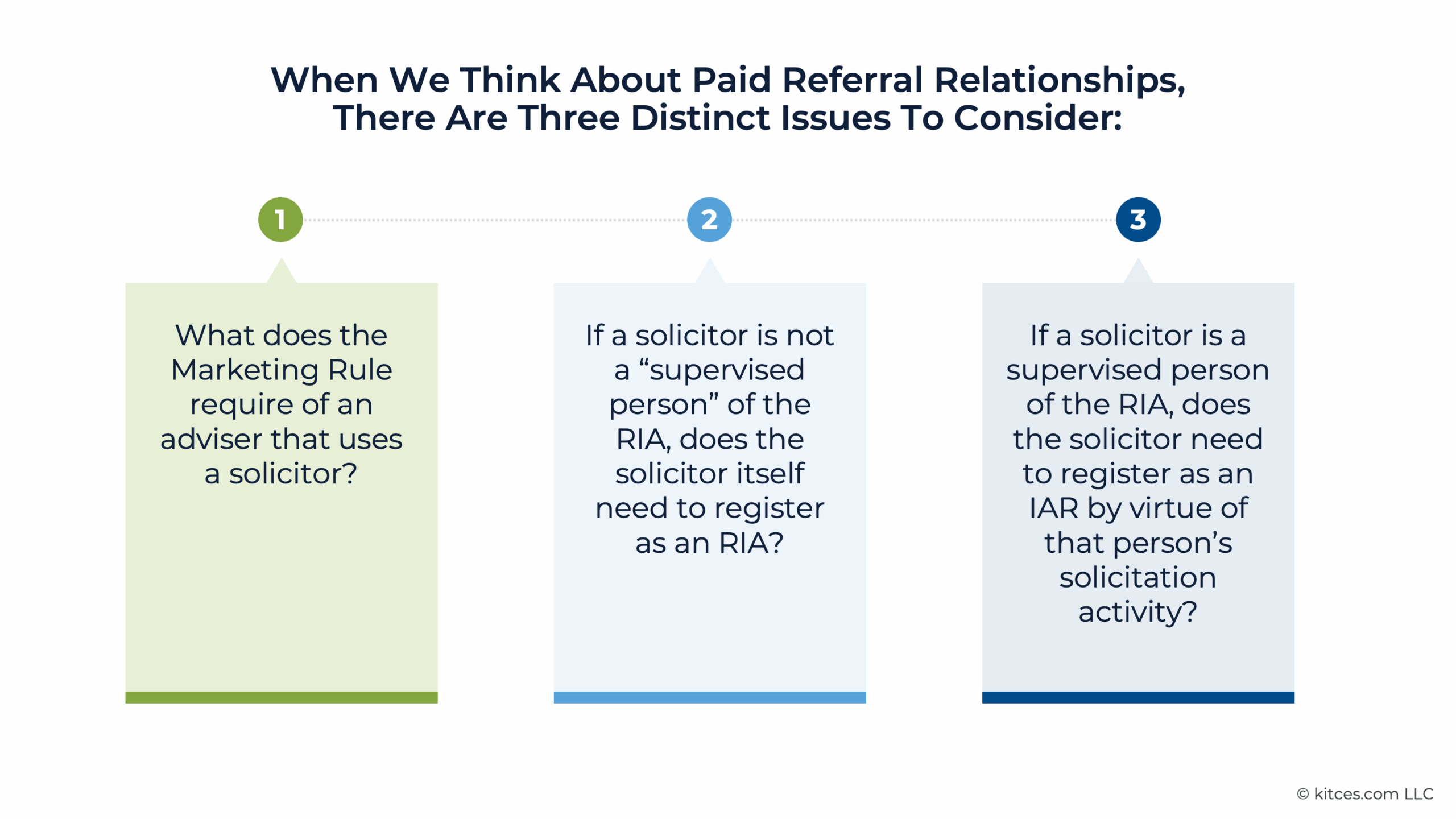

On this visitor submit, Isaac Mamaysky, Companion of Potomac Legislation Group and Cofounder and COO of QuantStreet Capital, explains the necessities for paid referrals below the SEC Advertising Rule, why paid promoters might must register as RIAs (or IARs), and whether or not the registration burden lies within the palms of the promoter or the RIA that is compensating them.

To begin, an RIA partaking with a promoter will wish to guarantee compliance with the Advertising Rule (and supply the required Type ADV disclosures) for the testimonials and endorsements themselves. For instance, the Advertising Rule requires that advisers disclose, amongst different objects, whether or not money or non-cash compensation was supplied for the testimonial or endorsement and any materials conflicts of curiosity arising from the adviser’s relationship with the promoter.

Subsequent, the RIA can decide whether or not the promoter is a supervised individual of the agency, outlined by the Funding Advisers Act as “any associate, officer, director (or different individual occupying an analogous standing or performing comparable features), or worker of an funding adviser, or different one who supplies funding recommendation on behalf of the funding adviser and is topic to the supervision and management of the funding adviser”. If a promoter is set to be a supervised individual, the RIA should decide whether or not the promoter is required to register as an funding adviser consultant (IAR) below relevant state regulation.

If, as a substitute, a promoter is performing independently of the adviser (i.e., not as a supervised individual), whereas there isn’t any express requirement for advisory corporations to verify their unaffiliated promoters’ registration standing, prudent corporations might select to conduct due diligence into the promoter’s compliance with their standalone registration obligations (if any).

In the end, the important thing level is that whereas the Advertising Rule made it simpler to make use of each paid and unpaid promoters for enterprise improvement, there are nonetheless compliance obligations relating to their use that would journey up advisors who haven’t got a full understanding of their necessities. However, by figuring out whether or not they have made ample disclosures relating to the usage of a solicitor, in addition to whether or not a solicitor is a supervised individual (and following the related Federal and state registration necessities relying on the solicitor’s standing), corporations can be certain that they adjust to not solely the necessities of the Advertising Rule itself, but in addition these below the Advisers Act, SEC, and state rules that make up the total compliance panorama for testimonials and endorsements.