{kind=link}

Mortgage charges have had a reasonably good April, all issues thought-about.

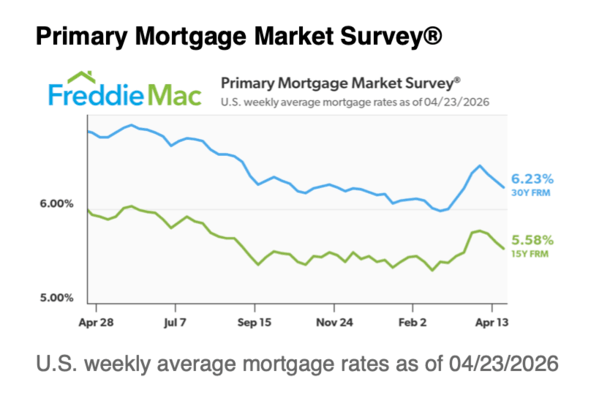

They’ve come down about 30 foundation factors (0.30%) over the previous month, regardless of the battle in Iran nonetheless raging on.

So I used to be curious the place mortgage charges could be with no warfare in Iran, had it by no means gotten began on the finish of February.

Again then, we had been slightly below 6% for a 30-year mounted and apparently we’d nonetheless be there had historical past been completely different.

And whereas the distinction in month-to-month cost is perhaps negligible, the psychological issue may have been large for residence consumers this spring.

Mortgage Charges Have a 0.25% ‘Geopolitical Premium’

I requested xAI’s Grok the place mortgage charges could be sans the battle in Iran and it instructed me a few quarter-point decrease.

If we use Freddie Mac’s newest 30-year mounted studying of 6.23%, that may put the favored mortgage sort proper beneath 6%.

As a substitute, debtors are nonetheless going through charges effectively into the 6s, which even when not an enormous cost distinction, should not really feel as good as a 5-handle price.

There’s a purpose most costs finish in .99. It’s no completely different with mortgage charges.

Residence consumers would a lot moderately have a 5%-something versus a 6%-something. It simply appears higher. And I’m certain it feels higher too.

As a substitute, those that’ve been shopping for houses this spring have needed to accept the upper charges, assuming they didn’t purchase down the mortgage price.

As for why, it’s what Grok coined as a “geopolitical premium” of about 25 bps.

Right here’s the way it breaks down:

- Pre-conflict 30-year mounted mortgage price: 5.98%

- Minus embedded geopolitical premium right this moment (~25 bps)

- Plus/minus modest pure drift (0–10 bps decrease)

- Mortgage price vary: 5.85% to six.05%

- Midpoint guess: 5.95%.

Mortgage Charges Often Fall Throughout Unsure Occasions

Usually, mortgage charges fall when there’s a warfare as a result of there’s a flight to security in bonds.

Traders search a protected haven in unsure instances. This time is completely different.

We’ve a inventory market at/close to all-time highs as traders proceed to chase increased returns within the face of $105+ per barrel oil.

So actually it’s not a lot a geopolitical premium as it’s an power worth premium, given oil was nearer to $70 per barrel pre-conflict.

If we take into account the 10-year bond yield, it was slightly below 4% previous to the warfare with Iran, and now sits round 4.30%.

This implies it’s largely the distinction in yields pushing 30-year mounted mortgage charges increased, and slightly little bit of the unfold widening.

The subsequent query is when can mortgage charges return to pre-war ranges? That’s a harder one to reply as a result of the trail stays very unclear.

Earlier than creating this web site, I labored as an account government for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 19 years in the past to assist potential (and current) residence consumers higher navigate the house mortgage course of. Observe me on X for decent takes.