{kind=link}

The extra wealth you construct, the extra the tax code turns into a central character in your monetary story. For prime-income earners, the distinction between a reactive and proactive strategy to taxes isn’t marginal. It’s materials and requires the flexibility to consider not solely at this time, however how choices you make at this time would possibly influence your tax state of affairs years down the highway.

The tax methods beneath aren’t a one-size-fits-all guidelines. They’re a framework for fascinated with the place actual alternatives exist for long-term tax effectivity. Your particular state of affairs will usually require the judgment of a certified tax skilled, and nothing right here ought to substitute for that. However understanding these ideas equips you to have the proper conversations.

1. Benefit from autos for future tax-free earnings.

Usually right here, you’re buying and selling a present tax profit within the type of decrease taxable earnings now for a future good thing about tax-free earnings later. Regardless of being in a excessive tax bracket at present, you could possibly be in an excellent HIGHER tax bracket sooner or later…even you probably have decrease earnings. Altering tax charges and brackets are at all times a chance in our political atmosphere–planning for this inevitability can alleviate nervousness surrounding future tax charges growing above the place they’re now.

So, how will you navigate this?

Roth Conversions

The One Massive Stunning Invoice Act (OBBBA), signed in 2025, made the person earnings tax charges initially established beneath the Tax Cuts and Jobs Act everlasting. That mentioned, present tax charges aren’t assured to stay unchanged indefinitely. Future Congresses can at all times revisit the tax code, and lots of the greater deductions that taxpayers are having fun with now beneath the OBBBA are scheduled to sundown after 2029, which means you may even see greater taxes in future tax years even when charges don’t change. Paying taxes now on Roth conversions whereas the present charges are identified nonetheless has strategic benefit for individuals who anticipate greater taxable earnings in retirement. This may help you construct tax-free wealth in your future wants or in your heirs to inherit. Be mindful:

Conventional IRA withdrawals are taxable as bizarre earnings, however certified Roth IRA withdrawals are tax-free. Usually, certified Roth IRA withdrawals embody these made after you flip 59 ½ and proudly owning a Roth IRA for no less than 5 years.

You might convert an infinite quantity out of your Conventional IRA to Roth IRA as usually as you would like. The transformed quantity can be taxable as bizarre earnings within the 12 months the conversion is finished–spreading out conversions over a number of tax years can provide you some management over your taxes.

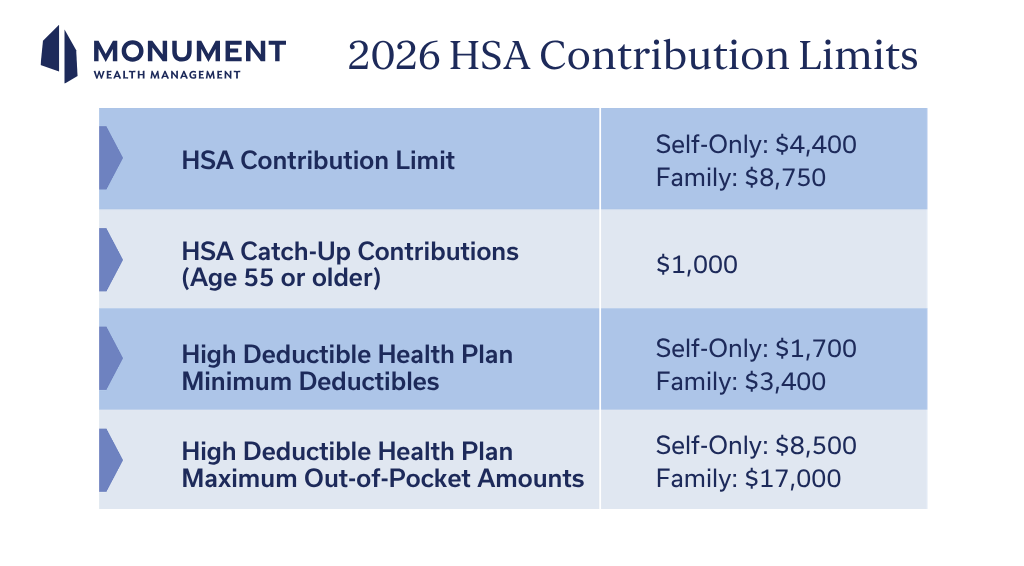

Well being Financial savings Account Contributions

With a well being financial savings account (HSA), you obtain a triple tax profit: tax-deductible contributions, tax-free earnings, and future tax-free withdrawals for certified medical bills!

There are some limitations to think about:

- You need to have a high-deductible well being plan to be eligible. Even you probably have nice well being advantages, it’s turning into an increasing number of frequent for firms to save lots of a buck by switching to high-deductible well being plans the place workers bear extra of the fee.

- You’ll obtain a present above-the-line tax deduction for any contributions you make to your HSA. This lowers your adjusted gross earnings (AGI), which can profit you as a result of your AGI is used to find out the brink for some below-the-line deductions and tax credit–which means extra potential tax financial savings!

- Your earnings compound tax-free.

- Withdrawals are tax-free for medical bills. Take into consideration the compounding potential when contributions are invested and stay untouched till retirement!

As a high-income earner, you might really feel comfy about your capability to cowl out-of-pocket medical prices. Don’t low cost the wealth-generating potential and adaptability an HSA can afford you, from decreasing your present taxable earnings now to making a tax-free supply of cash for an unsure future.

Roth 401(ok) vs. Conventional 401(ok) Deferrals

Many individuals prefer to decrease their present taxable earnings within the type of pre-tax, or Conventional, 401(ok) deferrals from their paycheck on to their employer-sponsored retirement plan. This can be a alternative that displays the assumption that taxes can be decrease sooner or later when cash is withdrawn in retirement than they’re at this time. Saving for retirement in any type is an efficient factor–however there is likely to be a greater tax technique so that you can think about within the type of a Roth 401(ok) as a high-income earner, relying in your marginal tax fee.

There isn’t a income-limit eligibility for a Roth 401k (not like a Roth IRA) and it additionally presents a better contribution restrict of $24,500 (plus a $8,000 catch-up over age 50 or $11,250 for these ages 60 to 63.) This received’t decrease your taxable earnings now however your future self will thanks for the management this will provide you with over how a lot taxable earnings you’ll understand year-to-year in retirement.

As a result of you’ve already paid taxes on the cash contributed to a Roth 401(ok), you’ll be able to withdraw these contributions AND earnings tax-free in retirement. This can be a nice alternative to construct a considerable supply of tax-free earnings to faucet into sooner or later when you might in actual fact be in a better tax bracket or have extra taxable earnings than you thought you’ll in retirement from the portfolio your wealth has constructed.

There could also be alternatives to contribute on a pre-tax foundation to your 401(ok) to decrease taxable earnings now and likewise add after-tax cash to your 401(ok) above the wage deferral limits relying in your plan. Many individuals name this a “Mega Backdoor Roth”, and it’s a method that would mean you can take pleasure in some tax financial savings now and tax financial savings down the highway, however it’s not a method that works for everybody and needs to be fastidiously analyzed in your distinctive state of affairs.

2. Take note of taxes in your portfolio and decrease the place doable.

Nobody ever thinks to themselves, “Hmm, how can I pay extra in taxes this 12 months?” Optimizing your tax technique is at all times the secret which is why ways like Tax-Loss Harvesting and using tax-efficient autos can current quite a lot of artistic alternatives to leverage.

Tax-Loss Harvesting

“Loss” doesn’t must be a four-letter phrase on the subject of your funding portfolio. It creates alternatives to cut back taxable realized beneficial properties. The thought of tax-loss harvesting is that you just’ll be capable to apply these losses towards any realized beneficial properties and as much as $3k in bizarre earnings in your tax return to assist decrease your tax invoice whereas sustaining an optimum asset allocation.

Instance: Rory’s investments carried out very properly final 12 months and he or she offered them whereas they have been up. By promoting her investments at a loss based on a particular set of tax-loss harvesting guidelines, she realized she might offset her realized beneficial properties. Professional tip: When you have extra losses than beneficial properties, you can too cancel out as much as $3k in bizarre earnings. Now that’s some candy lemonade.

You’ll have been burned earlier than and misplaced cash in previous selloffs. Tax-loss harvesting just isn’t the identical factor as taking a loss and by no means having a possibility to get well. By promoting a safety at a loss and changing it with the same safety, you keep market publicity AND cut back your tax invoice on realized beneficial properties elsewhere in your portfolio.

Tax-Environment friendly Automobiles

Particular person shares are low-cost and tax-efficient–which suggests YOU management the timing of realized beneficial properties.

Automobiles like lively mutual funds, and to a lesser extent, ETFs, go capital beneficial properties realized on the FUND stage via to buyers every year. These don’t rely upon whether or not you offered shares of YOUR funding; buyers in these autos have much less management over the quantity of taxable earnings attributable to their portfolio in a given 12 months.

Mutual funds and ETFs should have an necessary place in your diversified portfolio, nevertheless. However together with particular person shares is an efficient strategy to management your tax image AND reap the benefits of tax-loss harvesting alternatives. Take into account that not each inventory in an index can be performing the identical and rising collectively–by utilizing particular person shares vs. an index ETF or fund, you’ll have extra alternatives to lock in invaluable losses for tax functions with out dropping management over realizing beneficial properties.

For benchmark-conscious buyers, utilizing particular person shares additionally permits for Direct Indexing, which is basically proudly owning a basket of particular person shares to copy a benchmark index’s efficiency and danger profile as a substitute of proudly owning a single ETF or mutual fund. The sort of tax-loss harvesting over an extended time frame can improve general efficiency within the type of probably greater after-tax returns. This could’t be finished successfully with mutual funds or ETFs.

It’s value noting that it’s necessary to take a rules-based strategy to investing in particular person shares to keep away from the behavioral pitfalls we are able to sometimes fall sufferer to.

Our recommendation: Take away emotion out of your funding choices. That is the place an advisor will add a ton of worth in preserving you trustworthy.

3. Rethink your charitable giving technique.

Checkbook giving is frequent–it’s easy and handy. However you might be leaving one thing on the desk by not contemplating different methods to present. Your charitable giving technique deserves the identical personalized consideration paid to different areas of your monetary life, particularly on the subject of tax financial savings alternatives.

Donate Appreciated Inventory

Eradicate future capital beneficial properties on inventory you’ve held for no less than a 12 months AND get a deduction for those who itemize. Restricted itemized deductions of as much as 30% of AGI are permitted for donated appreciated inventory–you might carry any extra above the 30% AGI threshold ahead into future years. Whereas that is lower than the AGI restrict for money donations, there’s a present and future tax profit. It’s sensible to reap the benefits of this given uncertainty surrounding future capital beneficial properties tax charges for high-income earners. Adjustments beneath OBBBA do restrict the worth of itemized deductions for charitable presents, and the invoice additionally launched a brand new deduction for money presents made to charity for these taking the usual deduction, so it’s a good suggestion to know whether or not you itemize or take the usual deduction if you’re contemplating donating inventory to charity.

When you have a big place in your organization’s inventory, that is additionally an effective way to cut back focus danger and not using a tax hit and have some management over the place your wealth goes.

Donor-Suggested Fund

If you end up in an particularly high-income 12 months (perhaps you offered your enterprise or had invaluable restricted inventory vest), you would possibly need to think about a Donor Suggested Fund. With this sort of car, you possibly can unfold grants out to organizations over time or permit the cash you’ve donated to the Fund (which itself is a 501c3) to proceed to develop tax-free for future transformational giving. Additionally, it is a nice strategy to get your loved ones and the subsequent era concerned in giving–a DAF can function a supply of legacy that you just set up.

4. Defer taxes on realized beneficial properties the place it is sensible

Whereas it is sensible to hedge towards future tax fee will increase by build up tax-free earnings sources, it might additionally make sense to keep away from paying pointless taxes now on realized beneficial properties for those who anticipate that your earnings can be drastically decrease sooner or later.

1031 Change

Possibly you need to improve your trip residence or rental property, which to procure a long time in the past at an ideal value in an ideal location that’s now value far more. Nonetheless, you’re discovering that it now not meets your loved ones’s wants.

You’ve possible taken a depreciation deduction in your taxes, which matches a good distance in lowering taxable earnings when you personal the property. However while you attempt to promote, this could present an surprising tax invoice as these deductions decrease your price foundation and improve the quantity of achieve topic to taxes at a better fee.

Structuring the sale of the present property and rolling these proceeds instantly into the acquisition of one other may very well be finished via a tax mitigating car known as a 1031 trade. This could mean you can defer the realized achieve on the unique property and keep away from paying taxes till you promote the newly bought property sooner or later.

This may be very highly effective for households who intend to maintain a property within the household for his or her kids to inherit sooner or later–the property receives a “step-up” in price foundation when inherited, which means that deferred realized achieve is eradicated. These exchanges may be finished with any funding property however will also be difficult and dear, so that they have to be thought of very fastidiously.

Certified Alternative Zone Investments

The 2017 Tax Cuts and Jobs Act established the Certified Alternative Zone (QOZ) program to offer a tax incentive for personal, long-term investments in economically distressed communities.

Traders in these packages are given a possibility to defer paying taxes on acknowledged capital beneficial properties if these beneficial properties are invested in a QOZ inside 180 days. Along with deferring beneficial properties to be realized sooner or later, there’s additionally a possibility to cut back the quantity of achieve that can be taxed. QOZs have been modified beneath the OBBBA and made everlasting with a redesigned framework that make them value revisiting.

For brand new investments made after December 31, 2026, beneficial properties may be deferred 5 years from the date of funding and taxpayers have a doable discount within the taxable achieve of 10% on the 5 12 months mark. What does this actually imply? Say you’ve $100,000 of beneficial properties from the sale of an funding on December 31, 2026 and make investments them in a QOZ inside 180 days. In 2032, 5 years after the date of the funding within the QOZ, you’ll owe taxes on $90,000 – the $100,000 initially realized much less 10%. OBBBA additionally launched new Certified Rural Alternative Funds that obtain a bigger discount in achieve of 30% at 12 months 5.

Progress on the QOZ funding itself is tax-free if held no less than 10 years. These autos aren’t with out danger–they’re illiquid and could also be speculative. Very cautious consideration needs to be given to your liquidity wants and whether or not this kind of funding is consistent with your danger tolerance and your distinctive objectives and goals.

Tax Methods: How one can Scale back Taxable Revenue for Excessive Earners

Tax planning at this stage isn’t about discovering a single intelligent transfer. It’s about understanding how every bit connects to the bigger image of your monetary life. The methods above are a place to begin for the proper dialog, not an alternative choice to one.

At Monument, your wealth strategi is constructed round precisely these sorts of high-stakes choices: surfacing what you is likely to be lacking, integrating tax pondering into each layer of your plan, and providing you with readability when it issues most. In case your monetary life has gotten extra advanced, otherwise you merely desire a sharper perspective on what you’re working with, we’d welcome the dialog.