{kind=link}

Tax-loss harvesting might be an efficient option to cut back funding earnings in a taxable portfolio, by promoting positions at a loss and reinvesting the proceeds in comparable securities (however not equivalent ones, to keep away from wash sale guidelines negating the loss) – which creates a loss for tax functions that may offset beneficial properties from elsewhere within the portfolio, whereas preserving the portfolio funds nonetheless invested and capable of take part in any additional market upside. The caveat, nonetheless, is that until new funds are continuously added to the portfolio to purchase new positions, there turns into fewer and fewer losses out there to reap over time. As a result of on common, the market tends to rise, and so in a diversified portfolio most positions will finally rise far sufficient above their value foundation that even subsequent downturns do not end in taxable losses, whereas for positions that do proceed to say no there’s solely a finite quantity of losses they will really generate (as a result of their market worth – and value foundation – can solely go right down to zero).

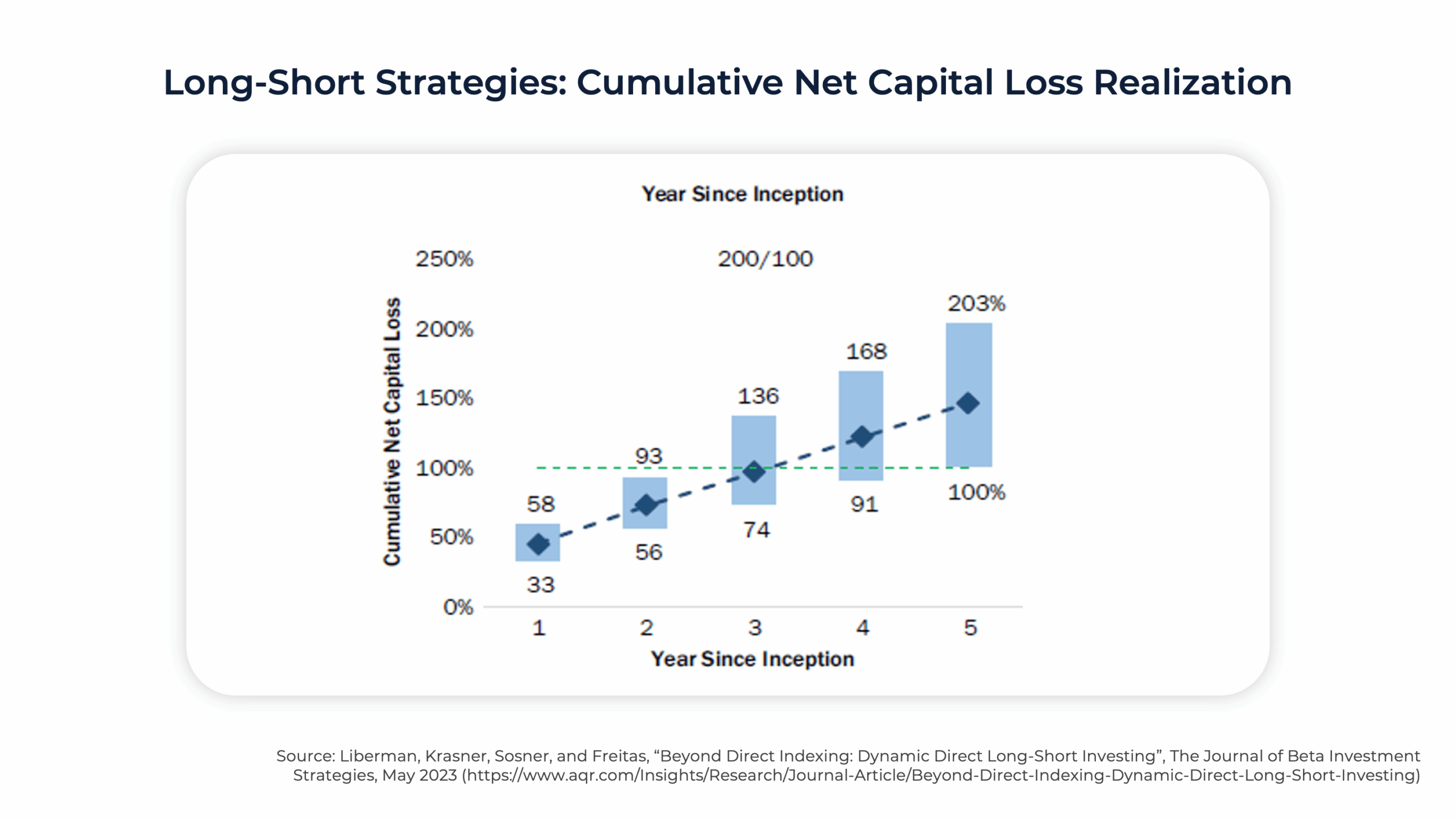

However latest years have seen the expansion in reputation of a sort of funding technique that goals to generate extra tax losses over time than commonplace portfolios, whereas nonetheless acting at or above the general market return. At its core, “Tax-Conscious Lengthy-Brief” (TALS) investing entails including leverage (i.e., borrowing) to an present portfolio to purchase extra positions and thus enhance the variety of potential losses to reap. The leverage is used for each lengthy (i.e., borrowing money to purchase equities in hopes that they will enhance in worth) and brief (i.e., borrowing equities to promote and repurchase later in hopes that they will decline) positions – which implies in idea, TALS portfolios can generate losses in each bear markets (the place the lengthy positions decline in worth) and bull markets (when the brief positions decline), whereas largely remaining economically impartial since a decline within the brief positions shall be principally offset by a rise within the lengthy positions and vice versa. And since brief positions can theoretically generate an infinite quantity of losses (since they refuse when markets rise), TALS portfolios are much less more likely to run out of losses to reap over time than commonplace long-only portfolios.

The upper tax-loss harvesting potential of TALS portfolios could make them helpful in conditions the place an investor expects to incur a considerable amount of capital beneficial properties earnings, e.g., in the event that they need to promote a highly-appreciated safety and reinvest in a extra diversified portfolio. Nevertheless, for advisors who’re contemplating TALS (e.g., managed by a subadvisor in a Individually Managed Account [SMA] portfolio), it is also vital to think about the underlying funding technique past simply the tax ramifications. As a result of tax guidelines stop TALS from being completely economically impartial, i.e., the lengthy and brief positions cannot precisely offset one another such {that a} loss on one aspect shall be totally offset by a achieve on the opposite aspect. As an alternative, they will need to have “financial substance”, which means there must be an inexpensive expectation of profitability earlier than contemplating the tax advantages of the technique. In different phrases, TALS managers cannot simply intention to precisely replicate the efficiency of a market index whereas producing no extra pre-tax return from the added leverage – they should actively attempt to outperform the market in an effort to substantiate the tax losses that they incur alongside the way in which.

Moreover, the “carrying prices” of TALS investing – which embody each charges to the TALS supervisor for managing the portfolio in addition to charges to the custodian as compensation for his or her position in lending funds on margin (for the lengthy aspect) and intermediating securities lending (for the brief aspect) – create a major baseline hurdle which TALS managers should overcome “simply” to realize market efficiency, not to mention outperformance. And the upper the leverage within the portfolio (with greater potential losses to reap), the better the carrying prices – starting from round 100bps (i.e., 1%) of the unique portfolio worth on the low finish to 400bps (i.e., 4%) or extra on the excessive finish. And with that extra leverage comes extra threat that any underperformance of the TALS portfolio shall be extra extreme than in a extra lightly-leveraged portfolio. Or put otherwise, rising leverage in a TALS technique will increase the potential tax advantages it may generate, but additionally will increase the danger that it might underperform sufficient that the investor would have been higher off merely promoting their concentrated safety and paying tax on it!

The important thing level is that TALS portfolios’ potential for uneven tax losses additionally comes with a possible for uneven financial losses. And because the reputation of TALS investing continues to extend, it is tough to know what the repercussions of occasions like brief squeezes shall be in a world the place TALS has ramped up the demand for brief positions (as custodians like Schwab and Constancy have begun to acknowledge by elevating borrowing prices and imposing varied restrictions on TALS accounts to handle their very own counterparty dangers as the first lender within the technique). And so advisors can present worth by analyzing not solely the tax impression of a possible TALS technique, but additionally how the prices and threat of the technique aligns with the consumer’s targets and their very own funding philosophy – as a result of it is one factor to generate ‘simply’ losses for tax functions, but it surely’s one other factor when these paper losses translate into actual financial losses as an alternative!