{kind=link}

Gifting immovable property—like land, plots, or homes—is tremendous frequent in India. Households typically do it out of affection, for easy succession planning, or to offer monetary help.

However not each transaction is real. Some use property presents purely for tax planning. Others create proxy possession (assume benami-style preparations). And in some instances, they’re used to keep away from taxes or cover actual possession.

Till now, these offers typically escaped correct reporting. That’s precisely what’s altering now.

Property Transactions – What’s Altering from 1 April 2026?

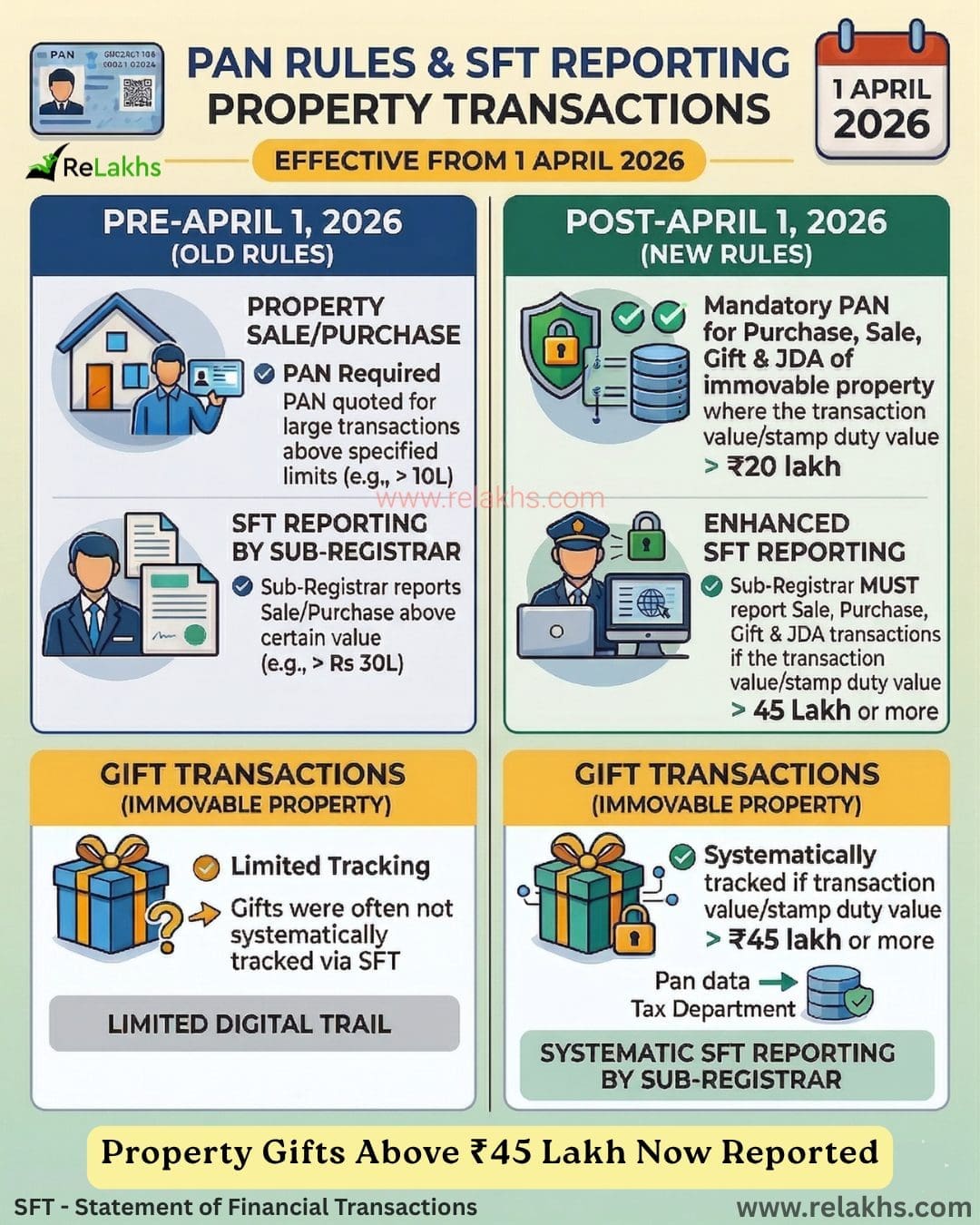

From 1 April 2026 and as per the revised SFT reporting guidelines, presents of immovable property valued above ₹45 lakh will probably be reported underneath the Assertion of Monetary Transactions (SFT). Whereas tax guidelines on presents stay unchanged, high-value transactions will now be tracked via PAN linkage, growing transparency and lowering tax evasion and proxy possession buildings.

So, Immovable property transactions will now face stricter reporting underneath the Assertion of Monetary Transactions (SFT).

Key adjustments in easy phrases:

- PAN is now obligatory for purchases, gross sales, presents, and Joint Growth Agreements (JDA) when the transaction worth or stamp responsibility worth reaches ₹20 lakh or extra.

- SFT reporting kicks in at ₹45 lakh—the place sub-registrars should report gross sales, purchases, presents, and JDAs to the Revenue Tax Division.

SFT (Assertion of Monetary Transaction) is a report filed by banks and monetary establishments to the Revenue Tax Division relating to high-value transactions linked to your PAN. It acts as a monitoring mechanism to make sure that your main investments and expenditures align together with your declared earnings.

Don’t combine up these thresholds—they serve totally different functions:

- ₹20 lakh = PAN required (that’s YOU offering it throughout the transaction).

- ₹45 lakh = SFT reporting begins (that’s the Sub-Registrar sending particulars to IT Dept).

Reward of Immovable Property Now Included in SFT

Earlier, presents of immovable property typically escaped constant monitoring with only a restricted digital path.

From April 2026, presents price ₹45 lakh+ will probably be absolutely tracked: reported by the sub-registrar, captured in SFT, linked to your PAN, and shared with the Revenue Tax Division.

What this implies: A clear digital path now exists, permitting authorities to match these transactions together with your ITR.

Tax Guidelines on Presents: No Change

The tax guidelines for property presents haven’t modified one bit—solely the monitoring has gotten stricter.

Right here’s the easy breakdown:

Presents from kinfolk (dad and mom, partner, siblings, lineal ascendants/descendants) stay absolutely tax-exempt.

Presents from non-relatives price greater than ₹50,000? Nonetheless absolutely taxable as “Revenue from Different Sources.”

Tax guidelines have NOT modified — solely monitoring and compliance have develop into stricter.

Full Particulars on Property Reward Deeds @ Property Reward Deed – All you needed to know!

The Actual Danger: Non-Disclosure & Proxy Transactions

In case your present transaction is real, you’re secure. If there’s intent to cover, the system will catch up. The largest influence is on non-disclosure and misuse.

Downside situation 1:

You obtain property ≥ ₹45 lakh from a non-relative however skip reporting it in your ITR.

Now it triggers:

Actual instance: Mr. A “presents” ₹60 lakh property to non-relative Mr. B. Mr. B doesn’t declare it.

Pre-2026: Low detection threat.

Submit-2026: Sub-registrar reviews through SFT, PANs linked → IT Dept spots undeclared asset → Tax demand + penalties.

Downside situation 2:

If somebody tries shopping for property in one other’s title and calling it a “present”: This screams proxy/benami construction—the place the actual proprietor funds it however hides behind a nominal proprietor.

Actual instance: Mr. A “presents” ₹60 lakh property to non-relative Mr. B. Mr. B doesn’t declare it.

Mr. A purchases a property price ₹25 lakh in 2024, however as an alternative of registering it in his personal title, he buys it within the title of his uncle (father’s brother), who doesn’t have robust monetary capability. For the reason that worth is beneath the sooner reporting threshold, the transaction doesn’t get captured underneath SFT at the moment.

Over the subsequent two years, the property worth will increase considerably. After 1 April 2026, when the worth reaches round ₹1 crore, the uncle presents the identical property again to Mr. A. Since presents from kinfolk are tax-free, on the floor, this appears like a wonderfully legitimate transaction.

Nonetheless, with the brand new SFT guidelines in place, this high-value present (above ₹45 lakh) will get reported and linked to PAN. The tax division can now see your complete path — from the unique buy to the ultimate switch.

This raises apparent questions: How did the uncle initially afford the property? Who really funded the acquisition? Why is the property being transferred again?

Regardless that the construction appears legitimate (present from a relative), the substance of the transaction suggests a proxy association.

Conclusion: Transparency is the brand new regular.

From April 2026, property presents of ₹45 lakh or extra will depart a clear digital path via SFT reporting by the sub-registrar, and the transaction will even be linked to PAN and shared with the Revenue Tax Division.

The general shift is straightforward: higher transparency and better compliance. For real presents, particularly these obtained from kinfolk, there may be normally no situation. But when the transaction is undisclosed or structured in a suspicious approach, the chance of notices and penalties goes up considerably.

Proceed studying:

(Submit first revealed on: 11-April-2026)