{kind=link}

My retirement planning for the previous two years since retiring has centered on the Bucket Strategy to have the suitable funds in the suitable funding buckets to have high-risk adjusted returns whereas minimizing taxes over my lifetime. This text focuses on forty of the highest performing ETFs that I consider can type a superb basis for the approaching decade. I wrote Investing in 2025 And the Coming Decade describing why I feel bonds will outperform shares on a risk-adjusted foundation as a result of rates of interest must keep greater for longer to finance the nationwide debt and beginning fairness valuations are so excessive. Federal Reserve Chairman Jerome Powell principally mentioned as a lot this previous Wednesday and the S&P 500 dropped 3%.

I rated over 5 hundred ETFs that I observe in over 100 Lipper Classes, utilizing the MFO Threat and Ranking Composites, Ferguson Mega Ratio which “measures consistency, danger, and expense adjusted outperformance”, Return After-Tax Submit Three 12 months Ranking, and the Martin Ratio (risk-adjusted efficiency) to pick the highest fund for every Lipper Class. I then subjectively adjusted the funds to favor the Nice Owls and for my very own preferences of Fund Households. I eradicated the Lipper Classes the place the ultimate fund had a excessive price-to-earnings ratio and fell additional than the S&P 500 following Mr. Powell’s announcement. I used the Factset Ranking System to get rid of a number of funds. I eradicated nearly twenty funds to maintain the ultimate record of funds to maintain the choice diversified and easy.

What Will the Investing Surroundings Usher in The Subsequent Decade?

The approaching decade will convey uncertainty as a result of:

- Nationwide debt as a proportion of gross home product (GDP) has not been this excessive since World Battle II.

- Federal Debt as a proportion of (GDP) is rising at six p.c including to the nationwide debt.

- Inhabitants progress which drives financial progress has slowed for many years.

- Tax cuts are coming and are more likely to scale back Federal income with advantages favoring the rich and including to the nationwide debt.

- Tariffs increase the price of inflation favoring holding charges greater for longer.

- Inventory valuations are excessive implying under common long-term returns.

- Rates of interest will possible be elevated in comparison with historic averages to be able to finance the nationwide debt and comprise inflation.

- Geopolitical danger has risen.

- Political brinkmanship has risen.

For concepts about the best way to put together for extra unstable markets, I refer you to David Snowball’s article final month, “Constructing a chaos-resistant portfolio”, in addition to mine, “Envisioning the Chaos Protected Portfolio”. The choice of ETFs on this article displays a few of these concepts from the MFO December publication.

Bucket Strategy

The Bucket Strategy is an easy idea of segregating funds into three classes to fulfill short-, intermediate-, and long-term spending wants. It may be extra difficult in a dual-income family with separate account possession, and totally different tax traits. For these in greater tax brackets, asset location to handle taxes is essential.

For instance, if an investor owns each Conventional and Roth IRAs, then funds with decrease progress and fewer tax effectivity ought to be put into the Conventional IRAs. Roth IRAs are perfect for greater progress funds which are much less tax-efficient. After-Tax accounts held for the long run are finest fitted to tax-efficient “purchase and maintain” funds with low dividends and better capital positive factors.

These are the ideas included within the following buckets. Traders want to pick what is acceptable for his or her particular person circumstances. Some funds can match comfortably into a number of buckets or accounts with totally different tax traits.

I prepare my accounts so as of which of them I’ll withdraw cash from first. The primary ones are probably the most conservative and the final ones are probably the most aggressive. I want to contemplate these being in Funding Buckets. On the day that the S&P 500 fell 3%, my accounts that may fund the following ten years of residing bills fell 0.35% whereas producing revenue.

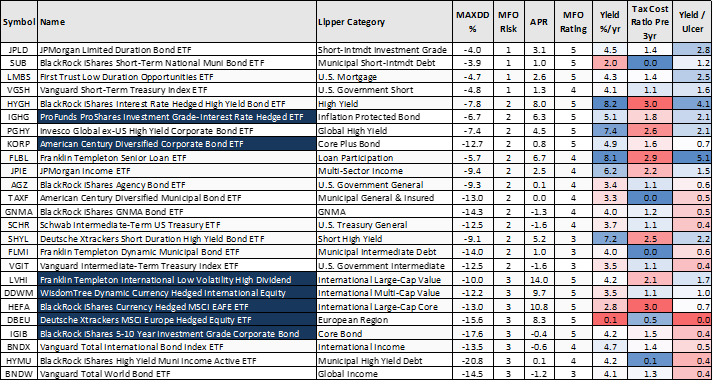

Bucket #1 – Security and Residing Bills for Three Years

The record of funds in Bucket #1 is brief as a result of I used fund efficiency in 2022 and the COVID recession to push funds with excessive drawdowns into Bucket #2. Cash market funds, certificates of deposit, and bond ladders ought to be thought of a staple of a conservative bucket for emergencies and residing bills. The Tax Value Ratio displays the portion of the returns that can be misplaced on account of taxes. The upper one’s tax brackets, the extra relevant it turns into to put money into municipal bonds. For an investor wanting to reduce taxes, BlackRock iShares Quick Maturity Municipal Bond Energetic ETF (MEAR) could also be an amazing selection.

The blue shaded cells signify a Nice Owl Fund which has “delivered prime quintile risk-adjusted returns, based mostly on Martin Ratio, in its class for analysis intervals of three, 5, 10, and 20 years, as relevant.”

Bucket #1 – Security and Residing Bills for Three Years

Supply: Writer Utilizing MFO Premium fund screener and Lipper world dataset.

Bucket #2 – Intermediate (three to 10 years) Spending Wants

There’s a crucial distinction between MFO Threat and MFO Ranking. MFO Threat relies on danger as measured by the Ulcer Index which is a measure of the depth and length of a drawdown. MFO Threat applies to all funds. MFO Ranking is the quintile score of risk-adjusted efficiency as measured by the Martin Ratio for funds with the identical Lipper Class.

I lately modified my funding technique for Bucket #2 from Whole Return to Revenue as a result of rates of interest are traditionally excessive. Within the desk under, I calculate the Yield to Ulcer ratio to see how a lot danger I is likely to be taking for that revenue. The danger over the previous three years has come from rising charges and the anticipation of a recession which can have reworked right into a gentle touchdown. I count on rates of interest to stay comparatively excessive for longer however progressively fall. I favor bonds with intermediate durations.

Bond portfolios ought to be top quality, however riskier bond funds could be added to diversify for greater revenue or complete return. Excessive Yield, Mortgage Participation, and Multi-Sector Revenue funds carry extra danger than high quality bond funds however are usually much less dangerous than fairness funds.

A number of Worldwide Fairness Funds make it into Bucket #2 as a result of the valuations are decrease and so they have decrease volatility. Franklin Templeton Worldwide Low Volatility Excessive Dividend Index ETF (LVHI) stands out for having a excessive yield and Yield/Ulcer ratio together with excessive returns, however it isn’t significantly tax-efficient.

Bucket #2 is the place I see probably the most alternative over the following 5 to 10 years due to excessive beginning rates of interest. I can be monitoring higher-risk bond funds and income-producing funds to doubtlessly add.

Bucket #2 – Intermediate (three to 10 years) Spending Wants

Supply: Writer Utilizing MFO Premium fund screener and Lipper world dataset.

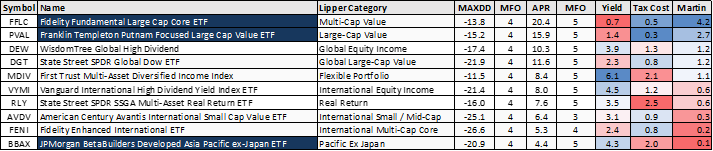

Bucket #3 – Passing Alongside Inheritance, Longevity, Development

My considerations about Bucket #3 are principally excessive valuations. The theme in Bucket #3 is progress at an inexpensive worth. Fairness funds could do effectively in 2025 and 2026 due to tax cuts. I provide fewer funds to contemplate in Bucket #3 as a result of I excluded these with excessive valuations and excessive current volatility.

I used to be considering of shopping for Berkshire Hathaway subsequent 12 months, however now favor Constancy Elementary Massive Cap Core ETF (FFLC) as an alternative.

Bucket #3 – Passing Alongside Inheritance, Longevity, Development

Supply: Writer Utilizing MFO Premium fund screener and Lipper world dataset.

Closing

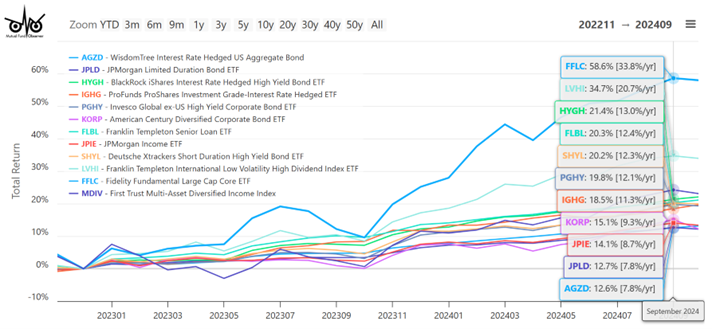

I’ve delayed making some small adjustments to my portfolio till subsequent 12 months to be able to maintain taxes decrease in 2024. I plan to make regular withdrawals from riskier investments to decrease my stock-to-bond ratio. Under is a chart of Whole Return of a few of the funds that I’m monitoring with probably the most curiosity.

Determine #1: Chosen Writer’s ETF Picks for 2025

Supply: Writer Utilizing MFO Premium fund screener and Lipper world dataset.

I want everybody and productive and nice new 12 months.