{kind=link}

After we purchase a life insurance coverage coverage, most of us begin by evaluating firms on their Declare Settlement Ratio. A few of us additionally take a look at premium charges, bonuses, or how robust the model feels.

However there’s another metric that hardly ever will get mentioned—the life insurance coverage persistency ratio.

This ratio, printed yearly by IRDAI, exhibits how constantly policyholders preserve paying their premiums after the primary 12 months. It shouldn’t be judged in isolation, however it does provide helpful clues about how nicely an insurer retains prospects over the long run.

On this article, I take a look at 10 years of official IRDAI persistency information (FY2015-16 to FY2024-25) to see how India’s main life insurers have carried out over time—and what you, as a potential policyholder, can be taught from these tendencies.

What’s the Life Insurance coverage Persistency Ratio?

The life insurance coverage persistency ratio tells you what proportion of policyholders preserve paying their renewal premiums after shopping for a coverage.

In easy phrases:

Increased persistency ratio = extra prospects proceed their insurance policies.

Regulators observe this at totally different closing dates to see what number of insurance policies stay lively:

- thirteenth month: Clients who renewed their coverage after the primary 12 months

- twenty fifth month: Clients who continued after the second 12 months

- thirty seventh month: Clients who continued after the third 12 months

- forty ninth month: Clients who continued after the fourth 12 months

- 61st month: Clients who continued after the fifth 12 months

As you progress from the thirteenth to the 61st month, these ratios often decline. That’s as a result of some policyholders cease their insurance policies alongside the best way—as a result of affordability points, modifications in revenue, shifting monetary priorities, or realizing the product doesn’t match their wants anymore.

Why Ought to You Care Concerning the Persistency Ratio?

Persistency Ratio deserves consideration as a result of it tells you one thing very totally different from the standard numbers like Declare Settlement Ratio.

A constantly greater persistency ratio can counsel that:

- Policyholders are literally sticking with their insurance policies and paying premiums over the long run.

- The merchandise are higher aligned with buyer wants and expectations.

- The continuing premium dedication is broadly manageable for many prospects.

- Buyer retention has been comparatively stronger over time.

That mentioned, a excessive persistency ratio doesn’t robotically imply an insurer is “higher”, and a decrease ratio doesn’t all the time imply poor efficiency. Product combine, buyer profile, distribution mannequin, and total enterprise technique can all affect persistency—so it’s finest used as one lens amongst many, not the one deciding issue.

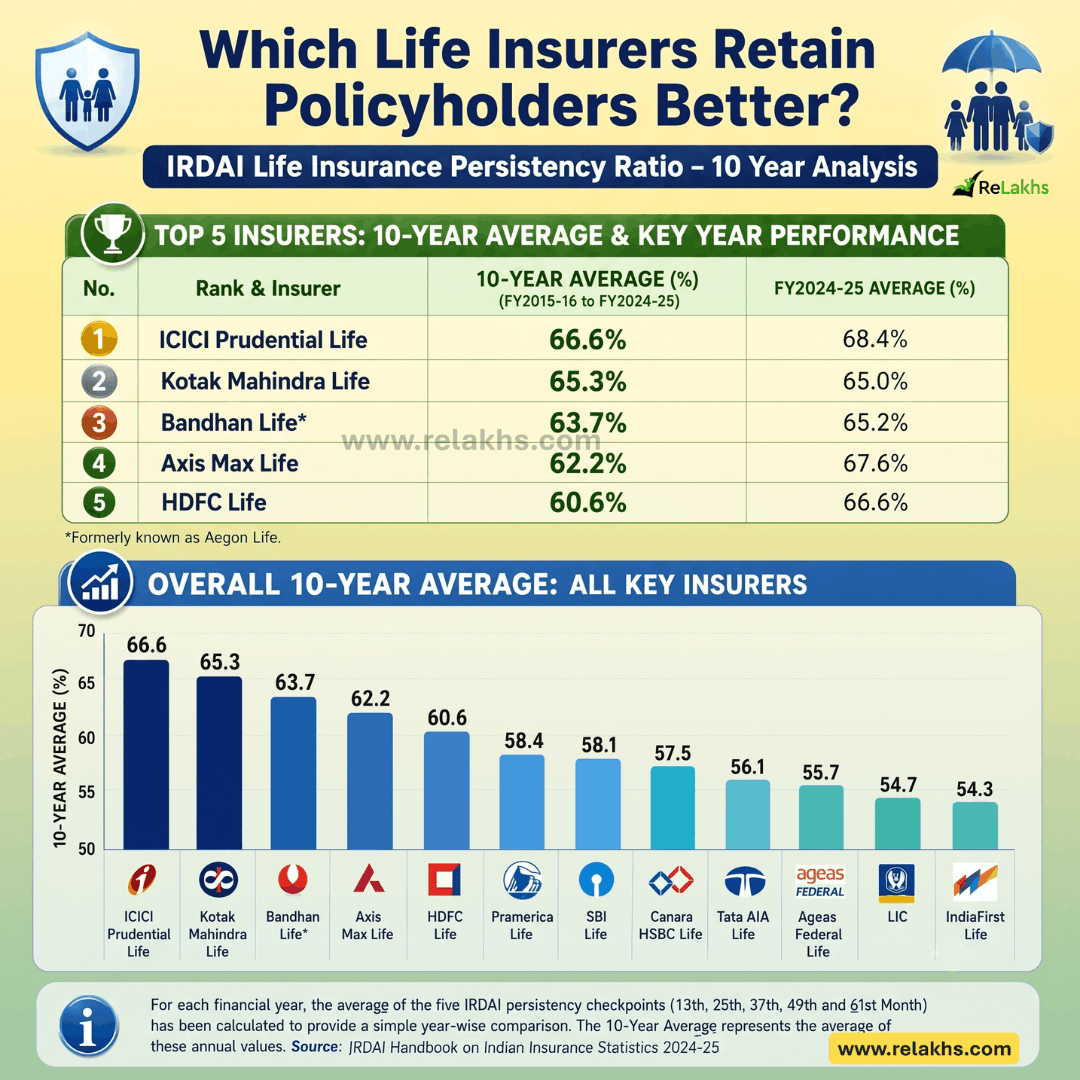

10-12 months Common Life Insurance coverage Persistency Ratios (FY2015-16 to FY2024-25)

Slightly than a single 12 months’s figures, I analyzed the final 10 years of official IRDAI information.

For every monetary 12 months, I calculated the common of the 5 persistency checkpoints (thirteenth, twenty fifth, thirty seventh, forty ninth and 61st Month). The desk beneath summarises the annual averages and the general 10-year common for every insurer.

| Rank | Life Insurer | FY16 | FY17 | FY18 | FY19 | FY20 | FY21 | FY22 | FY23 | FY24 | FY25 | 10-12 months Avg. |

| 1 | ICICI Prudential Life | 58.4 | 63.3 | 65.7 | 66.6 | 67.8 | 67.2 | 68.2 | 68.4 | 71.5 | 68.4 | 66.6 |

| 2 | Kotak Mahindra Life | 57.0 | 60.8 | 63.6 | 65.8 | 65.7 | 68.0 | 68.5 | 68.5 | 70.4 | 65.0 | 65.3 |

| 3 | Bandhan Life* | 51.3 | 54.4 | 59.8 | 62.2 | 63.4 | 68.4 | 71.3 | 72.0 | 69.0 | 65.2 | 63.7 |

| 4 | Axis Max Life | 55.0 | 58.8 | 60.6 | 61.8 | 63.8 | 61.4 | 62.2 | 64.2 | 67.0 | 67.6 | 62.2 |

| 5 | HDFC Life | 57.1 | 58.6 | 58.4 | 58.6 | 57.9 | 58.7 | 61.9 | 63.1 | 65.0 | 66.6 | 60.6 |

| 6 | Pramerica Life | 28.1 | 37.3 | 43.6 | 52.1 | 74.9 | 78.1 | 79.4 | 62.1 | 63.4 | 64.8 | 58.4 |

| 7 | SBI Life | 48.9 | 51.8 | 54.2 | 55.7 | 56.5 | 57.9 | 60.5 | 63.9 | 65.7 | 65.8 | 58.1 |

| 8 | Canara HSBC Life | 43.9 | 48.1 | 51.1 | 54.9 | 57.3 | 60.1 | 61.8 | 64.1 | 66.1 | 67.5 | 57.5 |

| 9 | Tata AIA Life | 40.1 | 43.3 | 46.6 | 51.1 | 55.8 | 56.1 | 61.4 | 66.0 | 69.2 | 71.1 | 56.1 |

| 10 | Ageas Federal Life | 56.4 | 54.1 | 54.3 | 57.2 | 55.9 | 58.1 | 54.4 | 53.8 | 54.9 | 57.5 | 55.7 |

| 11 | LIC | 52.4 | 53.0 | 54.6 | 56.2 | 52.2 | 56.0 | 56.0 | 55.8 | 55.8 | 55.0 | 54.7 |

| 12 | IndiaFirst Life | 47.1 | 49.2 | 50.0 | 50.5 | 52.6 | 53.3 | 63.0 | 64.1 | 57.2 | 55.9 | 54.3 |

Notice: The ten-12 months Persistency Evaluation is an impartial evaluation based mostly on official IRDAI information and is meant for instructional functions. It’s not an official IRDAI rating. * Bandhan Life contains the historic information of its predecessor entity as mirrored within the IRDAI Handbook. Previously referred to as Aegon Life.

For instance, if an insurer has a 10-12 months Common Persistency Ratio of 60%, it broadly signifies that, on common, round 60% of the eligible policyholders continued paying their renewal premiums throughout the 5 persistency checkpoints during the last decade, whereas the remaining policyholders discontinued their insurance policies at totally different phases.

Normally, the next persistency ratio is taken into account higher, because it suggests {that a} bigger proportion of policyholders continued their insurance policies over the long run.

Key Observations

A couple of attention-grabbing tendencies emerge from the 10-year evaluation:

- Lengthy-term consistency is extra significant than a single 12 months’s efficiency – An insurer could carry out exceptionally nicely in a single explicit 12 months, however analysing a decade of knowledge gives a a lot better image of long-term buyer retention.

- ICICI Prudential and Kotak Mahindra Life have proven robust long-term consistency – Based mostly on the 10-year common, these insurers have maintained comparatively robust persistency during the last decade.

- Tata AIA has proven exceptional enchancment – Though Tata AIA’s long-term common is decrease than some friends due to its earlier years, its annual persistency averages have improved considerably in recent times, reaching 71.1% in FY2024-25.

- LIC has remained comparatively steady – LIC’s annual averages have remained inside a reasonably slender vary during the last decade, indicating comparatively steady buyer retention regardless of its huge and numerous buyer base.

- Persistency is just one piece of the puzzle – A better persistency ratio shouldn’t be interpreted as a suggestion to purchase a coverage from a selected insurer. It’s merely one other parameter that may provide help to higher perceive long-term buyer retention.

Ought to Persistency Ratio Affect Your Selection of Life Insurer?

Sure—however solely as certainly one of a number of components. When evaluating life insurance coverage firms, additionally take into account:

- Declare Settlement Ratio

- Solvency Ratio

- Product options

- Premium affordability

- Customer support

- Your monetary objectives

Consider the Persistency Ratio as a further indicator relatively than a last verdict.

Closing Ideas

The IRDAI Life Insurance coverage Persistency Ratio affords precious perception into how constantly policyholders proceed their life insurance coverage insurance policies over time. As a substitute of specializing in a single 12 months’s numbers, analyzing a decade of knowledge helps determine broader tendencies and gives a extra balanced perspective on buyer retention.

As a potential policyholder, use the Persistency Ratio alongside different necessary metrics such because the Declare Settlement Ratio, product suitability, and premium affordability earlier than making your choice.

In spite of everything, the very best life insurance coverage coverage isn’t only one that you simply purchase—it’s one that you could comfortably proceed till it achieves its supposed function.

Proceed studying:

(Publish first printed on : 02-July-2026)

Disclaimer: The evaluation and observations shared on this article are based mostly on publicly obtainable IRDAI information and are supposed solely for instructional functions. At all times consider a number of components—together with product suitability, Declare Settlement Ratio, Solvency Ratio, options, and your personal monetary wants—earlier than selecting a life insurance coverage coverage or insurer.