{kind=link}

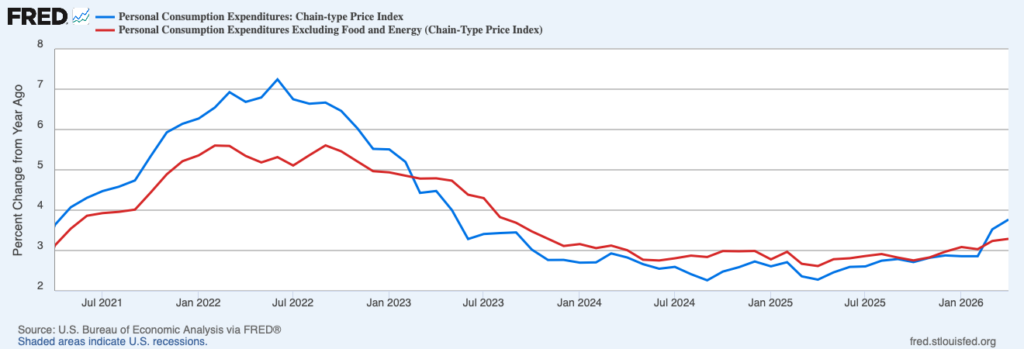

The battle within the Center East has pushed costs larger this 12 months. However the newest information from the Bureau of Financial Evaluation suggests the worst of the worth hikes could also be within the rear-view mirror. The Private Consumption Expenditures Value Index (PCEPI), which is the Federal Reserve’s most popular measure of inflation, grew at an annualized fee of 4.9 p.c in April 2026, down from 8.3 p.c within the prior month. The PCEPI grew at an annualized fee of 4.8 p.c over the past six months and three.8 p.c over the past 12 months.

Determine 1. Headline and Core Private Consumption Expenditures Value Index Inflation, April 2021 – April 2026

Core inflation, which excludes meals and power costs and is considered a greater gauge of the underlying fee of inflation, additionally declined. Core PCEPI grew at an annualized fee of two.9 p.c in April 2026, down from 3.6 within the prior month. It grew at an annualized fee of three.8 p.c over the past six months and three.3 p.c over the past 12 months.

Though inflation has declined on a month-over-month foundation, the year-over-year fee has ticked up. Headline PCEPI inflation climbed from 3.5 p.c to three.8 p.c, whereas core PCEPI inflation elevated from 3.2 p.c to three.3 p.c. What — if something — the Fed ought to do in regards to the larger inflation relies upon largely on why inflation is above goal.

The pass-through from power costs to all the pieces else definitely explains a portion of the distinction between inflation and the Fed’s two-percent goal, and the Fed shouldn’t reply to that portion. When constrained provides — of power, or the rest — push costs larger, these larger costs assist people make applicable choices about whether or not and the way a lot of the more-scarce merchandise to purchase. Until the Fed has a secret stash of oil, pure gasoline, or fertilizer mendacity round, it received’t have the ability to enhance issues on that entrance.

Constrained provides can’t clarify the entire distinction between inflation and the Fed’s goal, nonetheless. Among the extra inflation is because of extra nominal spending. When the sum of money being spent in an financial system grows quicker than the actual worth of products and companies being produced, costs should rise. And when nominal spending development outpaces actual output development, costs rise extra quickly. Therefore, a surge in nominal spending development leads to larger inflation. To enhance issues, the Fed can convey nominal spending development again all the way down to a fee in keeping with its inflation goal and the anticipated development fee of actual output.

Over the 5 years previous he pandemic, nominal spending grew round 4.1 p.c per 12 months. Free financial coverage allowed nominal spending development to surge from 4.3 p.c for the 12 months ending 2021:Q1 to 11.3 p.c for the 12 months ending 2022:Q1. Then, because the Fed tightened financial coverage, nominal spending development declined. Nominal spending grew 7.8 p.c, 5.5 p.c, and 4.6 p.c over the three years that adopted. As nominal spending development declined, so too did inflation. Over the 12 months ending in April 2025, PCEPI inflation was simply 2.3 p.c.

Alas, that disinflationary course of has not merely stalled, however reversed. Nominal spending grew 5.9 p.c from 2025:Q1 to 2026:Q1. And, with extra money chasing after the identical quantity of products, larger nominal spending development has introduced larger inflation.

It’s tempting to attribute the rise in inflation to the salient provide shocks we’ve got skilled over the past 12 months or so, together with the tariffs levied final 12 months and the battle within the Center East starting earlier this 12 months. However right here’s the factor: constrained provides don’t push nominal spending development larger. Quite, quicker nominal spending development is the telltale signal of a demand-side drawback.

Sadly, Fed officers don’t seem to see it that manner. Because the minutes from the Federal Open Market Committee (FOMC) assembly held in April reveal, FOMC members attribute the upper inflation to the battle within the Center East, tariffs, and different supply-side components:

Individuals noticed that general inflation had moved up, partly due to latest world power value will increase, and remained above the Committee’s two p.c longer-run objective. Individuals usually famous that core inflation had additionally moved additional above two p.c. A number of members famous that the speed of enhance in core items costs remained elevated, not less than partly reflecting the results of tariffs. Some members noticed that larger gasoline costs had brought on various different costs to extend, together with delivery prices and airfares. Along with power value will increase, a number of members famous that offer disruptions related to the battle within the Center East had brought on costs for fertilizer and another non-energy commodities to rise. Some members famous that latest value will increase within the data know-how sector had contributed to larger inflation. A number of of those members remarked that, whereas value will increase within the software program class have been contributing meaningfully to the rise in core inflation, value will increase in that class might not be good predictors of future general inflation.

Moreover, they “anticipated that prime power costs would proceed to place upward strain on general inflation” and “usually anticipated that the results of tariffs on core items inflation would diminish over the course of this 12 months” as long as tariff charges aren’t “elevated above current ranges, resulting in extra upward strain on inflation.”

It’s considerably odd that FOMC members didn’t explicitly acknowledge that extra demand has additionally pushed up inflation. On the assembly, members “usually noticed that financial exercise seemed to be increasing at a strong tempo” and “usually anticipated that the tempo of actual GDP development would stay strong this 12 months.” These observations are inconsistent with a supply-driven inflation story, whereby costs rise extra quickly as actual output development slows.

FOMC members even recognized particular sources of demand on the assembly, noting “that enterprise fastened funding remained sturdy, largely reflecting energy within the know-how sector” and that “excessive ranges of family wealth and financial coverage” had supported client spending. They simply didn’t join the dots from sturdy demand to larger inflation.

There’s a silver lining, nonetheless. Regardless of suggesting inflation is essentially supply-driven, which might not sometimes warrant a financial coverage response, FOMC members thought the state of affairs “may necessitate sustaining the present coverage stance for longer than beforehand anticipated.” That change within the projected path of financial coverage quantities to a modest tightening, although in all probability not sufficient to meaningfully gradual nominal spending development. Furthermore, a “majority of members” agreed “that some coverage firming would probably grow to be applicable if inflation have been to proceed to run persistently above two p.c.” The Fed might tighten financial coverage additional, and cut back nominal spending development as a consequence, with out ever acknowledging the demand-side drawback.

Ideally, policymakers will implement the proper insurance policies for the proper causes. Barring that, nonetheless, I would definitely favor they implement the proper insurance policies for the flawed causes than implement the flawed insurance policies. There’s a danger that, by not absolutely understanding the state of affairs, Fed officers is not going to react as they need to to incoming information. However not less than they’re headed in the proper route.