{kind=link}

Gabriel India Ltd. – Redefining trip consolation

Gabriel India Restricted is a Tier-1 automotive elements producer and the flagship listed firm of the ANAND Group, headquartered in Pune and tracing its origins to 1961. It’s India’s market chief in trip management merchandise and ranks among the many prime ten suspension producers globally, with a portfolio spanning shock absorbers, struts, entrance forks, and seat and cabin dampers. The corporate is among the few home gamers with a sizeable presence throughout each automotive section – two- and three-wheelers, passenger automobiles, industrial autos and railways – backed by a deep aftermarket portfolio and a rising export presence throughout six continents. Manufacturing is carried out throughout seven vegetation situated in key automotive hubs nationwide, supported by three R&D centres, together with know-how centres at Hosur and Chakan and the Gabriel Europe Engineering Centre (GEEC) in Belgium.

Merchandise and Companies

The corporate supplies big selection of trip management merchandise – shock absorbers, entrance forks, mono shox, strut meeting, dampers (axle, cabin & seat) catering to 2-3 wheelers (2W & 3W), passenger autos (PV), industrial car (CV), off freeway and railways.

Subsidiaries: As of FY25, the corporate has 2 wholly owned subsidiaries.

Funding Rationale

- ANAND Group’s Strategic Repositioning of Gabriel as its Automotive Progress Engine – ANAND Group has articulated an bold goal of ₹50,000 crore in revenues by 2030, with Gabriel India designated as the first automotive development engine to drive that ambition. As soon as a single-product suspension specialist, Gabriel is being systematically repositioned as a diversified mobility options supplier by means of a composite scheme of association authorised by the board in FY26, which includes the amalgamation of Anchemco India into Asia Investments Non-public Restricted (AIPL) and the next demerger of AIPL’s automotive enterprise into Gabriel. This restructuring brings in publicity to brake fluids, radiator coolants, diesel exhaust fluid (DEF/AdBlue), and PU/PVC-based adhesives broadening Gabriel’s product canvas nicely past its suspension roots. The group has concurrently strengthened Gabriel’s technical credentials by means of an asset buy settlement with Marelli Motherson Auto Suspension (MMAS), alongside a licence and technical help settlement with Marelli Suspension Methods, Italy – strikes that deepen Gabriel’s suspension capabilities whereas enhancing its competitiveness throughout OEM platforms. The lubricants and practical fluids section provides additional strategic depth by means of a JV with SK Enmove, a globally recognised participant within the area. Collectively, these initiatives replicate a deliberate group-level determination to consolidate automotive manufacturing capabilities beneath Gabriel, reworking it from a element provider right into a multi-product platform with a presence throughout suspension, practical fluids, sunroofs, and fasteners.

- New Enterprise Wins and Strategic Partnerships Increase the Income Addressable Market – Gabriel’s pivot to a multi-product firm is gaining tangible traction by means of a collection of recent enterprise wins and three way partnership partnerships throughout adjoining mobility segments. Within the sunroof section, Inalfa Gabriel Sunroof Methods (IGSS) posted income of ₹107 crore with an EBITDA margin of 13.5% in Q3FY26, and bought roughly 1,70,000 models in FY26, with administration guiding for utilisation enchancment to 60 – 70% on present manufacturing strains. On new buyer wins, IGSS secured enterprise with Hyundai for 3 extra mannequin variants, with anticipated volumes of 1,30,000 models every year translating to an annual turnover of roughly ₹120 crore; begin of manufacturing is focused for December 2027. Within the two-wheeler section, Gabriel made inroads into Hero MotoCorp, with begin of manufacturing anticipated in Q2FY27, whereas additionally securing its first improvement order in e-bike forks for a European buyer, with manufacturing anticipated to start round Q3FY27. The photo voltaic damper alternative provides a brand new non-automotive development vector with the worldwide photo voltaic damper market is estimated at USD 160 million in 2026, rising at a CAGR of 16% by means of 2034, and Gabriel has already received orders from three prospects throughout home and export geographies, with samples submitted for validation. In fasteners, the JV with South Korea’s Jinhap (affiliate of JINOS) with Gabriel holding a 51% controlling stake, making Jinhap Gabriel Auto India a subsidiary efficient February 2026 – targets each anchor buyer localisation wants and the broader Indian fasteners market. Throughout photo voltaic dampers and e-bike forks, manufacturing ramp-up is anticipated from FY27, including near-term income visibility to what’s an more and more diversified order pipeline.

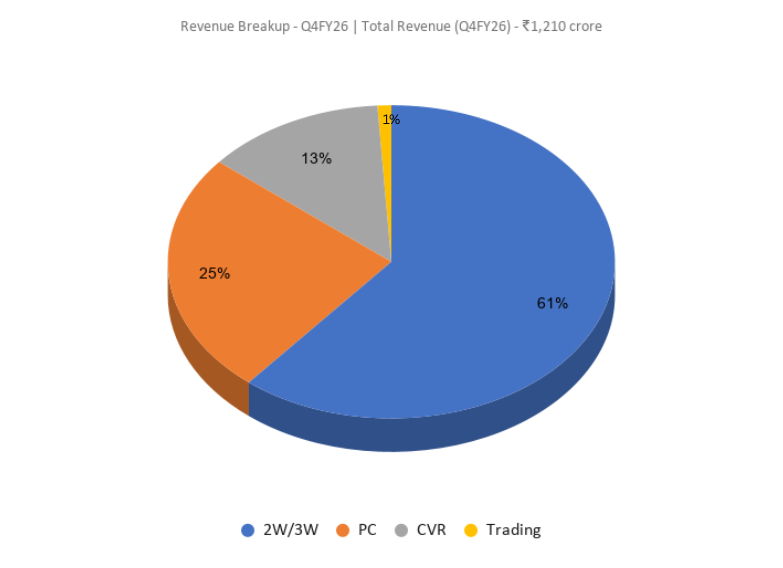

- Q4FY26 – In the course of the quarter, the corporate reported consolidated income of ₹1,210 crore, up 12.7% YoY from ₹1,073 crore in Q4FY25 (and up 2.6% QoQ). EBITDA rose to ₹117 crore, up 6.5% from ₹110 crore within the corresponding quarter, with EBITDA margin at 9.7% (versus 10.2% in Q4FY25). Internet revenue, adjusted for distinctive objects, stood at ₹67 crore, up 3.9% YoY from ₹64 crore in Q4FY25. The softer revenue development mirrored weaker sunroof-subsidiary income (the Kia Syros ramp-down) and the sooner sunroof royalty impression, alongside material-cost inflation, partly offset by operational and sourcing efficiencies.

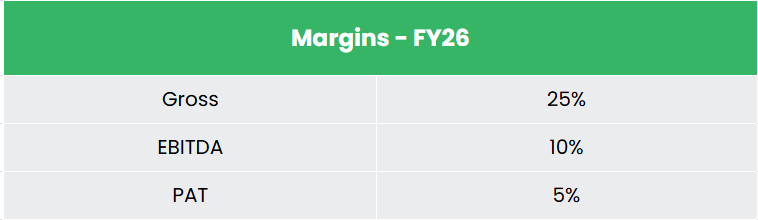

- FY26 – Throughout FY26, the corporate generated consolidated income of ₹4,667 crore, a rise of 14.9% over FY25. EBITDA stood at ₹452 crore, up 15.3% YoY, with EBITDA margin at 9.7%. The corporate reported a internet revenue of ₹252 crore (₹266 crore adjusted for distinctive objects, up ~8.6% YoY).

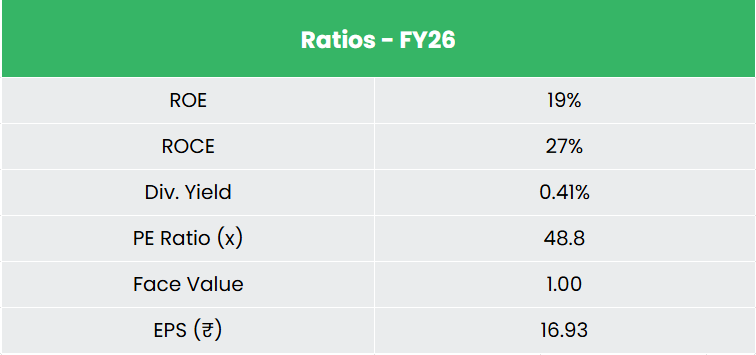

- Monetary Efficiency – The three-year income and internet revenue CAGR stands at 13% and 24% respectively between FY24-26. The corporate has a debt-to-equity ratio of 0.03. The three-year common ROE and ROCE are round 20% and 26% for the FY24-26 interval.

Trade

India’s auto elements sector stays among the many fastest-growing pillars of the nation’s manufacturing economic system, supported by a younger workforce, rising disposable incomes and the continued realignment of world provide chains towards India. Trade turnover stood at ₹6,73,557 crore (US$ 80.2 billion) in FY25, having compounded at roughly 10% over FY20 – 25, with home OEM provides contributing ~66% of turnover, the aftermarket ~11% and exports ~22%. The federal government’s manufacturing self-reliance and import-substitution push continues to strengthen home suppliers, with India more and more serving as a sourcing base for world OEMs given its price competitiveness and proximity to key markets throughout ASEAN, Europe, Japan and Korea. The trade is projected to succeed in US$ 200 billion by 2030, with exports envisaged to triple towards US$ 60 billion and India’s share of the worldwide automotive worth chain rising from ~3% to ~8%. Electrification is a central structural driver – EV gross sales reached 2.05 million models in FY25 and the federal government targets 30% EV penetration by 2030 – lifting demand for superior elements and content material per car because the home car parc expands towards 430 – 435 million models by 2030.

Progress Drivers

- 100% FDI is permitted beneath the automated route for auto-component manufacturing, supporting capability build-out and the localisation of world Tier-1 provide chains in India.

- Below GST 2.0, efficient 22 September 2025, GST on small automobiles and bikes as much as 350cc was reduce from 28% to 18% (with three-wheelers additionally at 18% and EVs retained at 5%), reviving mass-market two-wheeler and passenger-vehicle demand – the restoration administration cited as a key driver of FY26 volumes.

- Electrification and manufacturing incentives – the ~US$ 1.3 billion PM E-DRIVE scheme and the ~US$ 3.49 billion (₹25,938 crore) PLI-Auto scheme spanning FY23 – FY27 – proceed to underpin EV adoption and advanced-component localisation, aligned with the 30% EV-penetration-by-2030 ambition.

Peer Evaluation

Rivals: Sona BLW Precision Forgings Ltd, Endurance Applied sciences Ltd and so forth.

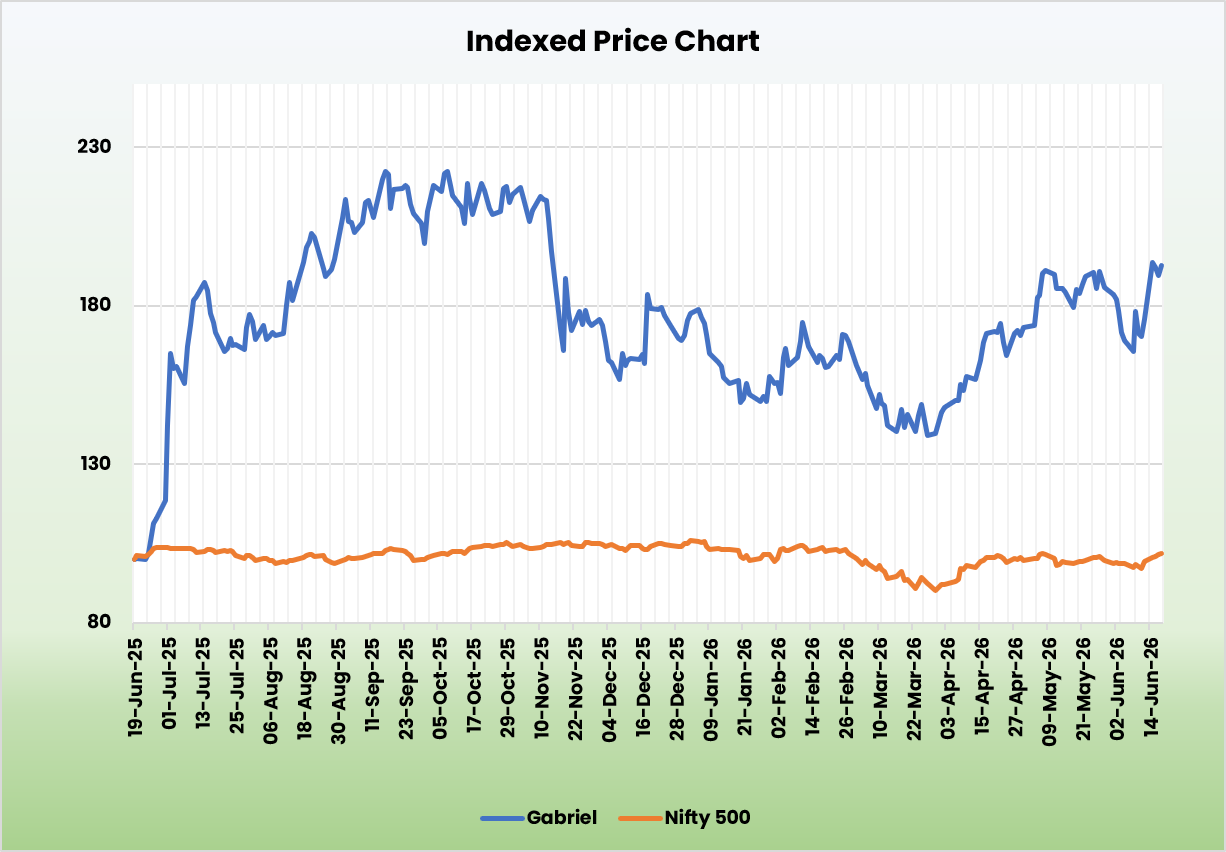

In contrast with its peer set, the corporate affords a superior return profile and best-in-class asset effectivity, generated on an asset-light, near-debt-free steadiness sheet.

Outlook

Gabriel India’s ongoing transformation right into a multi-product, multi-segment automotive elements firm types the cornerstone of its medium-term development narrative. The composite scheme of association positions the corporate as the first car for ANAND Group’s said ₹50,000 crore income goal by 2030. A broader product portfolio is anticipated to deepen OEM relationships, improve cross-selling alternatives, and strengthen Gabriel’s aftermarket presence – segments that sometimes carry superior margins relative to OEM provide. Capex steerage of ₹150 – 180 crore for FY27 indicators continued funding in capability and functionality forward of anticipated quantity ramp-ups throughout sunroofs, fasteners, photo voltaic dampers, and e-bike forks. With a number of new enterprise wins translating into outlined manufacturing timelines and the JV ecosystem progressively contributing to consolidated revenues, Gabriel’s earnings trajectory over FY27 – 28 is supported by a mix of natural quantity development and inorganic portfolio growth.

Valuations

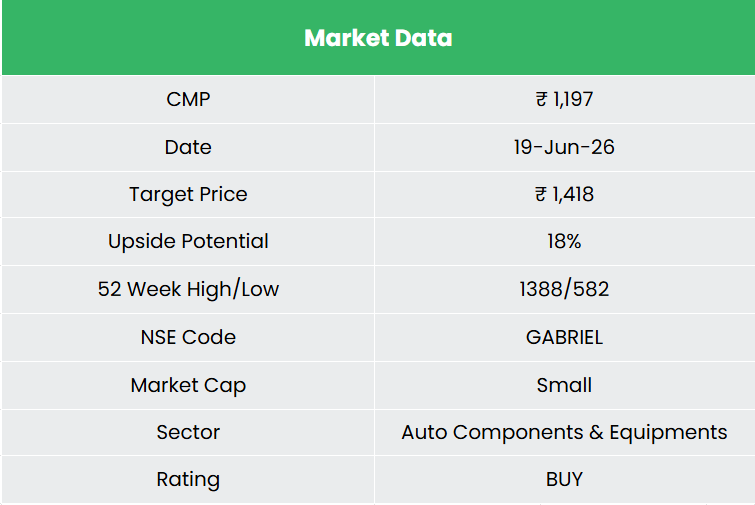

We imagine Gabriel’s development trajectory is anticipated to stay strong, underpinned by robust market demand, long-standing OEM relationships, constant income visibility, and a rising share of premium product choices. We suggest a BUY score within the inventory with the goal value (TP) of ₹1,418, 33x FY28E EPS. We additionally encourage sustaining a stop-loss at 20% from the entry value to handle potential draw back threat successfully.

SWOT Evaluation

| Energy | Weak spot |

|

|

| Alternatives | Threats |

|

|

Disclaimer: Investments within the securities market are topic to market dangers, learn all associated paperwork rigorously earlier than investing. Securities quoted listed here are exemplary, not recommendatory. Please seek the advice of your monetary advisor earlier than investing. Please be aware that we don’t assure any assured returns for the securities quoted right here.

Analysis disclaimer: Funding within the securities market is topic to market dangers. Learn all of the associated paperwork rigorously earlier than investing. Registration granted by SEBI, and certification from NISM by no means assure the efficiency of the middleman or present any assurance of returns to traders.

For extra particulars, please learn the disclaimer.

Different articles you might like

Publish Views:

134