{kind=link}

Are you aware how Gold & Silver ETF and Mutual Fund NAV is valued every day? SEBI modified this gold valuation rule from April 2026. Here’s what modified and why.

Most traders have by no means considered this. You purchase a Gold ETF. You watch the NAV go up and down with gold costs. You’re feeling all the pieces is working because it ought to. However have you ever ever stopped and requested your self — which gold value is my fund truly every single day to calculate my NAV?

The worth your native jeweller quotes? The worth in your cellphone’s information app? The worth on MCX? Or one thing else solely? Right here is the reply.

Till March 31, 2026, your Indian Gold ETF was a value fastened each morning in London. In US {Dollars}. By a world organisation sitting hundreds of miles away — one which has nothing to do with Indian taxes, Indian import duties, or Indian gold demand. Does that sound odd to you? It did to SEBI too.

That’s precisely why, from April 1, 2026, SEBI has modified how bodily gold and silver held by Indian mutual fund schemes are valued — changing an advanced London-linked technique with one thing way more logical, clear, and genuinely Indian.

Let me stroll you thru the entire thing from scratch. No jargon. Plain language. Simply the details you want to know as an investor.

Do You Know How Gold & Silver ETF and Mutual Fund NAV Is Valued?

What Is NAV? Why Does the Valuation Technique Even Matter?

Allow us to begin from the very starting, as a result of all the pieces else builds on this.

NAV stands for Web Asset Worth. It’s merely the value of 1 unit of your mutual fund or ETF on any given day. If you happen to maintain 10 items of a Gold ETF and in the present day’s NAV is Rs.600, your funding is value Rs.6,000 that day.

A Gold ETF holds bodily gold in your behalf. A Silver ETF holds bodily silver. So naturally, when gold costs rise, your NAV rises. When gold costs fall, your NAV falls.

That half is straightforward. However right here is the query no person asks — which gold value does the fund use to reach at that NAV determine each single night? That’s the place the actual story begins. And that’s what SEBI has now utterly modified.

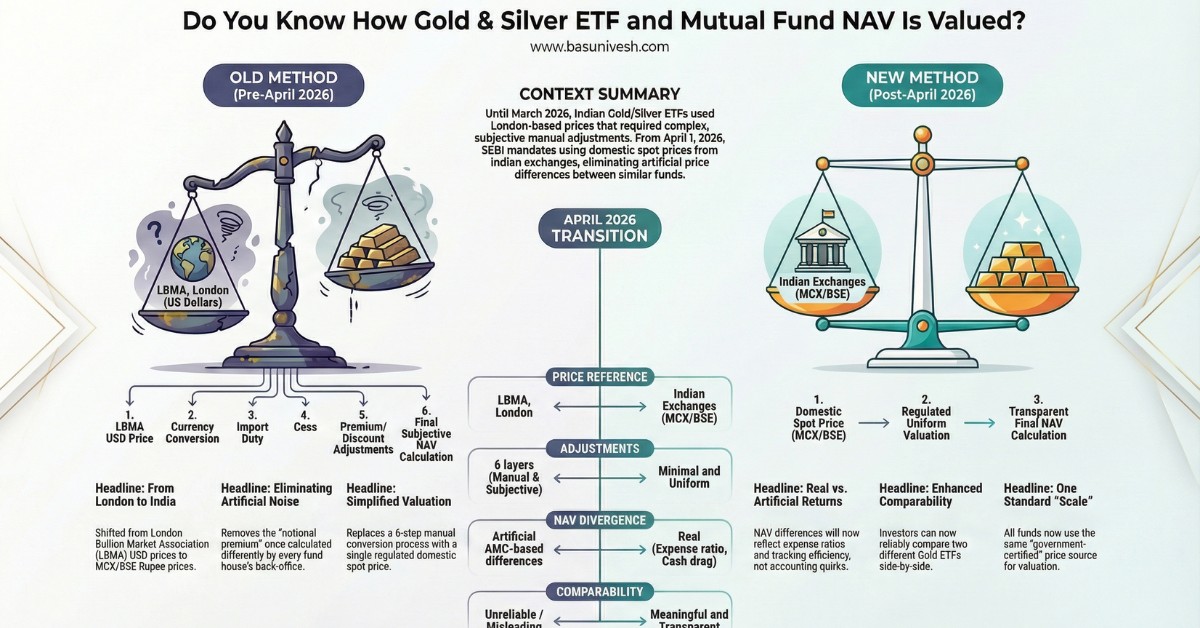

The Previous Technique — Your Indian Gold Was Being Priced in London Each Morning

Till March 31, 2026, each Gold ETF and Silver ETF in India valued their bodily holdings utilizing a value revealed by a world physique referred to as the London Bullion Market Affiliation — LBMA for brief.

The LBMA is a London-based organisation that publishes gold and silver costs twice a day — as soon as within the morning (referred to as AM fixing) and as soon as within the afternoon (PM fixing). Indian fund homes have been selecting up that AM fixing value each morning as the place to begin for calculating your NAV.

Now right here is the place the issue begins.

That LBMA value is in US {Dollars} per troy ounce. India doesn’t commerce gold in {dollars}. India doesn’t measure gold in troy ounces. And the value of gold in India is closely formed by customs obligation, native taxes, transportation prices, and home demand — none of which London is aware of or cares about.

So each fund home needed to carry out the next chain of changes each single day — manually — earlier than they might arrive at a NAV determine in your fund:

Step 1 — Convert US {Dollars} into Indian Rupees utilizing that day’s change fee

Step 2 — Convert troy ounces into grams since we measure gold in grams in India

Step 3 — Add customs obligation since gold imported into India attracts important import obligation

Step 4 — Add transportation and insurance coverage prices concerned in bodily bringing gold to India

Step 5 — Add all relevant taxes and levies

Step 6 — Add or subtract a “notional premium or low cost” — every fund home’s personal inside estimate of present Indian market circumstances

Now please learn Step 6 once more slowly.

That final adjustment had completely no commonplace rule behind it. No regulator advised the AMC what this quantity needs to be. Every fund home made its personal inside estimate, utilizing its personal inside logic. SBI Mutual Fund used one quantity. HDFC Mutual Fund used a unique quantity. Nippon used yet one more. Each AMC was basically doing its personal back-of-the-envelope calculation to reach at an Indian value.

What Drawback Did This Really Create For You as an Investor?

Right here is the place issues get genuinely unfair — and most retail traders by no means even realised it was occurring.

Think about two Gold ETFs sitting aspect by aspect in your funding app — Fund A from ABC and Fund B from XYZ. Each maintain precisely the same amount of bodily gold per unit. Identical gold. Identical purity. Identical amount. No distinction by any means in what they really maintain.

Below the outdated LBMA technique:

- ABC’s back-office workforce applies a notional premium of, say, Rs.5 per gram of their inside calculation

- XYZ’s back-office workforce applies a notional premium of Rs.8 per gram of their inside calculation

Outcome? XYZ’s Fund NAV seems Rs.3 larger than ABC’s Fund NAV in your display — not as a result of XYZ holds higher gold, not as a result of XYZ is a extra environment friendly fund, however just because their back-office workforce used a unique inside quantity that day.

You, as an investor, take a look at each funds in your app and naturally assume one is outperforming the opposite. You would possibly even contemplate switching funds. However that assumption can be utterly fallacious. It was simply a synthetic accounting distinction — one which had completely nothing to do with precise fund high quality or actual gold costs.

Niranjan Avasthi, Senior VP at Edelweiss Mutual Fund, confirmed this actual drawback: some ETFs used to account for the distinction between LBMA costs and precise Indian market costs, and a few didn’t — resulting in valuation divergence throughout fund homes for a similar underlying asset.

Let me provide you with a easy on a regular basis instance to make this crystal clear.

Think about two retailers on the identical road, each promoting the very same 100 grams of gold. You stroll into Store A — their weighing scale exhibits 98 grams. You stroll into Store B — their weighing scale exhibits 103 grams. Each scales are weighing the identical gold. However every shopkeeper calibrated their very own machine in another way. You can’t belief both studying. You definitely can not evaluate the 2 retailers pretty based mostly on these readings.

That’s precisely what was occurring with Gold ETF NAVs throughout totally different fund homes in India. Completely different inside calibration. Identical underlying gold. Fully deceptive comparability for unusual traders such as you and me.

The New Rule — India’s Personal Worth, From April 1, 2026

SEBI, after holding discussions with the Mutual Fund Advisory Committee (MFAC), looking for public suggestions, and consulting all market stakeholders, determined this needed to cease.

As per SEBI Round No. HO/(68)2026-IMD-POD-2/I/5780/2026 dated February 26, 2026, from April 1, 2026, all mutual funds should now worth their bodily Gold and Silver utilizing polled spot costs revealed by recognised Indian inventory exchanges.

Which Indian inventory exchanges? Particularly, exchanges which might be already used for the settlement of bodily delivered Gold and Silver derivatives contracts in India — at present, MCX (Multi Commodity Alternate of India) and BSE are among the many exchanges offering such polled spot costs.

Now what’s a “polled spot value”? In easy phrases — MCX goes out to a large cross-section of precise market contributors — merchants, sellers, jewellers — and gathers their value quotes for gold and silver from recognized market centres throughout India. It then arrives at a consultant home spot value from all these real-world inputs. This value displays what gold and silver are literally buying and selling for in India — proper right here, proper now.

So as a substitute of going to London each morning for a value in US {dollars} after which doing 5 to six guide changes that differ from one AMC to a different, each fund home will now merely choose up the identical Indian market value, from the identical regulated Indian change, each single day.

Going again to the weighing balance instance — SEBI has now mentioned: each store should use the identical commonplace government-certified weighing scale. No extra every shopkeeper calibrating their very own machine in another way. One scale. One commonplace. Each fund home. Daily.

However Will All Gold ETF NAVs Develop into Equivalent Now?

That is probably the most pure query at this level — and it completely deserves a transparent reply.

No. All Gold ETF NAVs is not going to grow to be equivalent. And they need to not.

Gold costs nonetheless go up and down each single day. All Gold ETF NAVs will proceed transferring with gold costs. Two funds from two totally different fund homes will nonetheless present considerably totally different NAVs. That’s utterly regular and anticipated.

However right here is the important shift — after April 1, 2026, any NAV distinction between two funds will likely be an actual and significant distinction, not a synthetic one.

If you happen to now see Fund A’s NAV larger than Fund B’s NAV over a time period, it should solely be due to real causes akin to:

Expense ratio — if Fund A fees 0.50% per yr and Fund B fees 0.25% per yr, over time Fund B’s NAV will compound sooner. This can be a actual distinction that tells you which ones fund prices you much less

Monitoring effectivity — how properly every fund truly manages shopping for, storing, and accounting for its bodily gold holdings

Money drag — funds hold a small portion of their corpus in money to deal with every day redemptions; this small distinction varies throughout fund homes

These are actual, significant variations. They inform you one thing genuinely helpful about which fund is run extra effectively and at a decrease value to you.

What the brand new rule completely removes is the synthetic noise — the half the place two funds holding equivalent gold confirmed totally different NAVs just because one AMC’s workforce utilized a unique notional premium from one other’s. That faux, deceptive distinction is now gone for good.

In actual fact, Niranjan Avasthi from Edelweiss Mutual Fund put it merely: “Gold and Silver ETF NAV returns for all ETFs will now be nearer to one another.” That’s exactly what this reform achieves.

| Earlier than April 1, 2026 | From April 1, 2026 | |

| Worth reference | LBMA, London (in US {Dollars}) | Indian inventory change (in Indian Rupees) |

| Who units the value | Worldwide physique in London | Regulated Indian exchanges like MCX, BSE |

| Changes wanted | 5 to six layers, every AMC decides its personal | Minimal and uniform for all fund homes |

| Why NAVs differed | Actual distinction + synthetic AMC adjustment | Solely actual variations like expense ratio |

| Are you able to evaluate two Gold ETFs? | Not reliably | Sure, reliably and meaningfully |

What Ought to You Do as an Investor Proper Now?

Nothing. Completely nothing pressing.

In case you are already holding Gold ETFs, Silver ETFs, or Gold and Silver Mutual Funds — whether or not by means of SIP or lumpsum — merely proceed. Your bodily gold and silver holdings contained in the fund are utterly untouched. Your items are secure. There isn’t a exit required, no switching wanted, no paperwork out of your finish.

On or round April 1, 2026, you would possibly discover your Gold ETF or Silver ETF NAV trying barely totally different from the way it was trending within the days earlier than. Please don’t panic. This isn’t a loss. It’s not a fund error. It’s merely the one-time impact of switching from the outdated London-based pricing technique to the brand new Indian exchange-based pricing technique. As soon as this transition settles, your NAV will proceed to behave precisely because it at all times has — rising when gold rises, falling when gold falls.

SEBI has additionally directed AMFI (Affiliation of Mutual Funds in India) to work out an in depth uniform coverage on how this spot value polling will function on a day-to-day foundation throughout all fund homes. Additional operational readability from AMFI is anticipated quickly.

Conclusion –

This can be a wise and long-overdue correction by SEBI — and actually, it’s stunning it took this lengthy.

For years, the LBMA-based technique quietly confused unusual traders with out anybody clearly explaining what was truly occurring behind the scenes. You’d take a look at two Gold ETFs in your app, see totally different NAVs, and surprise — which one is performing higher? Ought to I change? Am I within the fallacious fund?

Half the time, neither fund was truly higher. They have been merely utilizing totally different inside changes that created a very synthetic phantasm of efficiency distinction — the place none existed in actuality.

Shifting to a single, Indian, exchange-published spot value removes that phantasm completely. Now whenever you see one Gold ETF clearly outperforming one other over a time period, it should imply one thing actual — decrease prices, higher fund administration, tighter monitoring of the underlying steel. That’s data you’ll be able to genuinely act on as an investor.

For many retail traders, this variation is not going to really feel dramatic in day-to-day life. The gold in your ETF is similar. The fund is similar. Your SIP continues as earlier than. However on the coverage degree, this can be a important and necessary step towards making Gold and Silver ETFs extra clear, extra comparable, and extra reliable as funding merchandise for unusual Indians.

As at all times, gold stays what it’s — a long-term portfolio hedge and diversifier, not a short-term buying and selling instrument. Whether or not NAVs have been calculated utilizing London costs or MCX costs, your actual problem in gold investing has at all times been the identical: persistence, not pricing methodology.

Disclaimer: This text is written purely for academic functions and shouldn’t be thought of as funding recommendation. Mutual Fund investments are topic to market dangers. Please learn all scheme-related paperwork fastidiously earlier than investing.

Supply: SEBI Round No. HO/(68)2026-IMD-POD-2/I/5780/2026 dated February 26, 2026. Obtainable at sebi.gov.in below Authorized > Circulars.