{kind=link}

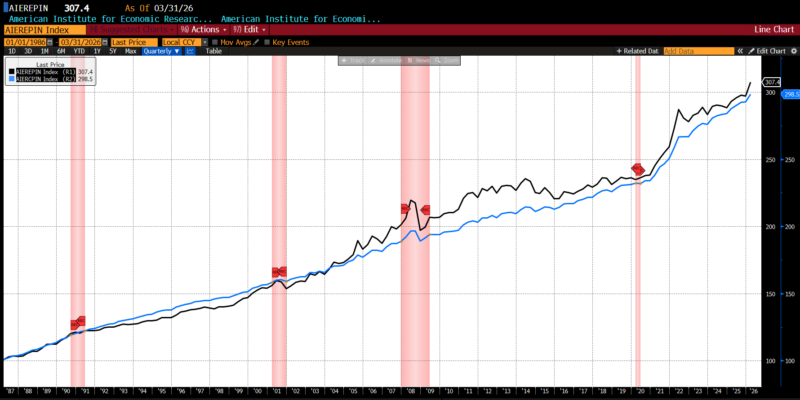

AIER’s proprietary On a regular basis Value Index (EPI) vaulted 2.5 p.c to 307.4 in March 2026, its second-largest month-to-month improve again to January 2020 (the primary was a rise of two.9 p.c in March 2022). Of the 24 value classes that compose the EPI, fourteen rose, two had been unchanged, and eight declined. Unsurprisingly, the most important jumps in value occurred in motor gasoline, housing fuels and utilities, and meals away from residence. Prescribed drugs, web companies, and meals at residence declined essentially the most. (The juxtaposition of value modifications within the meals away from residence versus meals at residence classes possible displays the gasoline pass-through of meals supply service prices.)

AIER On a regular basis Value Index vs. US Shopper Value Index (NSA, 1987 = 100)

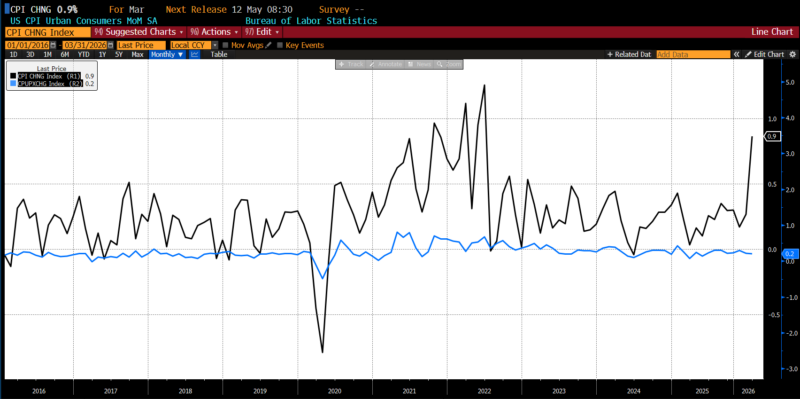

The US Bureau of Labor Statistics (BLS) launched Shopper Value Index (CPI) knowledge for March 2026 on April 10, 2026. Headline inflation rose 0.9 p.c over the previous month, assembly survey expectations. Core inflation rose 0.2 p.c, additionally assembly forecasts.

March 2026 US CPI headline and core month-over-month (2016 – current)

Shopper costs in March confirmed a combined sample, with meals costs flat total after February’s 0.4 p.c achieve, as grocery costs slipped 0.2 p.c even whereas restaurant costs continued to edge larger. Inside meals at residence, most main classes softened, led by a 0.6 p.c decline in meats, poultry, fish, and eggs — helped by a 3.4 p.c drop in egg costs — whereas cereals, dairy, and nonalcoholic drinks additionally moved decrease; the principle exception was fruit and veggies, which rose 1.0 p.c. The dominant story, nevertheless, was power, which surged 10.9 p.c on the month, its sharpest improve since 2005, pushed by a file 21.2 p.c soar in gasoline costs and a 30.7 p.c spike in gasoline oil, although pure gasoline costs bucked the pattern with a slight decline.

Core inflation, excluding meals and power, remained comparatively subdued at 0.2 p.c, matching February’s tempo and suggesting that the broader inflation impulse outdoors commodities remained largely contained. Housing-related prices continued their regular upward march, with shelter and house owners’ equal lease every rising 0.3 p.c, whereas lease itself elevated 0.2 p.c. A number of travel- and consumer-sensitive classes additionally superior, together with airline fares, up 2.7 p.c, attire, up 1.0 p.c, and training, up 0.3 p.c, indicating persistent service-sector firmness. Offsetting these positive factors had been declines in medical care, particularly prescribed drugs, together with decrease costs for used autos and private care items. Taken collectively, the March report factors to an inflation profile dominated by a commodity-driven power shock layered atop still-firm however comparatively average core and shelter pressures.

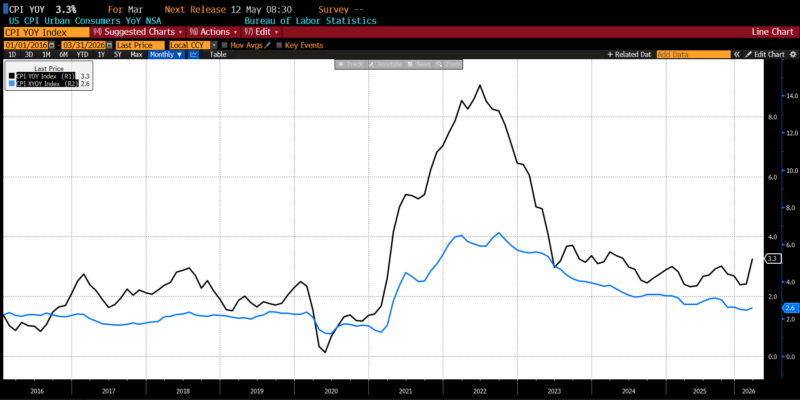

On the year-over-year facet, the March 2026 headline CPI jumped to three.3 p.c from 2.4 p.c the prior month, barely lower than the three.4 p.c predicted. Core costs, which strip out the extra unstable meals and power elements, superior 2.6 p.c over the identical interval versus the two.7 p.c survey expectation.

March 2026 US CPI headline and core year-over-year (2016 – current)

From March 2025 via March 2026, inflation remained broad however uneven throughout main client classes. Grocery costs rose 1.9 p.c total and restaurant costs climbed a stronger 3.8 p.c. Inside meals at residence, the most important annual positive factors got here from nonalcoholic drinks, up 4.7 p.c, fruit and veggies, up 4.0 p.c, and the “different meals at residence” class, which elevated 2.9 p.c, whereas cereals and bakery merchandise posted a extra modest 2.1 p.c rise. Offsetting these positive factors had been declines in dairy merchandise, down 1.6 p.c, and in meats, poultry, fish, and eggs, which slipped 0.9 p.c from a 12 months earlier. Power remained one of many strongest inflation drivers, advancing 12.5 p.c 12 months over 12 months, led by an 18.9 p.c soar in gasoline costs, alongside notable will increase in electrical energy and pure gasoline prices.

Excluding meals and power, core client costs rose 2.6 p.c over the 12 months, indicating that underlying inflation pressures remained current however far much less dramatic than within the commodity-sensitive classes. Shelter prices continued to supply a gradual supply of upward stress, growing 3.0 p.c over the previous 12 months and reinforcing the persistence of services-related inflation. Different areas exhibiting significant annual positive factors included medical care, family furnishings, recreation, and particularly airline fares, which surged 14.9 p.c. Taken collectively, the annual knowledge counsel an inflation setting formed by still-elevated power prices, agency service-sector pricing, and selective meals value energy, at the same time as some grocery classes supplied customers modest reduction.

The March CPI report was, above all, the primary clear inflation print to indicate the financial results of the Iran struggle filtering instantly into family costs. Probably the most fast transmission channel was power, the place the soar in oil costs quickly fed into gasoline and associated gasoline prices, pushing the headline studying markedly larger and dominating the general public notion of the report. This was much less a narrative of generalized demand stress than of a geopolitical commodity shock out of the blue colliding with the buyer economic system. In that sense, March’s inflation image regarded extra like an exterior provide disturbance than the sort of broad-based overheating that sometimes worries central banks most.

Beneath that headline surge, nevertheless, the underlying inflation construction remained comparatively calm. Grocery costs had been combined to softer, a number of main items classes confirmed little proof of renewed pricing stress, and a few discretionary client areas even appeared to weaken as households started adjusting to larger prices on the pump. Companies inflation, whereas nonetheless agency in key shelter-related elements, usually moderated, suggesting that the oil shock had not but meaningfully unfold into the broader service economic system. The one apparent early spillover was in travel-sensitive classes equivalent to airfares, the place larger jet-fuel prices possible started feeding via virtually instantly.

Taken collectively, the report reads because the opening stage of an energy-led inflation episode reasonably than a real reacceleration of the broader value pattern. The phenomenology is vital: customers are first encountering the shock in essentially the most seen and psychologically highly effective locations — gasoline stations, journey, and transportation-linked bills — whereas the remainder of the basket stays relativelys steady. That distinction issues the place coverage is worried, because it offers the Federal Reserve room to interpret the transfer as a brief oil-driven disruption reasonably than proof that inflation is turning into entrenched once more. The following few experiences will decide whether or not this stays a contained geopolitical value shock or evolves into one thing extra diffuse throughout an already-strained family price panorama.