{kind=link}

A succession of shocks to the worldwide financial system lately has targeted consideration on the improved financial and monetary resilience of rising market economies. For a few of these economies, this evaluation is well-founded and highlights the fruits of deep, structural financial reforms because the Nineteen Nineties. Nonetheless, for a a lot bigger universe of nations, the flexibility to climate shocks continues to be blended and lots of stay weak. On this submit, we discover the divide between the 2 units of nations and concentrate on the results of current financial shocks, together with the continuing battle within the Center East.

Defining Rising Markets

There is no such thing as a official definition of what constitutes an rising market (EM) financial system, however the time period is usually related to a rustic’s stage of per capita earnings, exports of products and companies, and integration into the worldwide monetary system. Additionally it is a monetary market conference used for asset allocation, danger evaluation, and index inclusion. A typical market reference, the MSCI Rising Market Index, contains twenty-four principally middle-income economies with liquid bond and fairness markets, however excludes the a lot bigger swath of growing international locations that symbolize a major share of the world’s inhabitants, together with a disproportionate share of the world’s poorest international locations.

For comparability, we phase rising markets into two groupings. We contemplate “Core” rising markets to be these international locations included within the MSCI Index (excluding superior economies South Korea and Taiwan). Extra broadly, our “Periphery” rising markets comprise ninety-two international locations that fall exterior the MSCI Index. The latter group excludes each international locations which can be in sustained large-scale armed battle and small island states that lack entry to worldwide sovereign bond markets.

As highlighted within the desk under, Core EMs have greater than doubled their share of the world financial system over the previous twenty-five years, with a lot of that development attributable to China’s outstanding (albeit uneven) growth. Over the identical interval, Periphery EMs’ share of worldwide GDP has remained stagnant, whereas their share of world inhabitants has grown, widening the wealth hole in per capita phrases. Excluding China and India, the Periphery international locations have a considerably bigger share of the world’s inhabitants than the Core international locations.

Stark Variations Between Core and Periphery Rising Markets

| Core EMs | Periphery EMs | |||||

| 22 international locations | Ex. China & India | 92 international locations | ||||

| Share of worldwide: | 2000 | 2025 | 2000 | 2025 | 2000 | 2025 |

| GDP | 14% | 33% | 9% | 13% | 6% | 6% |

| Gov’t debt | 7% | 26% | 5% | 7% | 2% | 7% |

| Inhabitants | 55% | 52% | 17% | 17% | 22% | 27% |

Notes: Core EMs embrace Brazil, Chile, China, Colombia, Hungary, India, Indonesia, Kuwait, Malaysia, Mexico, Morocco, Peru, Philippines, Poland, Qatar, Romania, Saudi Arabia, South Africa, Thailand, Turkey, U.A.E., and Vietnam. Periphery EMs exclude international locations that meet the UCDP definition of being at “conflict” and UN-defined small island growing states which can be not within the JP Morgan EMBI Index.

How Core EMs Constructed Resilience

The improved resilience of Core EM economies displays the sustained interval of macroeconomic and institutional reform that started after the crises of the Nineteen Nineties. At the moment, many governments confronted excessive publicity to international forex liabilities, restricted international change reserves, and weak financial coverage frameworks, leaving them weak to capital stream reversals. Over subsequent many years, Core EMs carried out reforms geared toward lowering these vulnerabilities and strengthening coverage credibility.

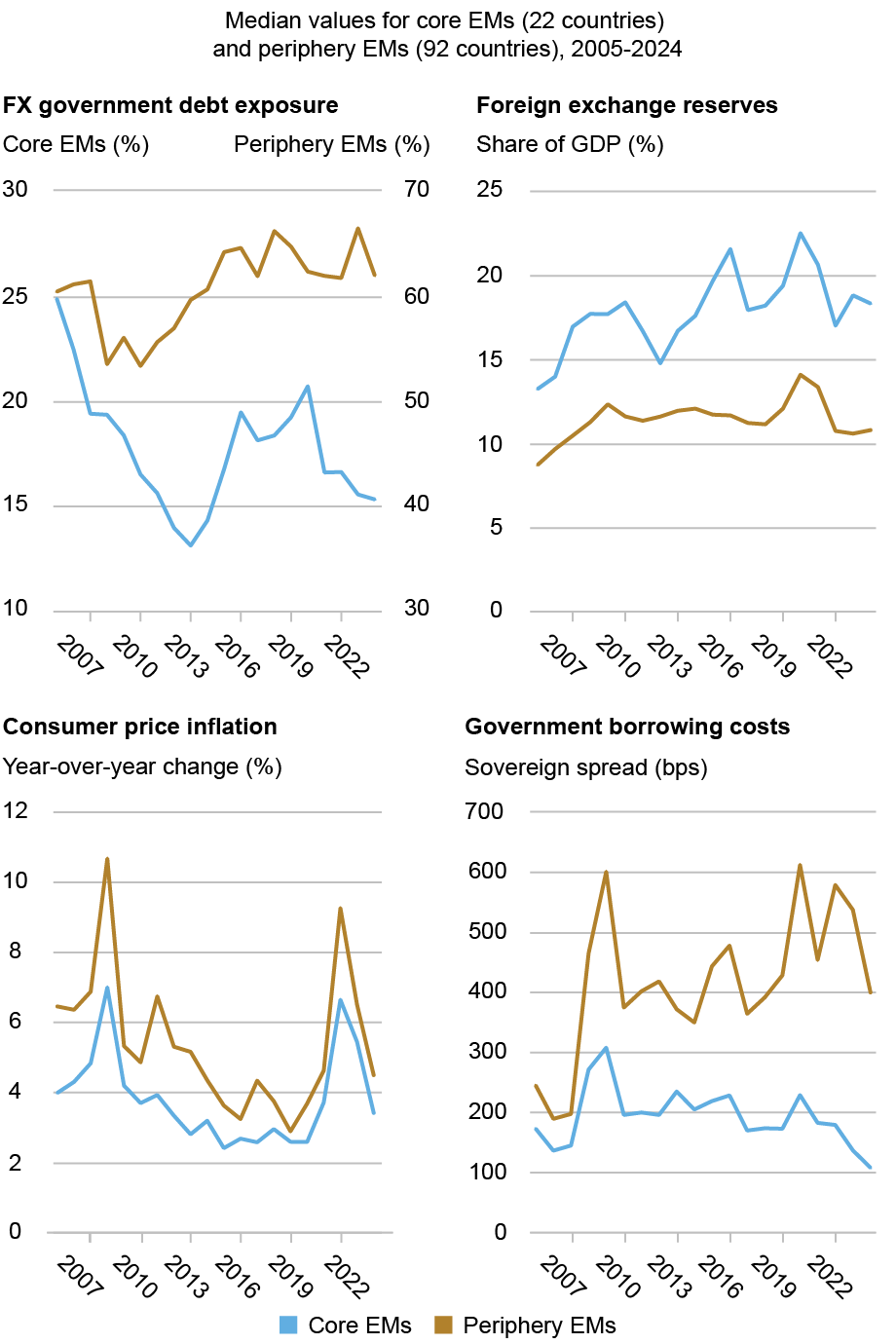

A central reform has been the discount in reliance on international forex borrowing. Traditionally, EMs had little choice however to concern debt primarily in U.S. {dollars} (i.e., “authentic sin”), exposing their public funds to change price actions. Core EMs regularly expanded their home capital markets and broadened their native investor base, enabling governments to concern a bigger share of debt in home forex. As proven within the higher left panel of the chart under, whereas international forex debt publicity fluctuated, it declined on internet for Core EMs over the previous twenty years and remained at comparatively low ranges in comparison with Periphery economies, the place publicity remained considerably elevated.

Core EMs additionally strengthened exterior buffers by way of sustained international change reserve accumulation. Their median reserve buffers have risen considerably in current many years, offering higher capability to soak up exterior shocks and permitting change charges to regulate. The higher proper panel of the chart under illustrates this widening hole: Core EMs entered current international shocks with considerably larger reserve protection than Periphery economies.

Institutional reforms bolstered macroeconomic enhancements. Core EMs enhanced central financial institution independence and clarified coverage mandates, contributing to higher anchored inflation expectations. As proven within the backside left panel of the chart under, Core EMs skilled a smaller inflation spike and a quicker return towards pre-pandemic ranges. This efficiency contrasts with Periphery economies, the place inflation remained elevated for longer.

Lastly, monetary markets mirrored these variations by way of sovereign borrowing prices. The underside proper panel of the chart under exhibits a decrease price of sovereign borrowing for Core EMs even within the aftermath of current international shocks (e.g., the pandemic and international financial tightening), whereas Periphery EM sovereign credit score spreads (above U.S. Treasury securities) remained elevated.

Core EMs’ Bigger Buffers Result in Higher Outcomes In comparison with Periphery EMs

Notes: Sovereign spreads are measured by U.S. dollar-denominated debt over U.S. Treasuries. Periphery borrowing prices and international forex share of presidency debt could also be understated as a consequence of restricted worldwide market entry and knowledge availability.

The Coverage Dilemma Going through Periphery Economies

Many Periphery economies nonetheless borrow predominantly in foreign exchange, maintain decrease ranges of international change reserve buffers, and have central banks that buyers view as much less credible. When international danger urge for food shifts, capital outflows from rising markets sometimes result in forex depreciations. In economies with important reliance on international forex borrowing, this depreciation tightens monetary situations by straining authorities and private-sector stability sheets and elevating debt servicing prices. For a lot of Periphery EMs, policymakers are nonetheless unable to react to a shock with countercyclical coverage (i.e., financial coverage easing or fiscal enlargement) as a consequence of considerations over inflation and monetary stability. Usually authorities in these international locations tighten insurance policies or promote international change reserves to defend the forex, usually worsening output losses (i.e., “worry of floating”).

Evaluating Rising Market Resilience Throughout and After the Pandemic

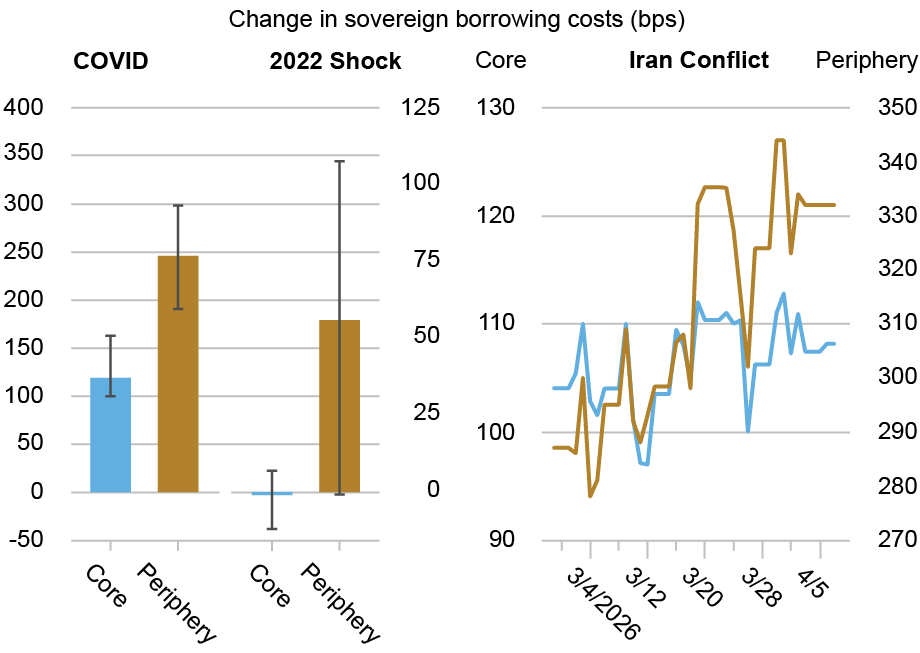

Current international shocks spotlight the divergence in resilience between Core and Periphery EMs. We concentrate on the respective sovereign borrowing prices throughout risk-off intervals round COVID and the following international financial tightening and provide shocks of 2022. The higher left panel of the chart under illustrates considerably bigger will increase in borrowing prices (as measured by adjustments in median sovereign bond spreads over U.S. Treasury securities) amongst Periphery EMs throughout each shocks.

Within the higher proper panel, we additionally contemplate adjustments in sovereign borrowing prices because the onset of the latest battle within the Center East. The median sovereign unfold throughout Periphery EMs has elevated by 45 bps from February 27 to 332 bps, whereas the median unfold on Core EM debt has elevated by solely 4 bps over the identical interval.

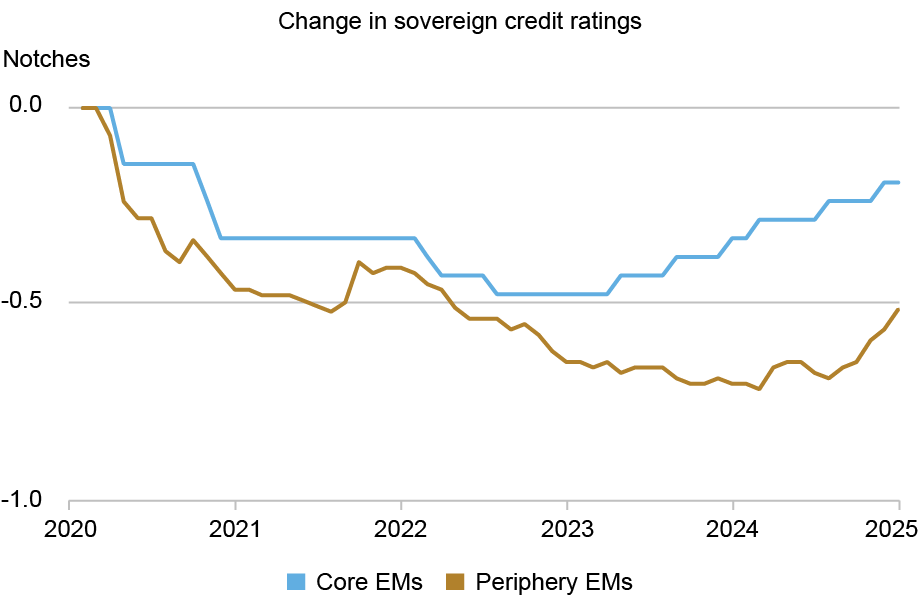

Sovereign credit score rankings inform the same story. These rankings measure the default likelihood of presidency debtors by contemplating a rustic’s financial, coverage, and institutional strengths, making them a pure barometer of structural resilience. Within the chart under, the decrease panel exhibits Periphery EMs with bigger and extra widespread credit standing downgrades relative to their Core counterparts and slower, much less pronounced upgrades since 2023. Sovereign borrowing prices and credit score rankings matter as a result of they instantly have an effect on market entry and refinancing dangers. Larger spreads and downgrades increase the price of rolling over present debt and might restrict entry to exterior financing when funding wants are best.

Periphery EMs Confronted Bigger Borrowing Price Spikes and Steeper Credit score Score Downgrades in Current Shocks

Notes: The higher left panel exhibits the median unfold change (in foundation factors) from the day earlier than every of two shocks. The COVID shock has a baseline date of January 22, 2020 (the day earlier than the Wuhan shutdown) and spans January 23-April 30, 2020. The 2022 shock has a baseline date of February 23, 2022 (the day earlier than Russia’s invasion of Ukraine) and spans February 24-Might 31, 2022. Bars present the median change in sovereign spreads (episode median minus baseline day); error bars present the interquartile vary (Twenty fifth-Seventy fifth percentile). The higher proper panel exhibits median sovereign spreads since February 27, 2026 (the day earlier than the outbreak of the Iran battle). Nations within the midst of debt restructuring on the time of every episode are excluded from the related panels. The decrease panel exhibits the change in imply sovereign credit score rankings from a January 2020 baseline; shifts larger mirror upgrades.

The Function—and Limits—of the International Monetary Security Internet

The worldwide monetary security internet has performed an essential position in shaping rising market outcomes, with Core rising markets engaged with IMF amenities on a precautionary foundation, thus reinforcing market confidence and preserving coverage flexibility. Against this, Periphery economies have extra usually relied on IMF assist beneath situations of acute stress, sometimes alongside rising borrowing prices and lack of market entry.

These variations mirror constraints imposed by the international monetary cycle and the restricted potential of exterior financing to offset shifts in international danger urge for food. Almost half of Periphery economies accessed IMF misery financing between 2020 and 2023, usually amid sharp will increase in sovereign spreads and widespread credit standing downgrades. Repeated program use has been widespread; of the Periphery international locations which have entered IMF packages since 2000, 70 % have needed to search three or extra such preparations.

Whereas IMF assist has helped stabilize situations in periods of stress, it has not persistently restored sturdy market entry. This sample is according to earlier proof on IMF-supported packages and market entry exhibiting that official financing can include crises with out totally resolving underlying vulnerabilities. Since 2005, Periphery economies have recorded thirty-two sovereign defaults throughout seventeen international locations (Argentina, Belize, and El Salvador have defaulted not less than thrice every), whereas no Core rising market has defaulted over the identical interval.

Wanting Ahead

Current shocks have bolstered the divide between rising markets which have strengthened their coverage frameworks and people who stay extra uncovered to exterior volatility. Core EMs have been higher positioned to soak up shocks and keep market entry, whereas many Periphery economies proceed to face tough tradeoffs when international situations tighten. Bridging this hole would require sustained progress in home coverage credibility, macroeconomic stability, and shock absorption capability. Exterior assist can ease adjustment in periods of stress, however sturdy resilience finally will depend on reforms carried out at residence.

Hunter L. Clark is an financial coverage advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Jeffrey B. Dawson is an financial coverage advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Julian Gonzalez-Murphy is a rustic danger affiliate within the Federal Reserve Financial institution of New York’s Markets Group.

The way to cite this submit:

Hunter L. Clark, Jeffrey B. Dawson, and Julian Gonzalez-Murphy, “A Nearer Take a look at Rising Market Resilience Throughout Current Shocks,” Federal Reserve Financial institution of New York Liberty Avenue Economics, April 9, 2026, https://doi.org/10.59576/lse.20260409

BibTeX: View |

Disclaimer

The views expressed on this submit are these of the creator(s) and don’t essentially mirror the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the accountability of the creator(s).