{kind=link}

Joint financial institution accounts are sometimes opened by spouses, dad and mom and kids, or enterprise companions. However many individuals assume that the primary account holder robotically will get the tax profit, or that the TDS deducted by the financial institution decides who ought to report the revenue.

In actuality, taxation is determined by who really owns the cash, not simply on whose identify seems first within the account.

So earlier than we have a look at the principles, let’s clear one widespread fable: simply because it’s a joint account doesn’t imply cash, taxes, or advantages are cut up equally. The Earnings Tax Division appears on the supply of funds and the precise contributor of the capital. That’s what determines possession, and in flip, the tax legal responsibility.

Allow us to perceive 5 essential tax and home-loan-related guidelines relevant to joint financial institution accounts.

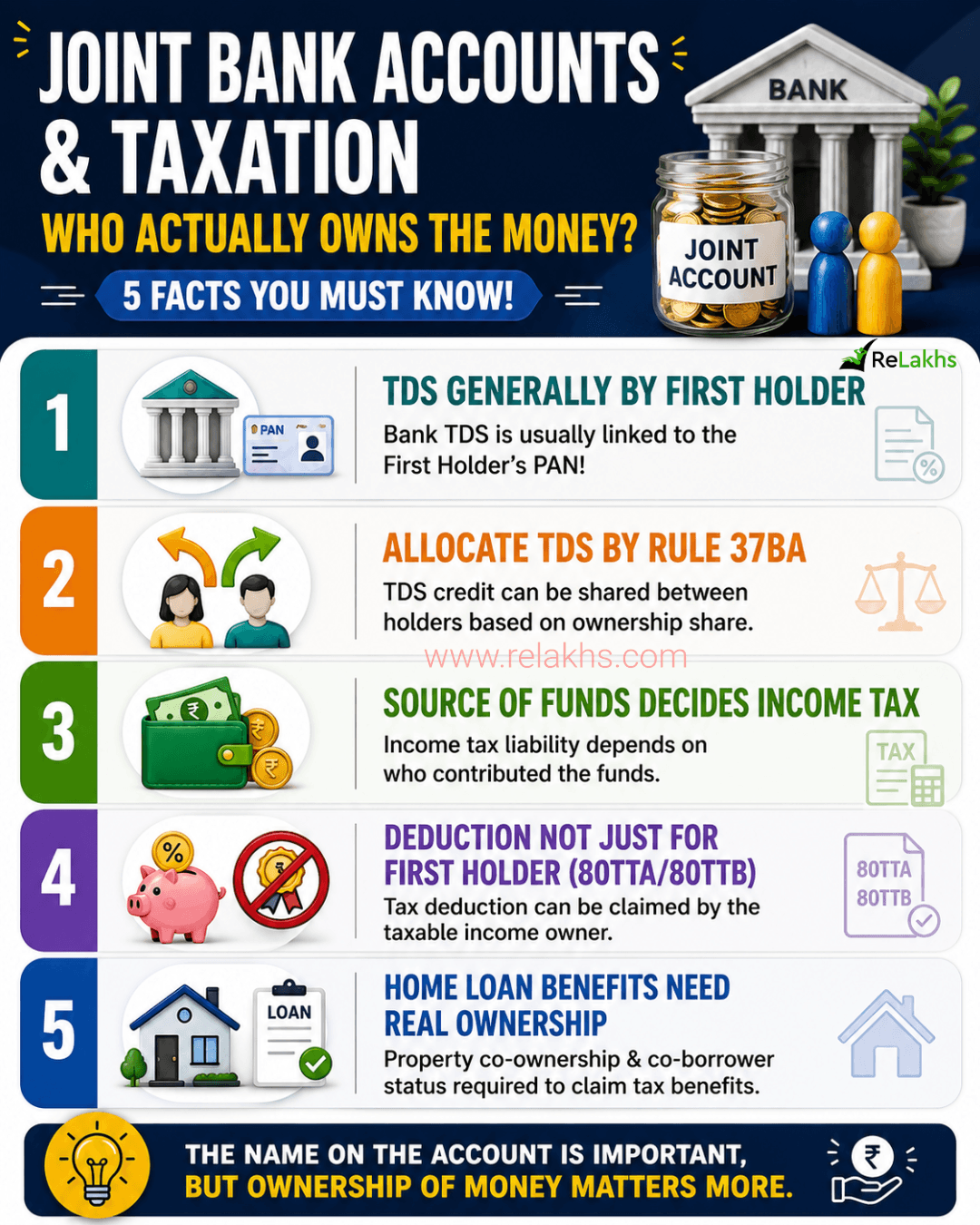

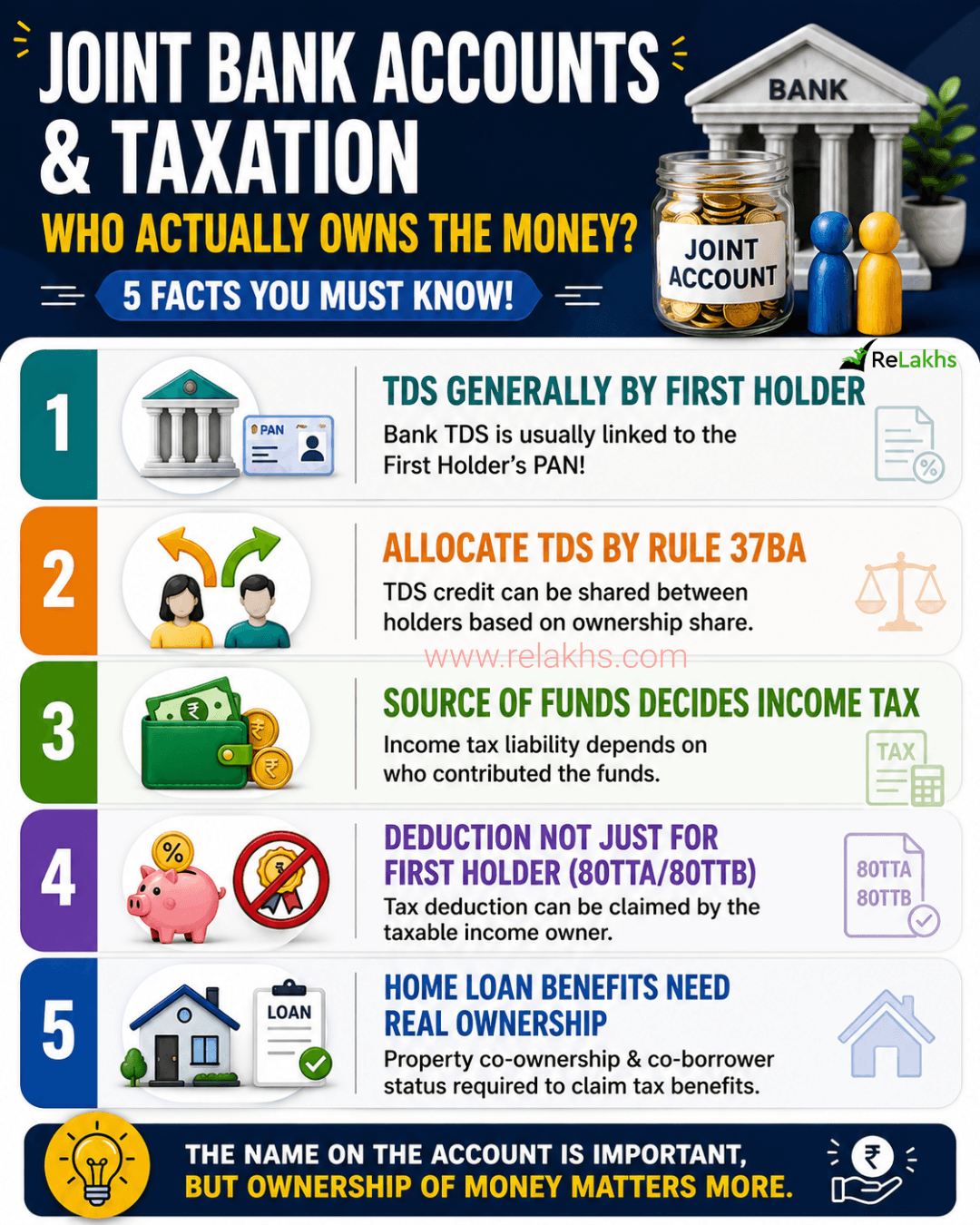

Rule #1 – TDS is usually deducted within the identify of the First Account Holder

If a financial institution deducts TDS on the curiosity earned from a joint fastened deposit or different interest-bearing deposit, the TDS is usually deducted towards the PAN of the primary (main) account holder.

For instance, allow us to assume a husband and spouse have a joint FD that earns curiosity of ₹60,000 throughout a monetary 12 months. If the husband is the primary holder, the financial institution will typically report the curiosity revenue and TDS towards his PAN.

Consequently:

- The TDS credit score will normally seem within the husband’s Kind 26AS and AIS.

- The spouse might not see this TDS credit score in her tax information.

Many taxpayers wrongly assume that as a result of the TDS seems within the first holder’s PAN, your complete curiosity revenue should even be taxed in that particular person’s fingers. This isn’t essentially right. TDS reporting and taxation of revenue are two various things.

Did You Know?

Most joint FD holders assume TDS should all the time be deducted within the first holder’s PAN. Nevertheless, beneath Rule 37BA, joint holders can request the financial institution to allocate TDS credit score in accordance with their precise possession/share within the deposit, topic to the financial institution’s procedures and documentation necessities

Rule #2 – TDS Credit score Can Be Allotted Based mostly on Precise Possession (Rule 37BA)

The Earnings-tax Guidelines present an answer when the revenue from a joint deposit belongs to a couple of particular person.

Underneath Rule 37BA, TDS credit score might be claimed by the one that is definitely taxable on the revenue, topic to prescribed situations.

For instance:

- Husband contributes ₹6 lakh (60%)

- Spouse contributes ₹4 lakh (40%)

- Curiosity earned through the 12 months is ₹10,000 on a Rs 10 Lakh joint deposit

On this case, the curiosity revenue belongs to each account holders within the ratio of 60:40. Accordingly, the husband’s share of curiosity is ₹6,000 and the spouse’s share is ₹4,000.

To make sure that the corresponding TDS can also be allotted in the identical ratio, the joint account holders might submit a declaration to the financial institution earlier than TDS is deducted, requesting the financial institution to separate the curiosity revenue and TDS credit score primarily based on their precise contribution ratio.

| State of affairs (60:40 Contribution) | First Holder (Husband) | Second Holder (Spouse) |

| Capital Contributed | ₹6,00,000 (60%) | ₹4,00,000 (40%) |

| Curiosity Earnings Earned | ₹6,000 | ₹4,000 |

| Default Financial institution Reporting (No Rule 37BA) | 100% Curiosity & TDS displays in AIS/26AS | 0% displays in AIS/26AS |

| After Rule 37BA Declaration | 60% TDS credited | 40% TDS credited |

It’s advisable to submit this declaration on the time of opening the deposit or nicely earlier than the top of the monetary 12 months and preserve information of the supply of funds and contribution ratio. Do notice that the operational course of and documentation necessities might differ from one financial institution to a different.

Rule #3 – Curiosity Earnings Depends upon the Supply of Funds

This is likely one of the most misunderstood elements of joint financial institution accounts. Simply because somebody’s identify is added to the account doesn’t imply the curiosity revenue robotically turns into taxable in that particular person’s fingers.

The true query is easy: who really contributed the cash? Generally, curiosity revenue follows the possession of the funds, not the order of names on the account.

For instance, if the husband put within the full deposit quantity, the curiosity could also be taxable in his fingers even when the account is joint along with his spouse. If the spouse contributed the complete quantity, then the curiosity could also be taxable in her fingers as an alternative. And if each contributed equally, the curiosity can typically be divided equally for tax functions.

So whenever you file your revenue tax return, the main focus ought to be on the supply of funds and helpful possession, not simply whose identify comes first within the checking account.

Rule #4 – Who Can Declare Deduction Underneath Part 80TTA or 80TTB?

A standard fable is that solely the primary account holder can declare the tax deduction on curiosity revenue, however that isn’t all the time true. The deduction ought to typically go to the one that is definitely taxed on that curiosity revenue.

Part 80TTA is on the market to eligible people and HUFs on financial savings account curiosity, throughout the prescribed restrict. Part 80TTB is on the market to eligible senior residents on specified curiosity revenue, additionally topic to the prescribed restrict.

For instance, if a joint financial savings account earns ₹15,000 in curiosity and the spouse is the actual proprietor of the funds, then the curiosity could also be taxable in her fingers. In that case, she could possibly declare the deduction even when she just isn’t the primary account holder.

So the straightforward rule is that this: the deduction follows the taxable revenue, not simply the order of names within the account.

Key Takeaway: Tax deductions comply with the taxable revenue, not the banking sequence. If you’re reporting the curiosity revenue in your ITR, you’re the one eligible to assert the Part 80TTA/80TTB deduction.

Notice: Deductions beneath Part 80TTA and 80TTB can be found provided that you select the Outdated Tax Regime. When you go for the New Tax Regime, these deductions can’t be claimed.

Rule #5 – A Joint Financial institution Account Does Not Robotically Create Residence Mortgage Tax Advantages

Many {couples} pay their dwelling mortgage EMIs from a joint checking account, and it’s straightforward to imagine that each account holders can robotically declare the tax profit. However that isn’t the way it works.

The tax division appears at three issues: who owns the property, who’s the borrower, and who really repays the mortgage. In different phrases, the joint account is simply the fee route — it doesn’t resolve the tax profit by itself.

For instance, if husband and spouse are each co-owners and co-borrowers, they are able to declare advantages primarily based on their respective contributions, topic to the regulation. But when the EMI is paid from a joint account and just one particular person owns the property, the opposite account holder doesn’t robotically get the deduction. Equally, if just one particular person is the borrower and eligible proprietor, the opposite particular person can’t declare the profit simply because the cash is flowing by means of a joint account.

So the straightforward rule is: a joint checking account doesn’t resolve dwelling mortgage tax eligibility — possession and borrowing standing do.

To say Residence Mortgage Tax Advantages (Principal/Curiosity), make sure you tick all 3 containers:

- [ ] Co-Proprietor: Your identify should be on the Property Title Deed.

- [ ] Co-Borrower: Your identify should be on the Financial institution Mortgage Sanction Letter.

- [ ] Contributor: You should be funding the Joint Account for EMIs in proportion to your possession share.

Conclusion

Many taxpayers assume that the primary account holder robotically will get the TDS credit score, tax advantages, and even dwelling mortgage deductions related to a joint checking account. Nevertheless, tax legal guidelines look past the order of names within the account.

Generally, what issues is the precise possession of funds, the supply of funding, property possession, borrower standing, and the person’s contribution in direction of compensation.

A joint checking account might make banking operations handy, nevertheless it doesn’t robotically decide who’s taxable on the revenue or who’s eligible to assert tax advantages.

Subsequently, earlier than opening a joint deposit, claiming curiosity deductions, or servicing a house mortgage by means of a joint account, it’s price taking a couple of minutes to know the tax implications. A small oversight at this time can result in pointless tax notices, disputes over TDS credit, or lack of professional tax advantages tomorrow.

Bear in mind, in taxation, the identify on the account is essential, however the possession of cash is commonly much more essential.

Proceed studying:

(Put up first revealed on : 24-June-2026)