{kind=link}

On this publish, we look at the evolution of U.S. Treasury market liquidity over the previous yr, which has witnessed myriad financial and political developments. Liquidity worsened markedly one yr in the past as volatility elevated following the announcement of higher-than-expected tariffs. Liquidity shortly improved when the tariff will increase have been partially rolled again after which remained pretty steady thereafter (by means of the top of our pattern in February 2026), together with after the latest Supreme Courtroom choice placing down the emergency tariffs and the following announcement of recent tariffs.

Why Treasury Market Liquidity Issues

The U.S. Treasury market is the biggest securities market on this planet, with greater than $30 trillion in marketable debt excellent as of February 28. The market is utilized by the Treasury Division to finance the U.S. authorities, by the Federal Reserve to implement financial coverage, and by monetary establishments to handle rate of interest threat and worth different securities. Liquidity is crucial to all of those makes use of and is due to this fact adopted intently by market contributors and policymakers.

How We Measure Treasury Market Liquidity

We outline market liquidity as the price of shortly changing an asset into money (or vice versa). As in our previous Workers Report, we have a look at three liquidity measures, estimated utilizing high-frequency knowledge from the interdealer market: the bid-ask unfold, order guide depth, and worth influence. The measures are calculated for essentially the most just lately auctioned (on-the-run) two-, five-, and ten-year notes over New York buying and selling hours (outlined as 7:30 a.m. to five p.m., Japanese time).

Volatility and Information over the Previous 12 months

As a result of volatility is tightly linked to Treasury market liquidity (see this LSE publish, for instance), we first assess worth volatility round necessary information occasions since April 2025. Volatility displays the uncertainty that always emanates from financial and political developments. We measure so-called realized volatility (volatility based mostly on precise worth variation) at a every day stage for a similar securities—and utilizing the identical knowledge—employed for our liquidity measures.

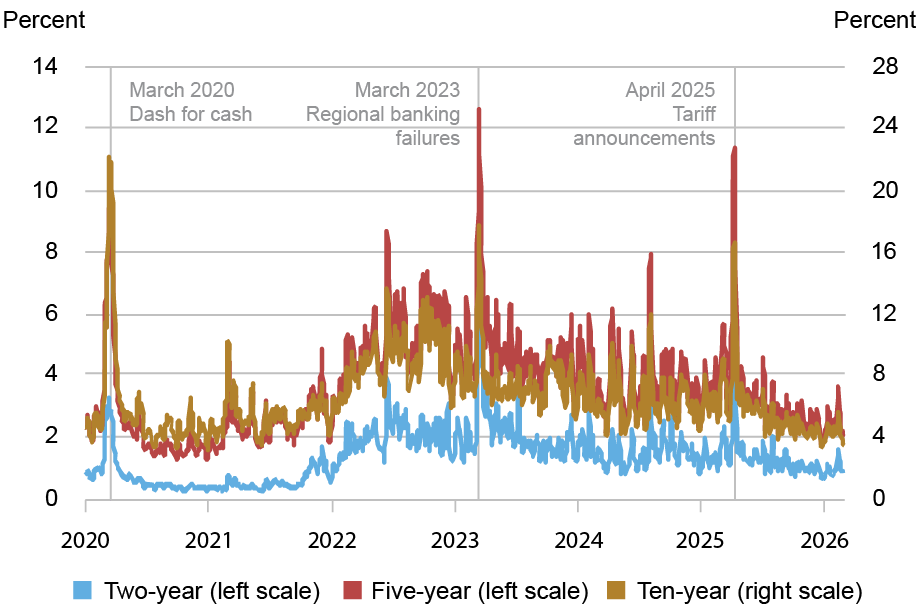

The chart beneath reveals that volatility rose sharply after the April 2, 2025 tariff announcement, peaking between April 7 and April 9. Treasury yields initially declined following the April 2 announcement (maybe as a result of flight-to-safety conduct by buyers), with the ten‑yr yield declining from about 4.2 p.c to as little as 3.9 p.c on April 4 earlier than closing the day at about 4.0 p.c (see the slide deck accompanying this Could speech by Roberto Perli, supervisor of the System Open Market Account).

Volatility Trended Down after April 2025 Spike

Notes: The chart plots five-day transferring averages of worth volatility for the on-the-run two-, five-, and ten-year notes within the interdealer market from January 2, 2020 to February 27, 2026. Worth volatility is calculated for every day by summing squared one-minute returns (log modifications in midpoint costs) from 7:30 a.m. to five p.m., annualizing by multiplying by 252, after which taking the sq. root. It’s reported in p.c. Drop strains flag the peaks within the five-day transferring common for the ten-year observe, that are centered round March 11, 2020, March 14, 2023, and April 8, 2025.

In the beginning of the subsequent buying and selling week, the ten-year yield opened decrease than Friday’s shut however rose quickly, from about 3.9 p.c to 4.5 p.c, or roughly 60 foundation factors, between 8 p.m. on April 6 and midnight two days later. Some analyses recommend the unwinding of swap unfold trades contributed to the rise in yields whereas others level to foreigners’ decreased willingness to carry Treasuries. On April 9, President Trump introduced that a lot of the new country-specific tariffs have been being postponed for 90 days. The ten-year yield declined sharply that day, later ending the week about 20 foundation factors larger than its stage on the time of the April 2 announcement.

After April 9, volatility shortly declined to extra regular ranges and continued trending down in subsequent months as extra tariff-related information was introduced: the implementation of the reciprocal tariffs, the Supreme Courtroom choice placing down the tariffs, and the instant imposition of new non permanent tariffs. There was a blip up in volatility in February 2026 across the releases of the employment report (February 11) and client worth index (February 13) however not across the Supreme Courtroom choice (February 20). Observe that our evaluation ends with the final buying and selling day of February 2026 and therefore doesn’t replicate results from the battle with Iran, which began the subsequent day.

Market Liquidity over the Previous 12 months

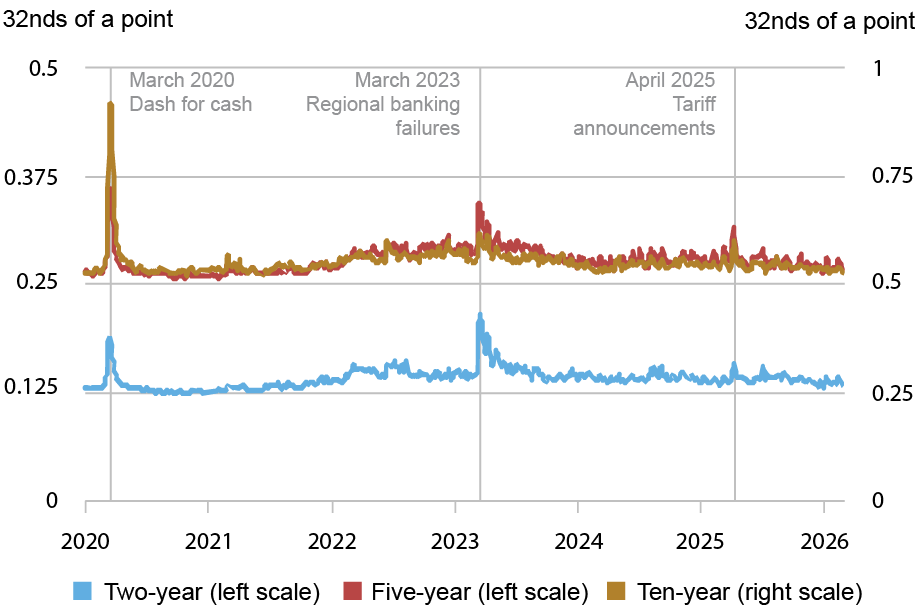

The bid-ask unfold is the distinction between the bottom ask worth and highest bid worth for a safety, with a wider unfold suggesting worse liquidity. Bid-ask spreads, proven within the chart beneath, widened markedly after the April 2 tariff announcement, albeit a lot lower than in March 2020 and even considerably lower than in the course of the March 2023 regional banking turmoil. Bid-ask spreads narrowed after the April 9 announcement that the brand new tariffs have been principally being postponed and since then have been just like ranges sometimes noticed in recent times.

Bid-Ask Spreads Had been Comparatively Steady after April 2025 Widening

Notes: The chart plots five-day transferring averages of common every day bid-ask spreads for the on-the-run two-, five-, and ten-year notes within the interdealer market from January 2, 2020 to February 27, 2026. Spreads are measured in 32nds of some extent, the place some extent equals one p.c of par. Drop strains flag the peaks within the five-day transferring common for the ten-year observe, that are centered round March 16, 2020, March 15, 2023, and April 9, 2025.

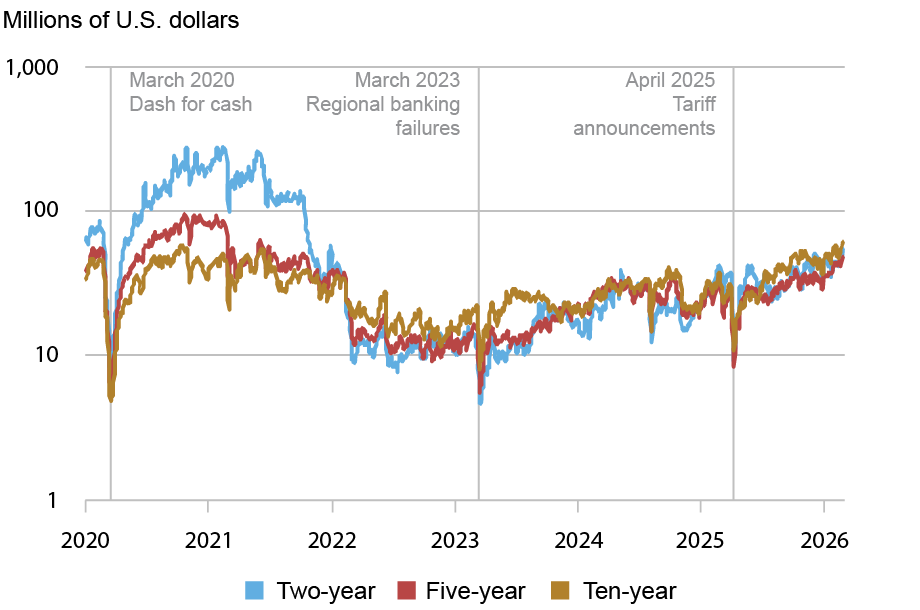

Order guide depth is measured as the common amount of securities posted for buy or sale at one of the best bid and supply costs. Decrease depth implies worse liquidity. This metric additionally factors to comparatively poor liquidity in April 2025, when obtainable depth declined to the bottom ranges since March 2023 (see chart beneath). Depth shortly recovered and by late summer time 2025 was at ranges just like, if not higher than, any time because the Fed’s post-COVID tightening cycle began in March 2022. Depth continued trending larger by means of February 2026.

Order E book Depth Elevated Steadily after April 2025 Decline

Notes: The chart plots five-day transferring averages of common every day depth for the on-the-run two-, five-, and ten-year notes within the interdealer market from January 2, 2020 to February 27, 2026. Knowledge are for order guide depth on the inside tier, averaged throughout the bid and supply sides. Depth is measured in tens of millions of U.S. {dollars} par and plotted on a logarithmic scale. Drop strains flag the low factors within the five-day transferring common for the ten-year observe, that are centered round March 16, 2020, March 15, 2023, and April 9, 2025.

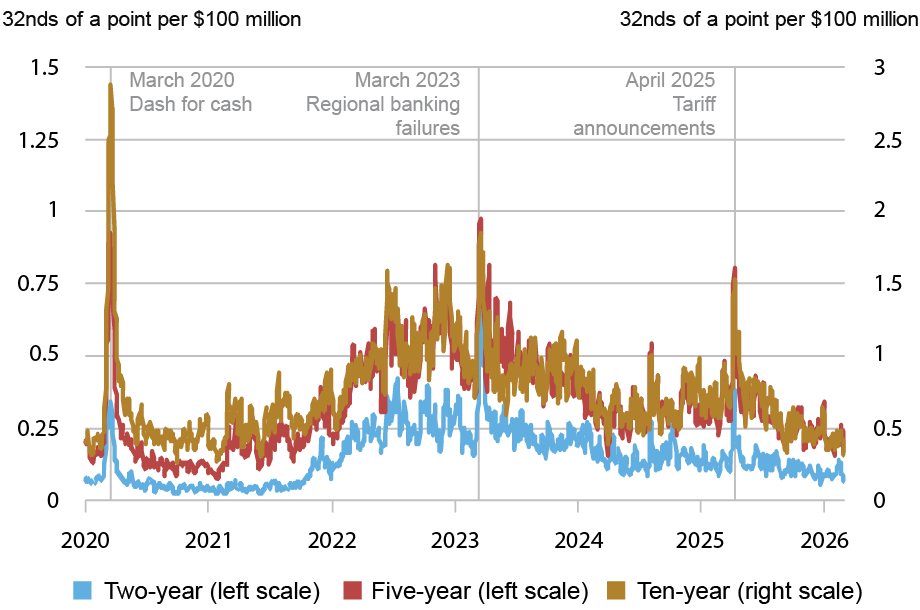

Measures of the worth influence of trades additionally recommend a pointy deterioration of liquidity in April 2025, a fast rebound, and regular enchancment thereafter. The following chart plots the estimated worth influence per $100 million in web order circulation (outlined as buyer-initiated buying and selling quantity much less seller-initiated buying and selling quantity). The next worth influence suggests diminished liquidity. Worth influence rose abruptly on April 2, however then shortly reverted. By early 2026, worth influence had turn out to be as little as at any time since 2021.

Worth Affect Trended Down after April 2025 Improve

Notes: The chart plots five-day transferring averages of slope coefficients from every day regressions of one-minute worth modifications on one-minute web order circulation (buyer-initiated buying and selling quantity much less seller-initiated buying and selling quantity) for the on-the-run two-, five-, and ten-year notes within the interdealer market from January 2, 2020 to February 27, 2026. Worth influence is measured in 32nds of some extent per $100 million, the place some extent equals one p.c of par. Drop strains flag the peaks within the five-day transferring common for the ten-year observe, that are centered round March 17, 2020, March 16, 2023, and April 9, 2025.

Summing Up

Treasury market liquidity over the previous yr was marked by a sudden however transient worsening after the April 2, 2025 tariff announcement, adopted by fast enchancment when the proposed tariffs have been partially rolled again. Liquidity steadily improved thereafter, reaching its greatest stage since 2021 in early 2026. Financial uncertainty and rate of interest volatility have elevated because the finish of our pattern interval—given the battle with Iran and its repercussions—underlining the view that Treasury market liquidity warrants continued shut watching.

Henry Dyer is a analysis analyst within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Michael J. Fleming is head of Capital Markets within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Tips on how to cite this publish:

Henry Dyer and Michael J. Fleming, “Treasury Market Liquidity Since April 2025,” Federal Reserve Financial institution of New York Liberty Avenue Economics, April 2, 2026, https://doi.org/10.59576/lse.20260402

BibTeX: View |

Disclaimer

The views expressed on this publish are these of the creator(s) and don’t essentially replicate the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the accountability of the creator(s).