{kind=link}

NTPC Ltd. – Main the Vitality Transition

NTPC Restricted (NTPC), included in 1975 and headquartered in New Delhi, is India’s largest energy producing firm and a Authorities of India Maharatna Central Public Sector Enterprise, producing energy throughout a diversified gas combine comprising coal, gasoline, hydro, photo voltaic, and wind. As of December 31, 2025, the NTPC Group had an put in and industrial capability of 85,637 MW, with coal accounting for 76% (65,194 MW) of the operational portfolio. Together with 32,958 MW underneath energetic building throughout thermal, renewable, hydro, and rising vitality segments, the group’s whole portfolio stood at 118,595 MW.

Merchandise and Providers

The corporate is primarily concerned in technology of electrical energy by way of a mixture of thermal (coal/gasoline), renewable (photo voltaic/wind), hydro, and rising nuclear property. Different providers supplied by the corporate includes home and cross-border vitality buying and selling (with Bangladesh, Bhutan, and Nepal), consulting providers, coal mining, growth of inexperienced hydrogen & chemical compounds, waste to vitality chemical compounds, e-mobility and so on.

Subsidiaries – As of FY25, the corporate has 11 subsidiaries and 18 joint ventures.

Funding Rationale

- Capability Commissioning because the Earnings Driver – NTPC’s income and profitability are tied extra to how a lot regulated capability will get commissioned than to how a lot energy is in the end dispatched, with CERC’s cost-plus framework guaranteeing a ~15.5% RoE on the fairness base of every working plant. As of Q3FY26, NTPC Group’s put in capability stood at 85,637 MW, up from 76,598 MW a 12 months in the past, with 32,958 MW at present underneath building throughout coal, hydro and renewables all of which can sequentially fee and circulation into the regulated fairness base. Standalone regulated fairness has grown to Rs.94,454 crore as of September 2025, up 6% YoY, whereas consolidated regulated fairness rose 10% to Rs.1,16,022 crore which is a direct, quantifiable proxy for earnings progress. Adjusted standalone PAT for 9M FY26 stood at Rs.13,585 crore, up Rs.570 crore YoY, even in a 12 months of subdued energy demand, reflecting the earnings resilience that the mounted cost restoration mechanism gives. That stated, execution threat on the under-construction pipeline notably for renewable capability the place grid connectivity and PPA tie-ups must progress in tandem with bodily building stays a key monitorable.

- Renewable vitality transition as the brand new progress engine – NGEL’s renewable capability has grown from 5,902 MW in the beginning of FY26 to eight,010 MW as of December 2025, with NTPC Group focusing on 60 GW of renewable capability by FY32. NTPC Group achieved highest annual addition of 9,039 MW within the CY25, with renewables accounting for a significant share. NGEL itself is delivering robust monetary metrics with income from operations rising 19% YoY in H1FY26 to Rs.1,292 crore, with working EBITDA margins at 88%, underscoring the inherent profitability of the renewable portfolio as soon as property are commissioned. Past renewable capability addition, NTPC is concurrently growing vitality storage infrastructure – NTPC has a 21,370 MW pumped storage pipeline, 5,000 MWh of BESS being deployed at thermal stations underneath the cost-plus framework incomes regulated returns and is commissioning the world’s second CO2-based vitality storage system at Kudgi alongside India’s first MWh-scale vanadium redox circulation battery.

- Operational Efficiency: Robust Availability Offsetting Softer Technology – Regardless of softer energy demand by way of a lot of 9MFY26, NTPC’s core operational metrics remained largely intact. Plant Availability Issue (PAF) remained primarily secure at 89.53% in 9MFY26 versus 89.11% in 9MFY25 and improved to 90.80% in Q3FY26 confirming that crops have been prepared and obtainable by way of the interval. On Plant Load Issue (PLF), coal stations operated at 70.69% in 9MFY26 versus an all-India common of 63.45%, an outperformance of 726 foundation factors. Standalone gross technology declined 5.7% YoY to 261.74 BUs, attributable to subdued demand throughout an prolonged monsoon season and grid restrictions, with restoration already seen as group technology grew 8.82% in December 2025. Common tariff realisation improved to Rs.4.89 per kWh from Rs.4.68 per kWh in 9MFY25. On receivables, excellent debtor days improved to 26 days as of December 2025 from 34 days a 12 months in the past, properly beneath the regulatory norm of 45 days. The important thing metric to observe going into FY27 is whether or not PLF recovers meaningfully as demand normalises – a sustained PLF beneath 70% would start to weigh on incentive revenue and total tariff realisations.

- Q3FY26 – Through the quarter, the corporate reported a income of Rs.45,856 crore, up 1.72% YoY. EBITDA was recorded at Rs.15,029 crore, up 5.7% YoY, and PAT grew 8% YoY to Rs.5,597 crore.

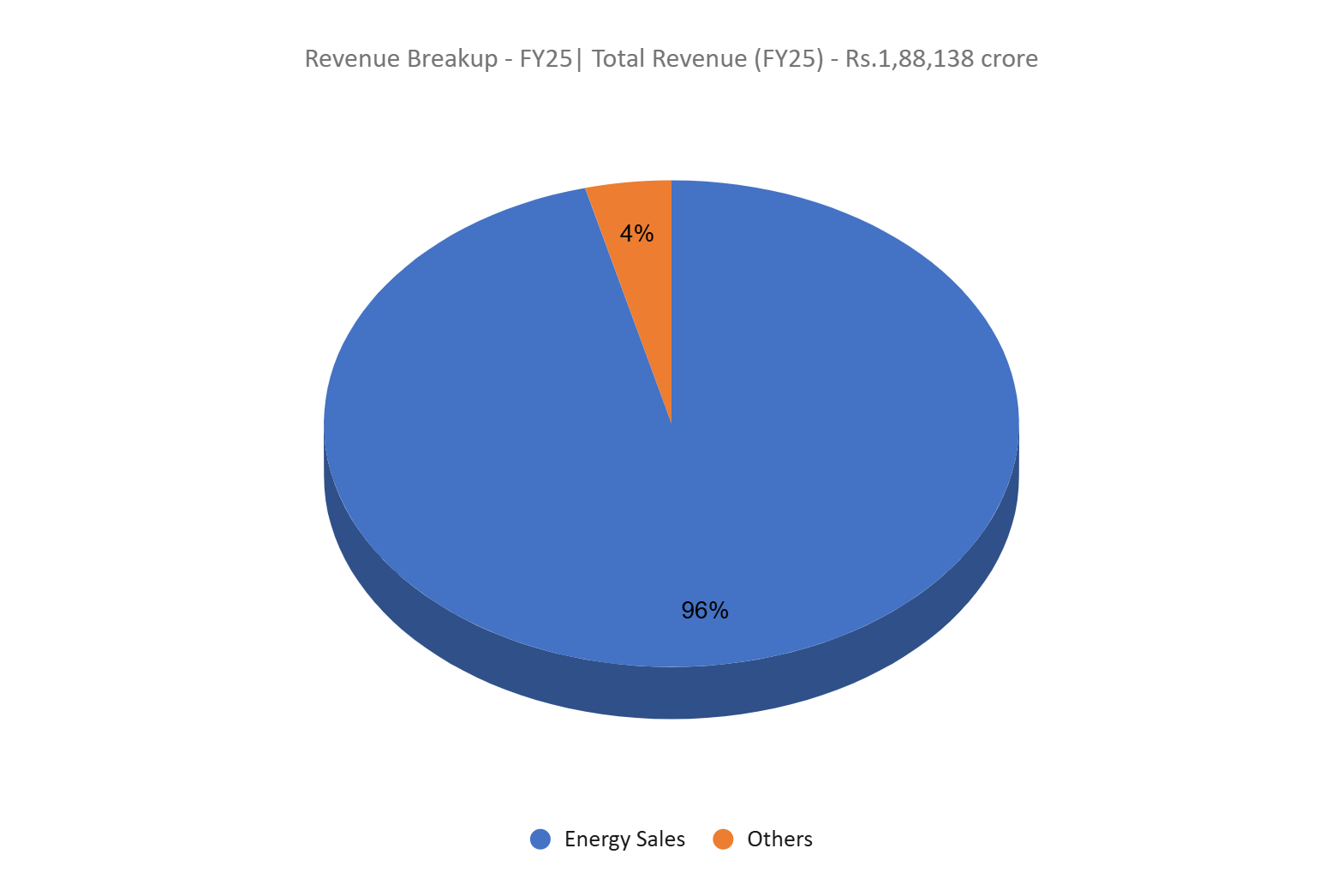

- FY25 – Throughout FY25, the corporate achieved a income of Rs.1,88,138 crore, translating to a YoY progress of 5.4% YoY. EBITDA elevated 6.6% YoY, to Rs.59,066 crore, and PAT grew 12.3% YoY to Rs.23,953 crore.

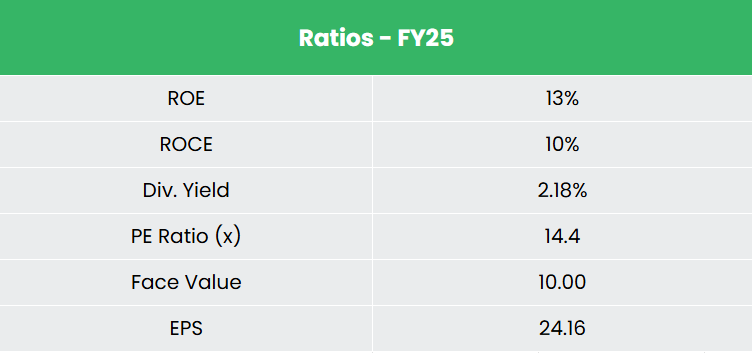

- Monetary Efficiency – The three-year income and web revenue CAGR stands at 12% and eight% respectively for FY22 – FY25. The corporate has a debt-to-equity ratio of 1.33, and the 3-year common ROE and ROCE stand at roughly 12.5% and 10% respectively for the FY22–FY25 interval.

Trade

India’s energy sector is the third largest globally by put in capability, with whole put in capability reaching 505 GW as of October 2025, compounding at ~6% yearly since 2016. Renewable vitality now accounts for ~50% of put in capability at 250.64 GW, with thermal at 245.6 GW remaining the dominant supply of precise technology. Whole energy technology in FY25 stood at 1,821 BU, up 5% YoY, whereas peak demand hit a report 250 GW in June 2025 in opposition to a projected FY26 requirement of 277 GW. The federal government targets 500 GW of non-fossil gas capability by 2030 alongside 80 GW of latest coal-based additions by 2031–32 to safe baseload reliability.

Development Drivers

- Rising energy demand: India’s electrical energy demand is predicted to develop 6 – 6.5% yearly over the following 5 years, pushed by industrial enlargement, rising per-capita consumption, and accelerating electrification. The CEA estimates peak requirement to achieve 817 GW by 2030.

- 100% FDI permitted within the energy sector: The facility section, together with renewable vitality, permits 100% FDI underneath the automated route, facilitating entry to international capital. Cumulative FDI inflows into India’s energy sector reached US$19.8 billion between April 2000 and June 2025.

- Authorities spending and coverage push: Union Price range FY26 allotted Rs.48,396 crore to the ability sector, a 30% improve YoY, with Rs.16,021 crore earmarked particularly for grid modernisation by way of sensible meter rollout and infrastructure upgrades underneath the Revamped Distribution Sector Scheme.

Peer Evaluation

Opponents: JSW Vitality Ltd, NHPC Ltd, and so on.

In comparison with the peer set, NTPC’s demonstrates decrease valuations at ~15x P/E and ~9x EV/EBITDA, reflecting its regulated, utility-like earnings profile with excessive visibility and restricted draw back threat. Throughout return metrics, NTPC leads the peer group with a ROCE of 9.95% and ROE of 12.13%.

Outlook

In keeping with CEA estimates cited by administration, peak demand is projected to the touch 575 GW by FY42, with vitality consumption rising at a CAGR of 5% over the FY32-FY42 interval offering a structural tailwind for India’s largest energy generator. NTPC has responded to this chance by revising its capability goal upward from 130 GW to 149 GW by FY32, backed by a cumulative group capex dedication of Rs.7 lakh crore. With 32,958 MW at present underneath building and consolidated regulated fairness already at Rs.1,18,970 crore as of December 2025, every successive commissioning milestone interprets instantly into a bigger regulated asset base and better mounted cost entitlements – giving earnings a level of ahead visibility that’s unusual within the broader energy sector. As NGEL’s monetary contribution to consolidated earnings turns into extra outstanding over the following 2-3 years, we consider there’s a credible case for re-rating of the consolidated entity. Past the near-term pipeline, NTPC’s entry into nuclear vitality with the inspiration stone of the two,800 MW Mahi Banswara undertaking laid in September 2025 and the SHANTI Nuclear Act offering a proper regulatory framework for enlargement represents a long-term choice that might meaningfully add to shareholder worth.

Valuations

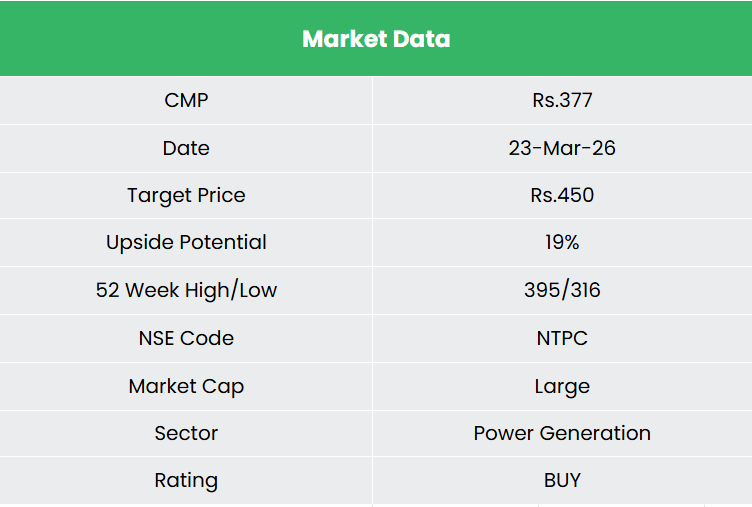

We consider NTPC Ltd. will be capable to capitalize on the surging energy demand throughout the nation. With its increasing thermal capability and renewables penetration, the corporate is poised to maintain its progress trajectory. We advocate a BUY ranking within the inventory with the goal value (TP) of Rs.450, 18x FY27E EPS. We additionally encourage sustaining a stop-loss at 20% from the entry value to handle potential draw back threat successfully.

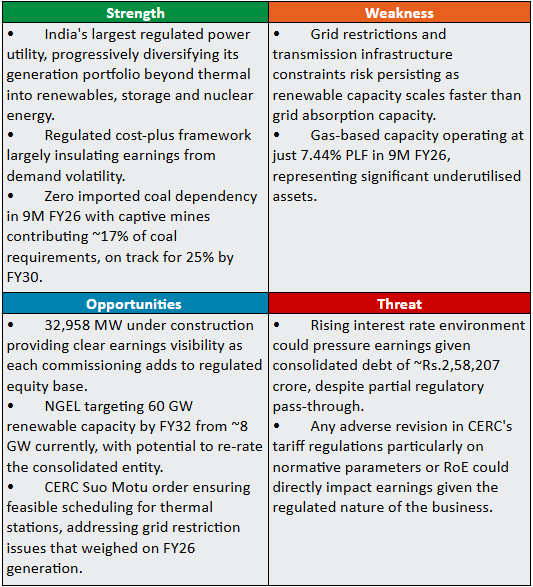

SWOT Evaluation

Disclaimer: Investments within the securities market are topic to market dangers, learn all associated paperwork fastidiously earlier than investing. Securities quoted listed below are exemplary, not recommendatory. Please seek the advice of your monetary advisor earlier than investing. Please word that we don’t assure any assured returns for the securities quoted right here.

Analysis disclaimer: Funding within the securities market is topic to market dangers. Learn all of the associated paperwork fastidiously earlier than investing. Registration granted by SEBI, and certification from NISM under no circumstances assure the efficiency of the middleman or present any assurance of returns to traders.

For extra particulars, please learn the disclaimer.

Different articles it’s possible you’ll like

Put up Views:

489