Editors notice: Since this submit was revealed, we clarified language within the first paragraph about year-ahead expectations for manufacturing and repair corporations within the 2025 survey. We additionally corrected the y-axis vary of Chart 2. (March 5, 11 a.m.)

After a interval of notably excessive inflation following the pandemic recession, inflationary pressures have been moderating the previous few years. Certainly, the inflation price as measured by the patron value index has come down from a peak of 9.1 p.c in the summertime of 2022 to 3 p.c at first of 2025. The New York Fed requested regional companies about their very own value and value will increase in February, in addition to their expectations for future inflation. Service corporations reported that enterprise value and promoting value will increase continued to reasonable by 2024, whereas manufacturing corporations reported some pickup in value will increase however not value will increase. Wanting forward, corporations anticipate each value and value will increase to maneuver increased in 2025. Furthermore, year-ahead inflation expectations have risen from 3 p.c final 12 months right now to three.5 amongst manufacturing corporations and 4 p.c amongst service corporations, although longer-term inflation expectations stay anchored at round 3 p.c.

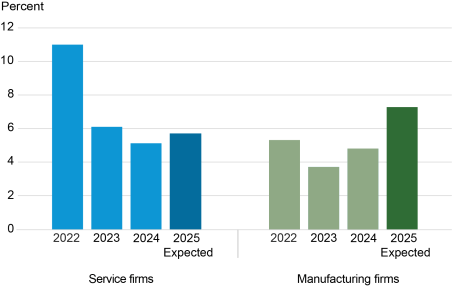

Enterprise Prices Have Come Down, however That Pattern Is Anticipated to Reverse

To gauge value and value will increase for regional companies, the New York Fed’s February regional enterprise surveys requested corporations within the New York-Northern New Jersey area about previous and anticipated adjustments of their enterprise prices and promoting costs, questions which now we have additionally requested in prior years. The typical annual value will increase reported over the previous 12 months on this 12 months’s survey—masking value will increase in 2024—in addition to in prior years’ surveys, are proven within the chart beneath.

Value Will increase Are Anticipated to Choose Up

Be aware: These averages signify a trimmed imply (the best 5 p.c and the bottom 5 p.c of responses are excluded).

The typical value improve for service corporations got here down from 11 p.c in 2022 to six.1 p.c in 2023 and fell additional to five.1 p.c in 2024. For manufacturing corporations, the typical value improve slowed from 5.3 p.c in 2022 to three.7 p.c in 2023 however picked as much as 4.8 p.c in 2024. Certainly, there have been important value will increase for numerous inputs over the course of 2024 reported by manufacturing corporations, together with metals corresponding to aluminum and copper, electrical energy and freight prices, in addition to espresso and chocolate amongst meals producers. Wanting forward, corporations anticipate extra important value will increase in 2025. On common, service corporations anticipate prices to rise at a 5.7 p.c tempo, whereas manufacturing corporations anticipate value will increase to rise 2.5 proportion factors to 7.3 p.c.

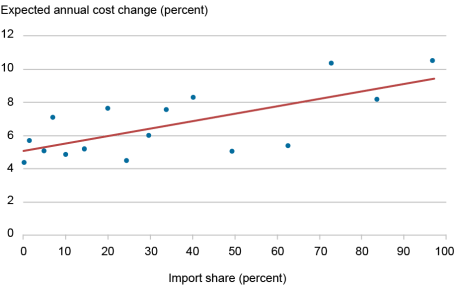

Imported Inputs Associated to Greater Value Expectations

This 12 months’s surveys have been within the subject from February 3 to 12, a interval throughout which a number of tariff bulletins have been made after which paused, with many corporations reporting that they have been unsure however involved about tariffs and their affect on prices. Certainly, increased value expectations have been associated to the import share of corporations’ inputs—a measure of potential publicity to tariffs. About 82 p.c of service corporations and 86 p.c of producing corporations within the survey reported some use of imported inputs, which speaks to the globally built-in nature of corporations within the U.S. financial system. Under we current a binscatter visualization which plots the connection between the share of inputs that corporations import and anticipated value will increase within the 12 months forward.

Anticipated Value Will increase Are Greater Amongst Corporations That Import Extra

A binscatter is basically a scatterplot, the place as a substitute of plotting every particular person response, responses are grouped into bins based mostly on import share, after which plotted in opposition to the corresponding common anticipated value improve for every bin. (For extra on the methodology, see “On Binscatter” in Employees Experiences; revealed additionally as Cattaneo et al. [2024]). The chart exhibits a optimistic relationship, which means that corporations with a better import share anticipate steeper value will increase within the 12 months forward. Certainly, the chart signifies that anticipated value will increase for these with no imports can be about 5 p.c, whereas those that import all of their inputs would anticipate value will increase of round 9 p.c.

Promoting Value Will increase Additionally Anticipated to Choose Up

Parallel to value will increase, the chart beneath exhibits common annual value will increase reported over the previous 12 months. Amongst service corporations, the typical annual value improve moved decrease in each 2023 and 2024 however is anticipated to rise from about 4 p.c to about 5 p.c over the subsequent 12 months. Amongst manufacturing corporations, the typical annual reported value improve was 3.2 p.c in each 2023 and 2024, however value will increase are anticipated to rise by over 2 proportion factors to five.4 p.c in 2025.

Value Will increase Are Additionally Anticipated to Choose Up

Be aware: These averages signify a trimmed imply (the best 5 p.c and the bottom 5 p.c of responses are excluded).

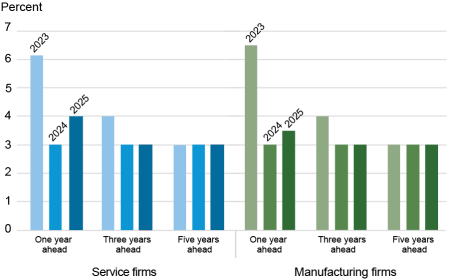

Greater Inflation Anticipated within the Yr Forward

With increased value and value will increase anticipated within the 12 months forward, expectations for general inflation within the financial system have additionally picked up relative to what was anticipated final 12 months right now, as proven within the chart beneath. Median year-ahead agency inflation expectations (based mostly on the CPI) climbed from 3 p.c in final February’s survey to 4 p.c amongst service corporations on this 12 months’s survey, and from 3 p.c to three.5 p.c amongst manufacturing corporations, each of that are increased than the CPI inflation price of 3 p.c reported in January. Longer-run inflation expectations at each the three-year and five-year horizons in our enterprise surveys have remained anchored at 3 p.c, each this 12 months and final 12 months. A rise in year-ahead inflation expectations in February has additionally been reported amongst customers in each the College of Michigan’s Survey of Shoppers and the Convention Board. The New York Fed’s Survey of Shopper Expectations will report its February knowledge in early March however inflation expectations had typically held regular by January 2025.

{kind=link}

Momentary or Persistent?

General, our February enterprise surveys confirmed a pickup in value and value expectations for 2025, in addition to year-ahead inflation expectations. Tariffs have been clearly on the thoughts of many companies. Nonetheless, longer-term agency inflation expectations remained anchored at 3 p.c, the identical as corporations have been anticipating final 12 months right now. Extra survey knowledge on inflation expectations within the months forward will assist make clear whether or not increased expectations are simply short-term or extra persistent.

Chart Information and Full Survey Outcomes ![]()

Jaison R. Abel is head of Microeconomics within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Richard Deitz is an financial coverage advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Ben Hyman is a analysis economist within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

The best way to cite this submit:

Jaison R. Abel, Richard Deitz, and Ben Hyman, “Corporations’ Inflation Expectations Have Picked Up,” Federal Reserve Financial institution of New York Liberty Road Economics, March 5, 2025, https://libertystreeteconomics.newyorkfed.org/2025/03/firms-inflation-expectations-have-picked-up/.

Disclaimer

The views expressed on this submit are these of the writer(s) and don’t essentially mirror the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the accountability of the writer(s).