{kind=link}

The beleaguered US housing market is displaying new indicators of pressure, with a surge in delistings, declining residence gross sales, and rising unsold inventories elevating considerations a couple of potential value correction. As reported in The Wall Avenue Journal, almost 73,000 properties have been pulled from the market in December 2024, a whopping 64 p.c enhance from the identical month a yr earlier. Regardless of a rise in accessible properties, the whole variety of residence gross sales fell to its lowest stage in almost thirty years, suggesting that demand has immediately dried up. Sellers of properties, that are normally the most important funding of a person’s life, are reluctant to decrease their costs and are as a substitute delisting properties in hopes of higher situations within the spring. There are in fact extremely seasonal components in housing market traits, and financial uncertainty beneath the brand new administration has vaulted up to now month, however there are deep structural points — together with mortgage fee lock-ins, regulatory constraints, and inflation-driven affordability challenges — distorting each the provide and demand sides of the housing market.

The persistence of mortgage fee lock-ins is one main issue. Owners who secured traditionally low mortgage charges throughout the pandemic are hesitant to promote, as transferring would imply taking over considerably increased borrowing prices. That alone has lowered the stock of properties in the marketplace and artificially inflated residence costs regardless of weakening demand. That impact can solely final till owners discover themselves pressured to maneuver resulting from job modifications, household wants, or different life occasions that may now not be postponed.

The variety of properties on the market in December 2024 rose by 16 p.c in comparison with the identical interval in 2023, indicating that some owners are lastly re-entering the market. Even so, many sellers are selecting to delist their properties reasonably than settle for decrease presents. The outcome has been a “shadow stock” of properties: these as soon as in the marketplace, now off, ready to be relisted. Ought to sellers with properties immediately be pressured into the market by some macroeconomic shock — a recession, or one thing of that nature — the sudden glut of properties hitting the market may put substantial downward strain on costs.

PMMS 30-year Mounted (black)

30-year Mortgage Nationwide Common (blue)

MB30 Index (orange), 2018 – current

(Supply: Bloomberg Finance, LP)

At current, new residence costs are beginning to decline, however not essentially resulting from an easing of market constraints. Builders, all the time aware of the traits in markets, are more and more constructing smaller, extra inexpensive properties for the first-time purchaser market. Whereas that helps some would-be owners, it underscores the broader affordability disaster. Some homebuilders are additionally providing incentives, akin to mortgage fee buy-downs (a financing association the place a homebuyer pays an upfront payment to a lender to completely scale back the rate of interest on a mortgage), however even these measures are proving inadequate in some instances.

The variety of accomplished however unsold new properties rose by almost 50 p.c in December in comparison with the earlier yr, reflecting the gaping mismatch between what potential homebuyers can afford and what the availability aspect of the market is providing. A smoother adjustment is perhaps discovered if there have been a rest or elimination of the restrictive net of zoning legal guidelines and allowing laws, which severely constrain the availability of housing in high-demand areas. With out reforms to those insurance policies, the market will proceed to battle to satisfy actual housing wants, and affordability challenges will persist, maybe worsening.

Inflation and rising mortgage charges are further obstacles to a housing market restoration. The typical 30-year mounted mortgage fee approached 7 p.c on the finish of 2024, making homeownership dearer and suppressing demand. Larger borrowing prices, alongside elevated residence costs, have stored many potential patrons on the sidelines. Uncertainty concerning the route of the economic system beneath the brand new administration, as seen within the sudden decline in each enterprise optimism and client sentiment, additionally play a job. Actual property funding corporations like Invitation Houses and American Houses 4 Lease are buying and selling at deep reductions to their asset values, indicating that buyers predict a housing market correction. The leap in delistings means that sellers would like to not minimize their itemizing costs, but when demand doesn’t return they’re prone to be pressured to take action. The longer that unsold residence stock stays excessive, the extra seemingly a broader housing market correction turns into.

New Dwelling Gross sales, Median Worth (violet)

S&P CoreLogic Case-Shiller US Nationwide Dwelling Worth Index (blue)

Annual US Housing Begins (orange)

US New Privately Owned Housing Items Began by Construction (black)

(The violet and blue traces signify two measures of median residence value traits over the previous 20 years, whereas the black and orange traces monitor housing begins. The sharp enhance in median residence costs, coupled with a decline in new residence development, is clear.)

A helpful financial idea to know these dynamics is the reservation value: the bottom value at which a vendor is keen to have interaction in a voluntary transaction. It’s sometimes a value that exists within the thoughts of a vendor or purchaser, as financial actors attempt to keep negotiating leverage and maximize their utility. Usually in a market downturn probably the most motivated sellers decrease their reservation value to satisfy patrons the place they’re. Within the present housing market, although, many sellers are reluctant to regulate their expectations downward, even within the face of weak demand. Because of this delistings have surged reasonably than outright value declines: sellers’ reservation costs stay above what patrons are keen to pay. To some extent, which will counsel optimism concerning the economic system broadly, or the housing market particularly. If housing market situations fail to enhance, sellers should scale back their reservation value or threat being unable to promote their properties. The longer the standoff persists, the higher the probability of a sharper value correction when sellers lastly capitulate.

The mortgage fee lock-in impact stems straight from the Federal Reserve’s resolution to pursue zero rate of interest insurance policies (ZIRP) throughout the pandemic, which has generated an unnatural incentive for tens of millions of house owners to remain put. Laws at many ranges — together with zoning legal guidelines, allow restrictions, environmental overview processes, and different hindrances — are persevering with to stifle housing provide, stopping the market from adjusting, not to mention clearing. And inflation, which has by some measures been rising because the Fed started decreasing charges in September 2024, has eroded buying energy and made homeownership all of the much less achievable. New residence development, as nicely, is being constrained by burdens that enhance prices and gradual the tempo and breadth of improvement.

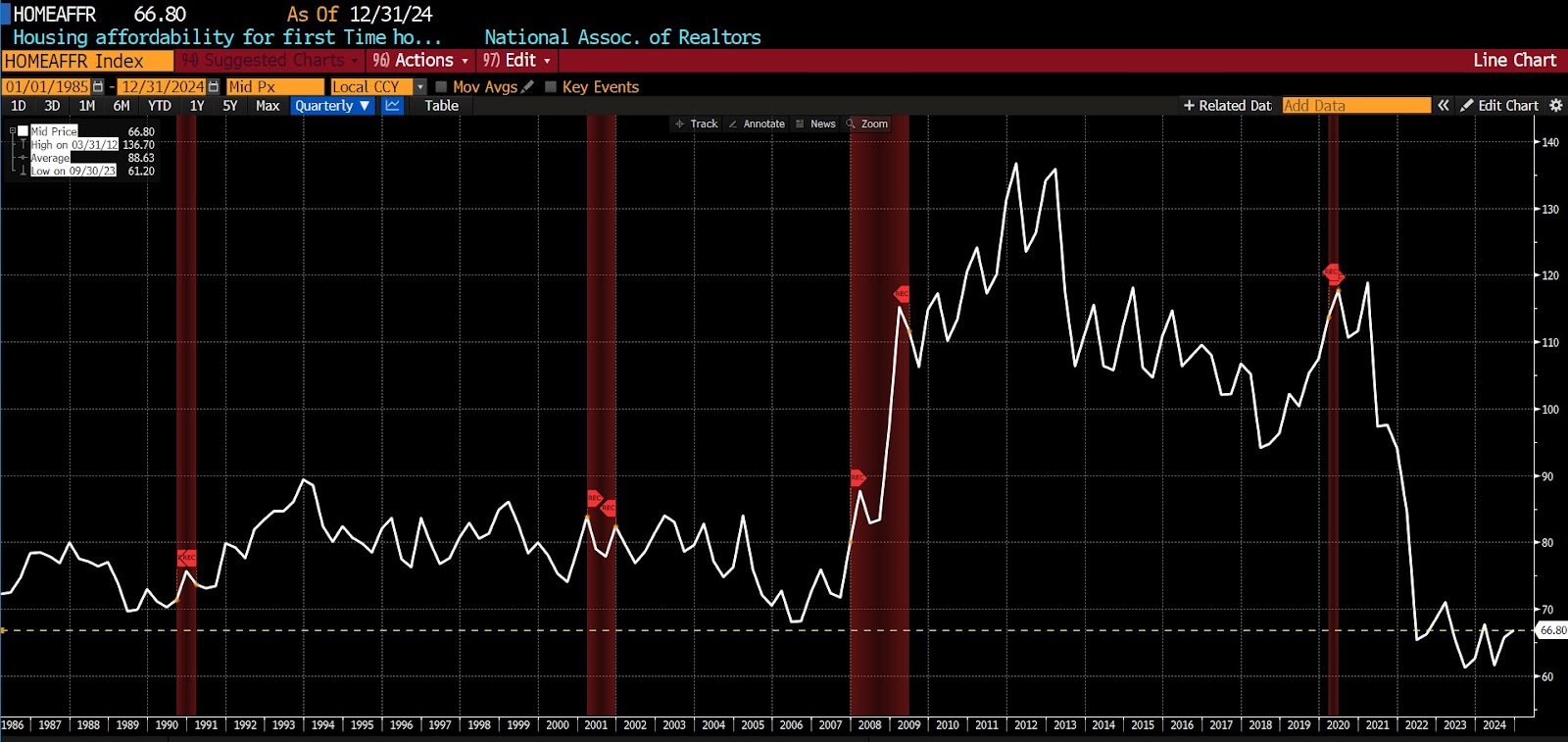

Housing Affordability for First Time Homebuyers, Nationwide Ass’n of Realtors, 1986 – current

(Though off the lows of late 2023 and mid-2024, residence affordability remains to be, in early 2025, decrease than it was within the depths of 2006.)

Permitting rates of interest to discover a pure equilibrium, whether or not that’s increased or decrease than the Fed-divined stage, would assist restore stability between each the availability and demand on the mortgage market and, subsequent to that, in housing. Rolling again restrictive zoning legal guidelines and easing or eliminating the allowing course of would permit builders to create extra housing the place it’s wanted most, sending market alerts to suppliers. And decreasing purchasing-power-destroying, budget-winnowing inflation would ease the disaster of affordability. In different phrases, let markets work as a substitute of ready for a “tender touchdown” or plotting one other spherical of grossly wasteful authorities stimulus.

The present wave of delistings, declining residence gross sales, and rising unsold stock are a warning signal that the US housing market is ailing and presumably sure for a pointy, maybe sudden drop in costs.

The consequences of the mortgage fee lock-in are fading, albeit slowly, but affordability stays a significant concern resulting from excessive rates of interest, regulatory constraints, and inflation. Sellers with excessive reservation costs could not have the ability to maintain out for much longer, and if all of them regulate their costs downward at roughly the identical time, it should ship a discounting cascade via the market. Making certain a wholesome, steady housing market requires permitting provide and demand to realign through market forces reasonably than imposing nonetheless one other layer of expensive, distortive guidelines to a market already piled excessive with them.