{kind=link}

LG Electronics India Ltd. – From Home to World

LG Electronics India Restricted, integrated in 1997, is amongst India’s largest shopper durables and electronics firms and the market chief throughout washing machines, fridges, air conditioners and televisions, together with the premium OLED phase. It operates by two segments – Residence Home equipment & Air Answer (air conditioners, fridges, washing machines, microwave ovens, dishwashers, and water and air purifiers) and Residence Leisure (televisions, audio-visual merchandise, screens and private computer systems). Anchored by a “Make in India, Make for India, Make India World” technique, it manufactures domestically and is constructing further capability by a brand new plant at Sri Metropolis, Andhra Pradesh.

Merchandise and Providers

LG Electronics India operates throughout two segments:

- Residence Home equipment & Air Options: Manufactures and markets fridges, washing machines, room air conditioners, microwave ovens, and dishwashers, with a rising B2B enterprise spanning business air-con and annual upkeep contracts.

- Residence Leisure: Affords panel televisions (together with OLED and large-screen premium codecs), screens, and knowledge show options resembling business signage and digital blackboards focusing on institutional and authorities prospects.

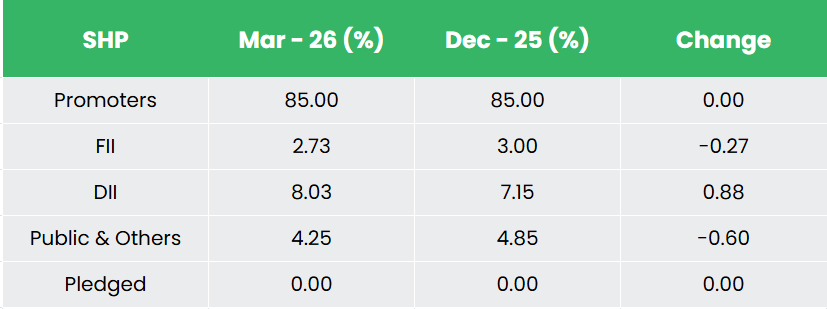

Subsidiaries – As of FY25, the corporate doesn’t have any subsidiaries or joint ventures.

Funding Rationale

- Export as an Incremental Progress Engine – The corporate is pivoting meaningfully in the direction of exports as a structural income diversifier, shifting past its core home franchise. The corporate has already made early inroads – large-capacity fridges are being exported to superior markets in Q1FY27, and the Important Sequence has been launched throughout neighbouring international locations, with distribution now spanning 22 export locations. Administration has reiterated steering to double export income in FY27, with a medium-term ambition to scale export contribution from the present ~7% of income to mid-teen ranges. The corporate is actively constructing a devoted export organisation and infrastructure, diversifying its product portfolio for worldwide markets, and increasing its distributor community. The macro tailwinds are beneficial: the India-US and India-EU commerce negotiations, mixed with LG’s world positioning of India as a producing hub beneath its “Make India World” technique, present a structural value benefit relative to competing export origins. Because the Sri Metropolis plant ramps up export-led income ought to add an incremental progress layer.

- Sri Metropolis: Capability, Localisation, and the Export Hub of the Future – Development of the corporate’s third manufacturing facility at Sri Metropolis, Andhra Pradesh is progressing in keeping with inside timelines, with compressor manufacturing scheduled for Q3FY27 and room air conditioner manufacturing commencing in Q4FY27. The ability, backed by a complete deliberate funding of ₹50 billion, is being positioned as each a home capability enlargement and a devoted premium export hub – immediately supporting administration’s aim of doubling exports and decreasing dependence on imported parts. What makes Sri Metropolis significantly compelling from a capital allocation standpoint is the funding construction: with a money and financial institution stability of ₹44.76 billion as of March 2026, LG India has the complete capability to fund this funding by inside accruals, avoiding dilution or leverage. The plant may even strengthen LG’s presence within the high-growth South India market, scale back pan-India logistics prices, and supply the manufacturing base to introduce compressor localisation. As the ability strikes from capex to income era by FY27 and FY28, it ought to function a tangible re-rating set off, changing the present funding overhang into seen capacity-led earnings progress.

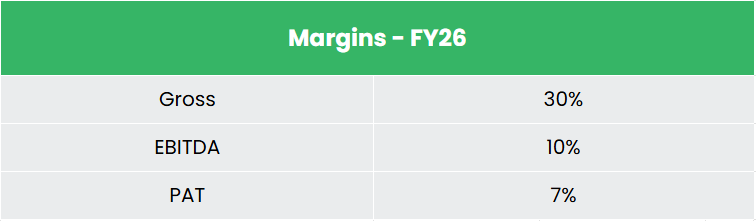

- Premiumisation and Margin Restoration – FY26 margins had been compressed by a confluence of transitory headwinds – rupee depreciation, elevated copper and aluminium costs, and deliberate channel funding spend of ~110 bps, however the underlying product combine trajectory factors firmly in the direction of margin enlargement. Premium classes drove incremental income in FY26: totally automated washing machines, French door fridges, and 5-star rated ACs all delivered increased common promoting costs, whereas the dishwasher enterprise doubled its income as city shoppers more and more undertake the class. In televisions, LG instructions a dominant 60% OLED market share, insulating it from volume-driven worth competitors on the premium finish. Past the product combine, two structural margin drivers are gaining scale: the AMC (Annual Upkeep Contract) enterprise, which is a high-margin recurring income stream deepening post-sale buyer relationships, and the B2B phase, which is seeing robust order inflows from authorities infrastructure, IT parks, business actual property, and the hospitality sector. Localization, now at 55.2% and guided to enhance 1 – 2 share factors yearly, will progressively scale back FX sensitivity and import-led value volatility. Administration has guided FY27 EBITDA margins at early-teen ranges, broadly restoring FY25 profitability.

- Q4FY26 – Through the quarter, the corporate reported consolidated income of ₹8,054 crore, up 8.1% YoY from ₹7,448 crore in Q4FY25 (and up 95.7% QoQ on the seasonal cooling-led upcycle). EBITDA stood at ₹945 crore, down 9.8% from ₹1,048 crore within the corresponding quarter, with EBITDA margin compressing to 11.7% (versus 14.1% in Q4FY25). Internet revenue got here in at ₹693 crore, down 8.2% YoY from ₹755 crore in Q4FY25. The roughly 250 bps margin contraction mirrored strategic channel-promotion investments, rupee depreciation and elevated commodity prices, alongside increased e-waste compliance prices, whilst document 1 million-plus air-conditioner gross sales and a richer premium combine drove the topline.

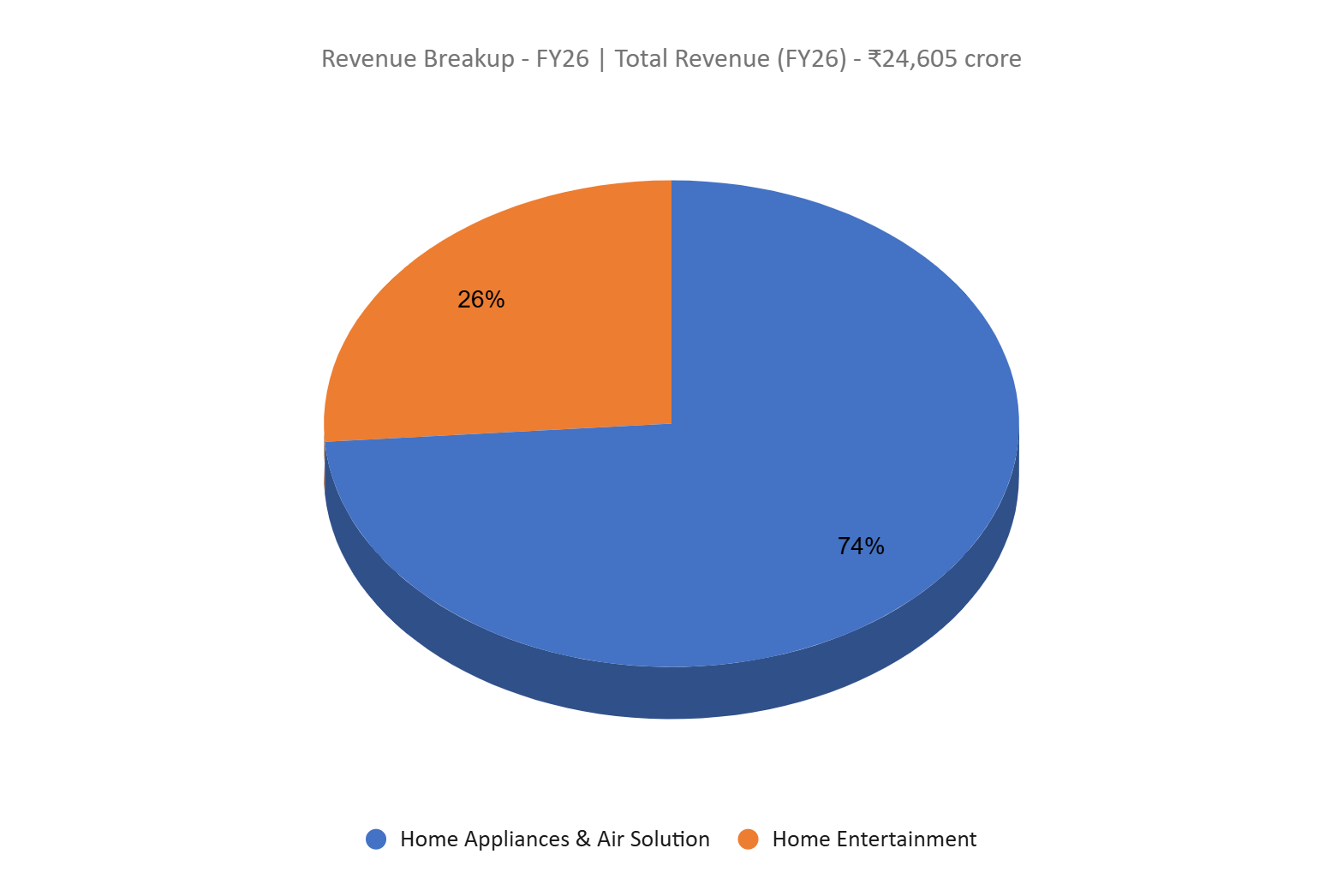

- FY26 – Throughout FY26, the corporate generated consolidated income of ₹24,605 crore, a rise of 1.0% over FY25. EBITDA stood at ₹2,408 crore, down 22.6% YoY, with EBITDA margin at 9.8%. The corporate reported a internet revenue of ₹1,685 crore, down 23.5% YoY.

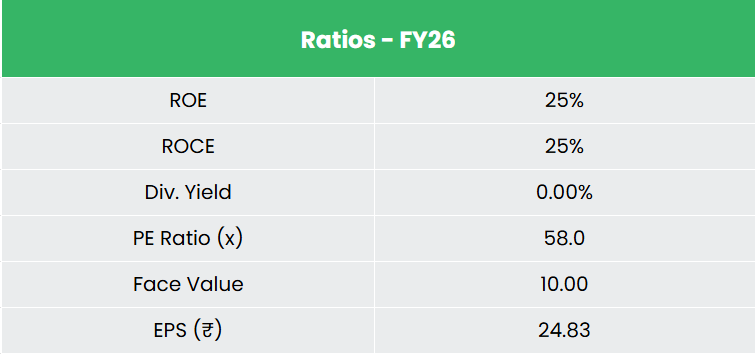

- Monetary Efficiency – The three-year income and internet revenue CAGR stands at round 7% and eight% respectively between FY24-26. The corporate is successfully debt-free, with a debt-to-equity ratio of about 0.06 comprising solely lease liabilities. The three-year common ROE and ROCE are round 34% and 45% for the FY24-26 interval.

Trade

India’s shopper durables sector is among the many fastest-growing pillars of the nation’s manufacturing economic system, supported by rising disposable incomes, low family penetration, premiumisation and a sustained “Make in India” push towards import substitution. The home equipment and shopper electronics market was valued at round US$ 75 billion in 2024 and is projected to almost double to roughly US$ 149 billion by 2033, compounding at about 7.7%. The market is broadly break up between shopper electronics (brown items) and shopper home equipment (white items), with the white-goods phase extremely concentrated – the highest 5 gamers maintain over 75% of the washer and fridge markets and round 55-60% in air conditioners and followers. Presently contributing about 0.6% of GDP, the sector is predicted to turn out to be the world’s fourth-largest shopper durables market by FY27, rising at an ~11% CAGR, with demand more and more led by premium, large-screen and energy-efficient merchandise, current GST price cuts, and quicker offtake from rural and semi-urban markets.

Progress Drivers

- 100% FDI is permitted beneath the automated route for electronics {hardware} manufacturing, supporting capability build-out and the localisation of worldwide provide chains in India; digital items attracted cumulative FDI inflows of ₹56,651.88 crore (US$ 7.67 billion) between April 2000 and December 2025.

- GST price cuts efficient September 2025 – together with a discount on televisions above 32 inches from 28% to 18%, alongside cuts on room air conditioners have revived demand and accelerated premiumisation and large-screen adoption, with some producers reporting 30 – 35% gross sales progress on the primary day of the brand new charges.

- The Manufacturing-Linked Incentive (PLI) scheme for white items (air conditioners and LED lighting), with an outlay of ₹6,238 crore, continues to deepen home manufacturing and part localisation.

Peer Evaluation

Opponents: Whirlpool of India Ltd, Voltas Ltd and so on.

In contrast with its peer set, the corporate combines one of many largest scales within the listed Indian consumer-durables house with a markedly superior return profile and category-leading market positions, generated on a debt-free, cash-rich stability sheet.

Outlook

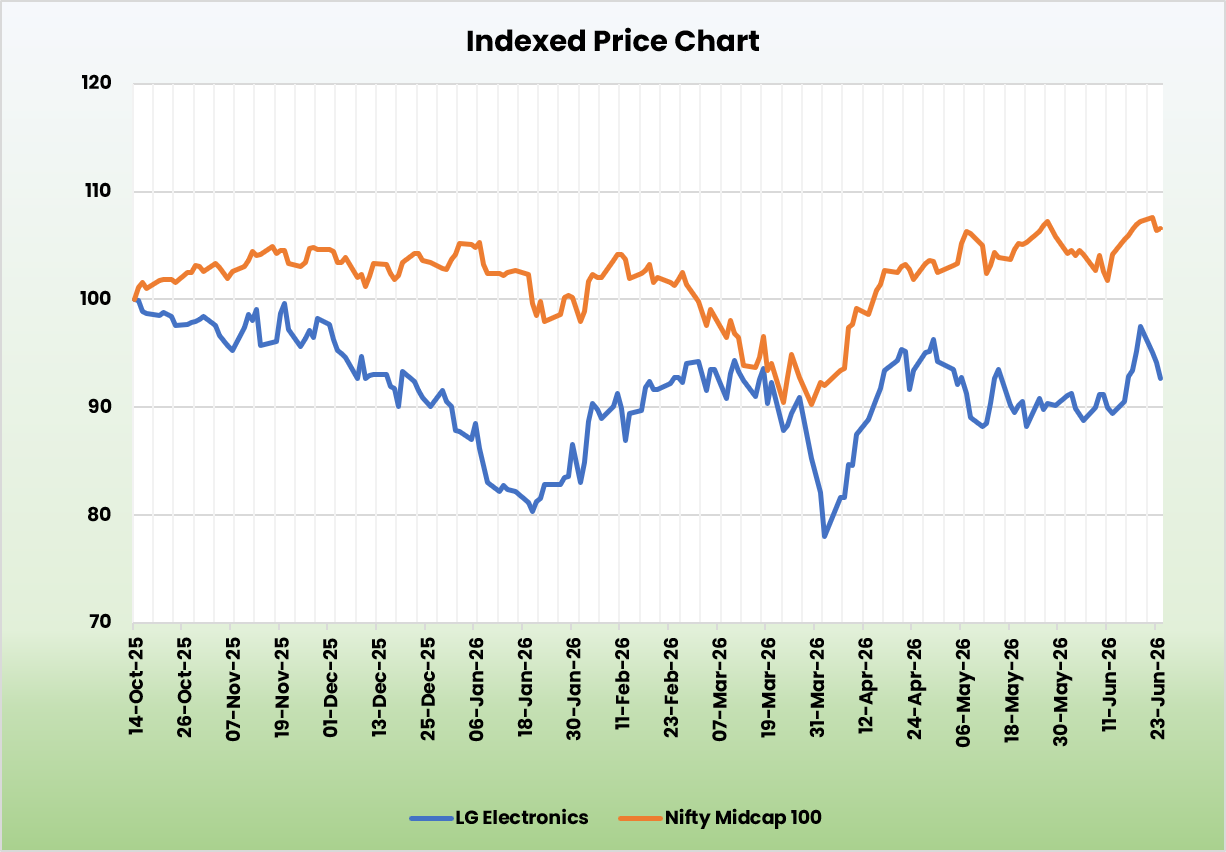

Having delivered its highest-ever quarterly income in Q4FY26, LG Electronics India enters FY27 with seen demand momentum – room air conditioners and washing machines are seeing robust early-season offtake, with premium fridges together with side-by-side and French door fashions including incremental combine uplift. Administration has guided for mid-teen income progress in FY27, underpinned by a two-track technique that concurrently scales premium classes and addresses the mass-premium phase by the Important Sequence. On margins, the corporate targets early-teen EBITDA ranges in FY27 – an enchancment over FY26 – supported by industry-wide worth will increase already underway, progressive localization features, and the gradual unwinding of the channel funding spend that weighed on FY26 profitability. The Sri Metropolis plant commissioning, with compressor manufacturing anticipated in Q3FY27 and RAC strains in Q4FY27, provides a capability and export dimension to the expansion outlook that ought to turn out to be incrementally earnings-accretive by FY28.

Valuations

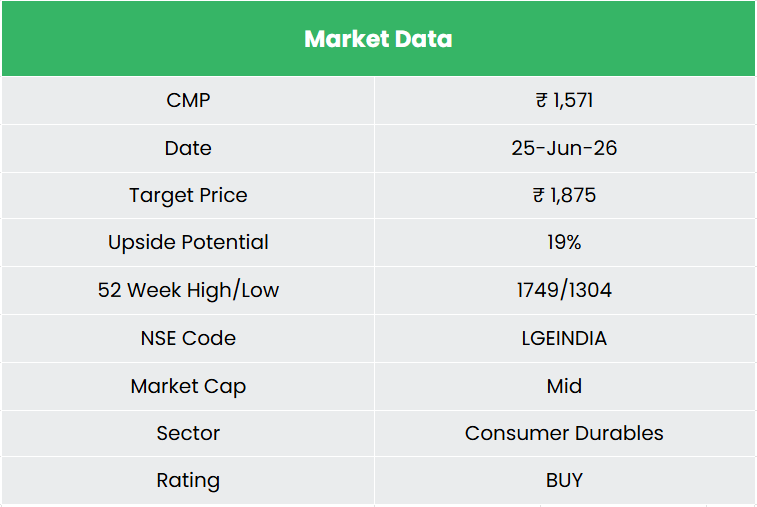

LG Electronics India stands at an inflection level – market management, a self-funded Sri Metropolis enlargement, and an export ramp converging to drive a structural earnings improve over FY27-28. We advocate a BUY score within the inventory with the goal worth (TP) of ₹1,875, 51x FY28E EPS. We additionally encourage sustaining a stop-loss at 20% from the entry worth to handle potential draw back danger successfully.

SWOT Evaluation

| Power | Weak point |

|

|

| Alternatives | Threats |

|

|

Disclaimer: Investments within the securities market are topic to market dangers, learn all associated paperwork fastidiously earlier than investing. Securities quoted listed below are exemplary, not recommendatory. Please seek the advice of your monetary advisor earlier than investing. Please word that we don’t assure any assured returns for the securities quoted right here.

Analysis disclaimer: Funding within the securities market is topic to market dangers. Learn all of the associated paperwork fastidiously earlier than investing. Registration granted by SEBI, and certification from NISM under no circumstances assure the efficiency of the middleman or present any assurance of returns to traders.

For extra particulars, please learn the disclaimer.

Different articles it’s possible you’ll like

Publish Views:

167