{kind=link}

By Stacey Pogue and Abigail Knapp

It’s the beginning of charge evaluate season for state insurance coverage departments. Though most proposed premium charges for 2027 Market protection should not as a consequence of federal regulators till mid-July and won’t be public till the top of July, some state regulators require insurers to submit proposed charge filings in Might or June and launch various ranges of knowledge early within the course of. These early charge filings present an preliminary have a look at how insurers are responding to market developments, comparable to rising well being care prices, in addition to coverage adjustments that have an effect on Market premiums.

Final yr, a trio of federal coverage adjustments—expiration of enhanced premium tax credit, enactment of H.R. 1 (additionally known as the “One Huge Lovely Invoice”), and adoption of the federal “Market integrity” rule—precipitated unprecedented web (after federal subsidies) premium will increase and contributed to the biggest proposed common gross premium will increase in almost a decade.

As insurers develop their 2027 charges this spring, they have to deal with federal coverage adjustments which might be inflicting upheaval within the particular person market. The person market is projected to shrink by 17% – 26% this yr, with ongoing implications for 2027 charges.

Insurers should additionally deal with uncertainty stemming from the annual federal Market rule replace, referred to as the Discover of Profit and Cost Parameters (NBPP). This yr, the Facilities for Medicaid and Medicare Providers (CMS) not solely adopted large-scale adjustments within the NBPP, however did so later within the yr than standard, after charges have been due in some states.

The next is a roundup of knowledge from proposed 2027 Market charge filings made publicly out there up to now, which offer some early clues in regards to the trajectory of and causes behind 2027 Market charge will increase.

Double-digit proposed charge will increase proceed in 2027

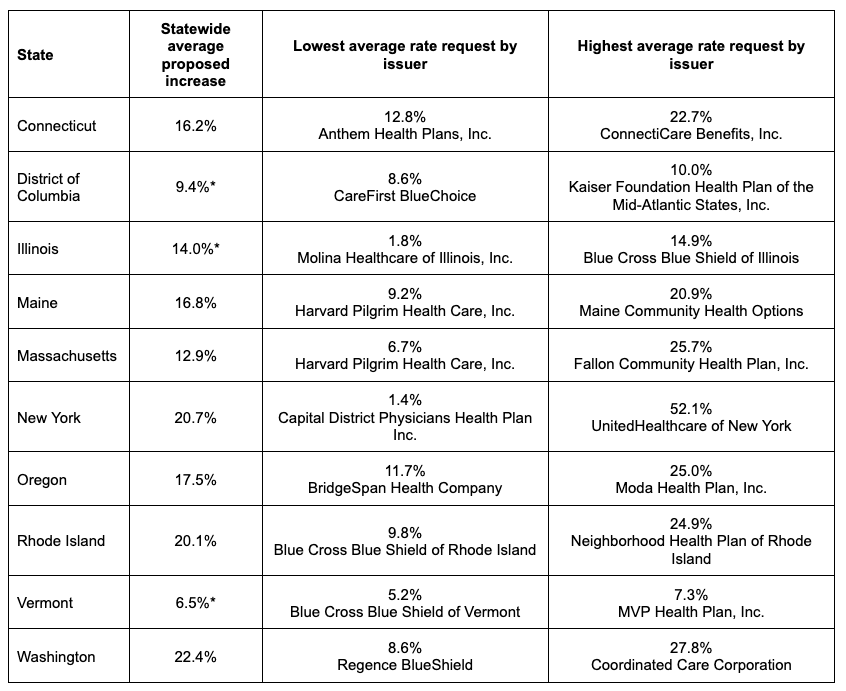

Early charge filings for 2027 Market plans sign charge will increase for subsequent yr, typically substantial ones. Statewide common proposed 2027 will increase launched so far vary from 6.5% in Vermont to 22.4% in Washington.

These statewide averages are usually akin to the numerous proposed charge will increase seen in states’ early filings final yr. Final yr’s nationwide median proposed improve of 18% was the very best in almost a decade, and almost triple the median proposed will increase from the 2 prior years (6% in 2024 and 7% in 2025).

2027 Proposed Market Price Will increase

Notice: Knowledge mirror 2027 ACA particular person market (or Massachusetts merged market) charge filings that embrace Market plans made publicly out there as of June 15, 2026. Statewide common proposed charge change as calculated by the state, the place out there. These marked with an asterisk (*) are a weighted common utilizing enrollment data from 2027 charge filings. See linked supply supplies for additional data. Connecticut, District of Columbia, Illinois, Maine, Massachusetts, New York, Oregon, Rhode Island, Vermont, and Washington.

With a median requested improve of twenty-two.4 %, insurers in Washington are in search of probably the most vital statewide charge hike up to now. “I do know the requested charge adjustments might be tough for people and households,” stated Insurance coverage Commissioner Patty Kuderer. “We’re going to spend the following a number of months reviewing each assumption made by the insurers to ensure their requests are justified.” Enrollment by way of the Washington Well being Profit Change has declined 13% since 2025, a development primarily attributed to the expiration of enhanced premium tax credit (ePTC).

Oregon regulators additionally acknowledged the affect of ePTC expiration on declining enrollment and proposed charge will increase. “Oregon shoppers are dealing with difficult instances with expiring premium tax credit, rising medical insurance charges throughout the nation, and two carriers leaving the Oregon market,” stated TK Eager, Oregon’s Insurance coverage Commissioner.

Excessive prices and market uncertainties result in provider exits

At the very least six insurers have introduced that they may exit ACA Marketplaces in plan yr 2027: Cigna Well being, CareSource, PacificSource, Baylor Scott and White, Windfall Well being, and Mending (previously Taro Well being). Because of this, roughly 650,000 folks throughout a 3rd of states might want to choose new plans subsequent yr.

Insurers cited rising prices, declining enrollment, and coverage uncertainty as components behind their selections. Cigna president and incoming chief government Brian Evanko indicated that there was no “clear path” to scale the corporate’s ACA enterprise, which has been shrinking lately; enrollment in Cigna Market plans dropped 17% in comparison with the primary quarter of 2025. A spokesperson for PacificSource indicated that rising well being care prices have turn into unsustainable, whereas Baylor Scott & White pointed to particular person market “complexities.” Windfall CEO Erik Wexler famous that adjustments in state and federal regulation have made it more and more tough for regional, not-for-profit well being plans like Windfall to thrive. “In the meantime, the bigger insurance coverage corporations have consolidated considerably, giving them the dimensions and sources to function extra effectively. This has left us in an untenable scenario,” stated Wexler.

As insurers exit the ACA Marketplaces, shoppers are left with fewer selections for protection. With the exits of Windfall and PacificSource, solely 4 insurers will supply Market plans in Oregon. Nevertheless, Oregon’s insurance coverage commissioner famous that customers in each county can have at the least three choices to select from. Exits additionally create uncertainty for insurers that stay out there, as they’ve little perception into the chance profile of shoppers newly enrolling of their plans.

Insurers level to federal insurance policies and better medical prices as driving charge will increase

A handful of states publish the detailed supporting documentation filed by insurers comparatively early in comparison with different states. These paperwork clarify the assumptions utilized by insurers and their justifications for proposed charge adjustments. We reviewed 40 insurer justifications from eight of those states, Connecticut, the District of Columbia, Illinois, Maine, Massachusetts, Oregon, Vermont, and Washington, to higher perceive the first drivers of 2027 Market charge will increase.*

As was true final yr, insurers in our pattern of 2027 charge filings steadily cited rising well being care prices and impacts from the expiration of ePTCs as key drivers of proposed charge will increase.

Expiration of enhanced premium tax credit pushes some charges increased for the second yr

Between 2021 and 2025, Congressional motion enhanced the generosity of the ACA’s premium tax credit. These ePTCs made Market protection rather more reasonably priced, resulting in document Market enrollment—24 million folks—in 2025. Congress failed to increase ePTCs, they usually expired on the finish of 2025.

Most insurers pointed to the top of ePTCs as a key contributor to massive 2026 charge will increase, driving charges 4% to 6% increased on common than they in any other case would have been. In 2026 charge filings, insurers anticipated that more healthy folks can be extra more likely to drop protection as web premiums rise. Remaining enrollees can be sicker on common—known as elevated “morbidity” by insurers—rising common claims prices and driving up charges.

Early charge filings sign that charge impacts from the top of ePTCs will proceed into 2027. Insurers in our pattern steadily pointed to the expiration of ePTCs as a key issue behind 2027 proposed charge will increase, with many pointing to a smaller, sicker threat pool. Mass Normal Brigham Well being Plan in Massachusetts explains that the top of ePTCs decreased “the monetary help that beforehand made medical insurance extra accessible,” resulting in “the lack of lower-risk members.” Neighborhood Well being Plan of Washington famous declining enrollment in 2026 and “anticipate[s] additional market dimension discount in 2027.” It expects “the remaining threat pool in 2027 to have increased healthcare wants, on common.”

Insurers additionally pointed to rising developments they’re monitoring to evaluate the impacts of ePTC expiration. MVP Well being Plan in Vermont believes it has not seen the “full affect” of expired ePTCs but, because it “proceed[s] to see retroactive protection terminations for non-payment of premium.” Blue Cross Blue Defend of Vermont stated the “massive” adjustment it made to mirror increased morbidity was knowledgeable by its evaluation of prior claims prices of people that had dropped protection as of February 2026. Along with decreased enrollment, Moda Well being Plan in Oregon has noticed “a shift in rising 2026 utilization developments,” associated to ePTC expiration.

Some filings quantified the impacts associated to expired ePTCs on 2027 charges. Fallon Neighborhood Well being Plan in Massachusetts famous that 3.3 proportion factors of its 25.7% proposed improve is because of morbidity impacts from coverage adjustments, together with expired ePTCs. ConnectiCare Advantages in Connecticut attributes a 5% premium improve to the scheduled expiration of ePTC-related state subsidies on the finish of 2026. (Connecticut carried out a short lived state-funded subsidy to backfill a portion of expired ePTCs in 2026, and the state directed insurers to imagine it expires as scheduled on the finish of this yr.) MVP Well being Plan of Vermont stated the adjustment it made for elevated morbidity from the expiration of ePTCs interprets to a further $48 per member per 30 days in claims prices.

2027 NBPP provides a layer of uncertainty

The not too long ago adopted 2027 NBPP consists of broad adjustments that CMS tasks will cut back enrollment by 1.2 to 2 million folks subsequent yr, together with further paperwork burdens at enrollment, will increase in plans’ out-of-pocket prices, and erosion of ACA shopper protections. Modifications within the rule can have implications that insurers want to contemplate as they set 2027 premiums. For instance, in feedback on the proposed rule, insurers and state regulators raised considerations that some provisions may trigger more healthy people to depart the chance pool, resulting in increased premiums.

The later-than-usual timing of the rule creates challenges for insurers and regulators in the course of the charge evaluate course of. CMS printed the proposed rule on February 11, 2026, as insurers have been creating 2027 plans and charges, and adopted it on Might 20, 2026, after plans and charges have been due in some states. Including to uncertainty, a coalition of cities, physicians, and small companies filed a lawsuit on June 3, 2026, difficult lots of the rule’s provisions. An identical lawsuit from final yr resulted in a keep of many provisions, together with some much like these adopted within the 2027 NBPP. State and federal regulators might enable insurers to refile their charges to account for altering insurance policies by way of August 12, 2026.

Just a few filings in our pattern mentioned impacts–whether or not projected or unknown–from the 2027 NBPP. Just a few filings reference uncertainty in regards to the final impacts. Blue Cross Blue Defend of Vermont, for instance, famous uncertainty as a result of, when it submitted its proposed charges, the NBPP “ha[d] not been finalized but.” Coordinated Care Company of Washington signifies it “will search regulatory approval to file revised charges” if “materials score impacts” come up, together with from threat adjustment updates within the 2027 NBPP.

Each insurers in Vermont famous impacts from increasing catastrophic plan eligibility (past primarily folks underneath age 30), as codified within the 2027 NBPP. MVP Well being Plan of Vermont proposed a 109% premium improve for its catastrophic plan. It alluded to traditionally decrease charges for its catastrophic plan when such plans have been restricted primarily to folks underneath age 30, however anticipates that broader eligibility will shift the chance profile of catastrophic plan enrollees to be much like that of metal-level ACA plans.

Just a few insurers alluded to challenges utilizing the particular methodology for calculating value sharing discount funds required by the rule. For instance, Neighborhood Well being Choices in Maine acknowledged the strategy spelled out within the regulation, however famous that it “acquired approval from the Maine [Bureau of Insurance] to make use of an estimation method” as an alternative.

Rising value developments contribute to charge will increase

Growing well being care prices are a key driver of medical insurance charge adjustments in 2027, as they’re in most years. Price filings embrace insurers’ assumptions in regards to the year-over-year change in well being care prices, known as medical value development (or “development”). Parts of development embrace anticipated adjustments to unit costs (the quantity insurers pay suppliers for well being care items and providers) in addition to utilization (the frequency or quantity of providers delivered). PwC tasks that development might be excessive in 2027, reaching 8.5% within the particular person market.

In early filings, insurers steadily attribute requested charge will increase to increased supplier reimbursements, better utilization, and normal medical value inflation. UnitedHealthcare of Illinois famous that key well being care value developments embrace annual will increase in reimbursement charges to well being care suppliers. United additionally indicated that the variety of workplace visits and different providers continues to develop and that shifts within the depth of care and in using several types of well being care providers have an effect on its prices. Moreover, many insurers particularly cite rising pharmaceutical spending, significantly for high-cost specialty medication. Past pharmacy prices, just a few insurers talked about different particular providers impacting value developments, together with hospital stays, outpatient surgical procedures, and psychological well being/behavioral well being visits.

A few insurers famous that elevated supplier consolidation has contributed to rising prices. Premera Blue Cross in Washington indicated that, “excessive unit value will increase mirror continued stress from supplier contract negotiations, together with supplier requests for double-digit reimbursement will increase in sure markets.” It additional famous that restricted competitors and regional monopolies have decreased downward pricing stress.” Relatedly, Anthem Well being Plans in Connecticut argued that the state’s well being care value development benchmark fails to completely account for components driving up well being care prices, together with however not restricted to “excessive value specialty medication and coverings, will increase in healthcare labor prices as a consequence of scientific workforce shortages, and supplier consolidation.”

Some insurers present detailed estimates that break down their development assumption into elements, together with well being care costs and utilization. When included in charge filings, the affect of supplier reimbursements versus utilization on general value development varies throughout states and insurers. As an illustration, insurers in Oregon usually indicated that costs had a better affect on projected development than utilization, whereas components underlying development projections in Massachusetts have been extra combined. For instance, BridgeSpan Well being Firm in Oregon and Wellsense Well being Plan in Massachusetts each projected development close to 10% for 2027. Nevertheless, BridgeSpan projected that costs can have the best affect on development in 2027, whereas Wellsense projected that costs and utilization/mixture of providers delivered can have a comparatively equal affect.

Conclusion

The majority of 2027 Market charge filings should not but out there, however filings from early states foreshadow one other bumpy yr for ACA Marketplaces. Insurers are dealing with excessive well being care value development, vital drops in enrollment, a worsening threat pool, and an unstable coverage setting. Some ACA Market shoppers might be affected by insurer exits, and those that don’t qualify for monetary assist might face double-digit charge hikes. A extra full image of charges and insurer participation within the 2027 Market will emerge as charge submitting season progresses.

*Authors’ word: Our evaluate of publicly out there, early 2027 particular person market charge filings was largely restricted to the narratives within the actuarial memoranda that should accompany every charge submitting. These memos clarify, in lay language, insurers’ previous expertise, present assumptions, and predictions for the following plan yr. The findings summarized on this weblog should not essentially generalizable to the broader universe of particular person market charge filings for plan yr 2027, nor do they mirror all the components underlying charge requests or variations between insurers’ filings on this set of states. The authors thank Max Quan and Logan DeLeire for his or her help with charge submitting analysis and evaluate of the information.