{kind=link}

Rainbow Childrens Medicare Ltd. – It takes loads to deal with the little

Rainbow Youngsters’s Medicare Restricted (RCML), included in 1998 and headquartered in Hyderabad, is India’s largest pediatric multi-specialty hospital chain and one of many nation’s main perinatal care suppliers, working by means of its “Rainbow Youngsters’s Hospital” (pediatric and neonatal care) and “BirthRight by Rainbow” (obstetrics, fetal drugs and fertility) manufacturers. The group runs an built-in, full-time consultant-led community of 24 hospitals and 5 clinics throughout 9 cities in 6 states, aggregating 2,435 capability beds (together with the just lately commissioned 60-bed HRBR hospital, Bengaluru), organised on a hub-and-spoke mannequin. Its scientific focus spans pediatric secondary, tertiary intensive (NICU, PICU, ECMO) and quaternary care – together with pediatric cardiac surgical procedure, haemato-oncology, neurosciences, nephrology and organ transplantation (liver, kidney and bone marrow) alongside complete maternity and fertility companies. The community is anchored by JCI-accredited flagship hubs at Banjara Hills, Hyderabad and Marathahalli, Bengaluru.

Merchandise and Providers

The companies provided by the corporate fall primarily underneath two foremost divisions:

- Paediatric companies – Contains new child and paediatric intensive care, paediatric multi-specialty companies, paediatric quaternary care (together with organ transplantation) underneath “Rainbow Youngsters’s Hospital model.

- Girls care companies – Underneath the “Birthright by Rainbow” model, the corporate gives companies comparable to perinatal care companies which embrace regular and complicated obstetric care, multi-disciplinary foetal care, perinatal genetic and fertility care alongside gynaecology companies.

Subsidiaries – As of FY25, the corporate has 6 subsidiaries and no different three way partnership or affiliate firms.

Funding Rationale

- Capability Enlargement – Platform Constructed, Execution Part Begins: FY26 marked some of the aggressive capacity-building yr in Rainbow’s historical past, with the corporate including almost 500 beds (the very best annual addition on document), taking whole capability to 2,375 beds. This included the commissioning of Warangal (100 beds), Guwahati’s Pratiksha Hospital (150 beds), Rajahmundry (~100 beds), Digital Metropolis Bengaluru (~90 beds), HRBR Bengaluru (~60 beds), and a devoted IVF centre in Mahadevapura. With the present growth cycle now full, Rainbow’s subsequent pipeline of ~900 beds spanning Gurugram’s Sector 44 hub (~325 beds) and Sector 56 spoke (~125 beds), Coimbatore (~130 beds), Pune (~150 beds), Seegehalli Bengaluru (~80 beds), and Indore (~100 beds) is in energetic execution, with most services focused for commissioning within the subsequent 1-3 years. The Gurugram initiatives alone carry an estimated incremental capex of ₹400 – 500 crore, whereas the remaining pipeline is guided at ~₹65 – 70 lakh per mattress. Critically, administration confirmed that the total pipeline will likely be funded by means of inner accruals, with a money and liquid funding stability of ~₹594 crore and nil debt on the stability sheet as of March 2026, eliminating near-term fairness dilution threat. Bengaluru’s build-out – now six hospitals, one OPD clinic, and two devoted fertility centres positions Rainbow as the biggest paediatric and perinatal care community within the metropolis, validating the hub-and-spoke replication thesis past Hyderabad.

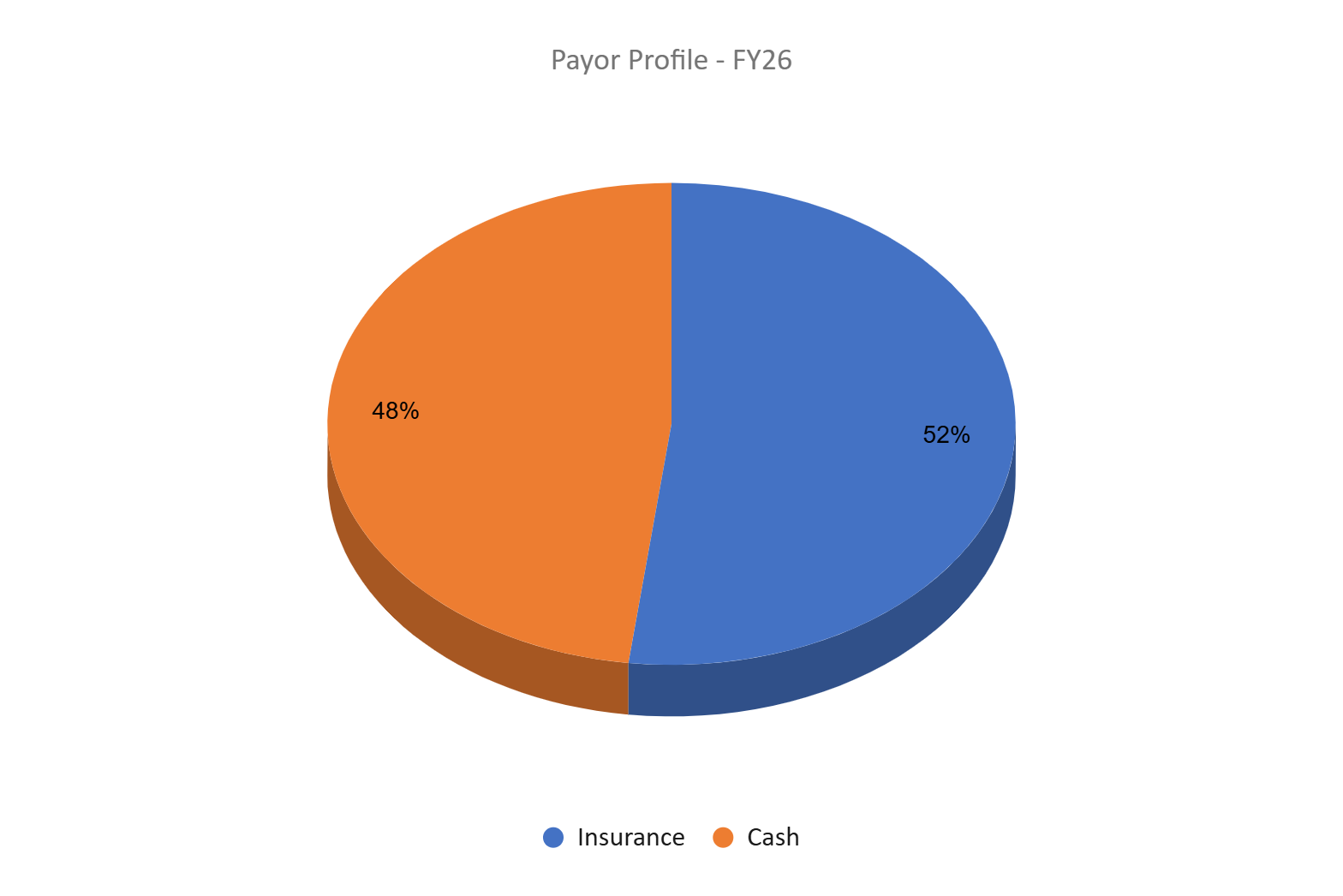

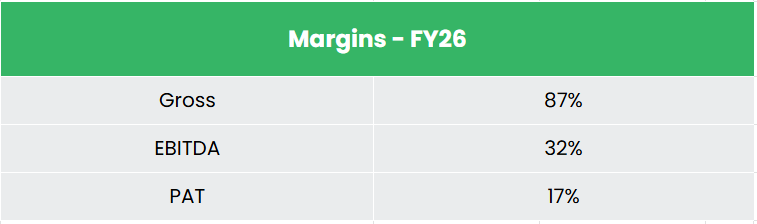

- Operational Metrics – Quantity Momentum Intact Amid Dilution from Ramp-Up: Rainbow’s quantity trajectory in Q4FY26 displays a enterprise working with wholesome underlying demand – inpatient discharges grew 18% YoY, outpatient consultations 19%, and deliveries 22%, with natural IP discharge progress at ~9 – 10% and the stability from acquired items. ARPOB expanded 8% YoY to ₹62,464, supported by a richer case combine, an rising share of obstetrics (~32% of income vs. ~28 – 30% traditionally), and a fast-growing IVF enterprise that contributed ₹61 crore in FY26 (3.7% of income, rising to 4.1% in This fall) and is guided to develop ~25% yearly over the following three years. Occupancy at 46.3% for FY26 is optically decrease than FY25’s 50.5%, however the 427 bps decline is arithmetic – the corporate absorbed ~440 incremental weighted operational beds by means of the yr; mature hospitals exited Q4FY26 at ~52% and administration is concentrating on a restoration to ~60% for the mature cohort in FY27, with blended community occupancy guided at 56 – 57%. ALOS at 2.71 days is structurally lean, and working money stream conversion at ~72% post-tax confirms that margin and money high quality have held – EBITDA margin stood at 31.5% in Q4FY26 regardless of ramp-up drag from six newly commissioned hospitals.

- Q4FY26 – Throughout This fall FY26, the corporate reported consolidated working income of ₹460 crore, up 24% YoY from ₹370 crore in This fall FY25. EBITDA rose 26% YoY to ₹145 crore from ₹115 crore, with EBITDA margin increasing to 31.5% from 31.0%, aided by a richer case combine, greater quaternary/surgical complexity and a rising fertility contribution. Internet revenue grew 38% YoY to ₹78 crore, although adjusted for a one-time deferred-tax credit score (~₹13 crore referring to subsidiary Rosewalk) underlying PAT progress was ~17%; the quarter was supported by broad-based quantity progress (inpatient discharges, outpatient volumes and deliveries up 18%, 19% and 22% YoY respectively), an 8% rise in ARPOB, and the ramp-up of newly commissioned items (Rajahmundry, Digital Metropolis, and the Mahadevapura IVF centre) alongside the combination of the acquired Warangal and Guwahati hospitals.

- FY26 – Throughout FY26, the corporate reported consolidated working income of ₹1,703 crore, a 12% YoY improve over ₹1,516 crore in FY25, with EBITDA up 11% to ₹544 crore at a broadly secure 32.0% margin (vs 32.3%) and internet revenue up 15% to ₹282 crore.

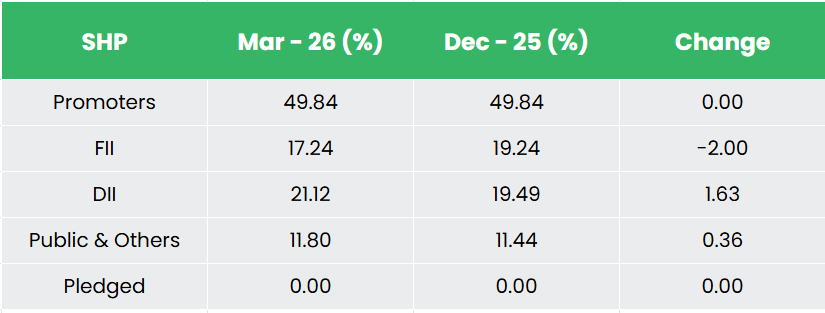

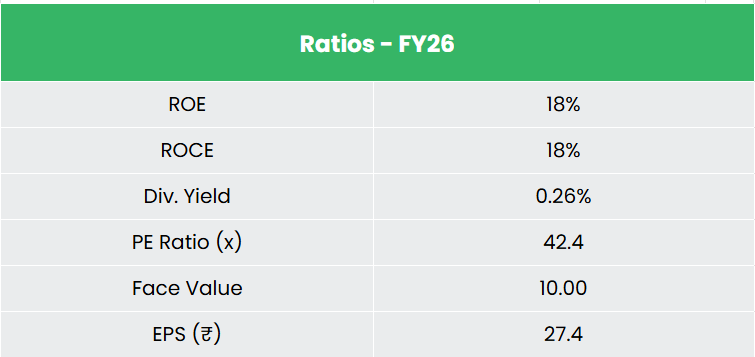

- Monetary Efficiency – The three-year income and internet revenue CAGR stands at 13% and 10% respectively between FY24-26. The corporate has a debt-to-equity ratio of 0.54. The three-year common ROE and ROCE are round 18% and 19% for FY23-25 interval.

Trade

The Indian healthcare sector is among the many fastest-growing segments of the home financial system, supported by beneficial demographics, rising earnings ranges, and bettering entry to medical companies. The sector is has seen unprecedented progress within the latest years, pushed by growth throughout hospitals, prescription drugs, diagnostics, and digital well being. Inside this, the hospital phase stays the biggest and most capital-intensive vertical. Healthcare spending in India continues to pattern upward, with whole expenditure anticipated to rise from 3.34% of GDP in 2023 to ~5% by 2030, whereas public sector help stays significant, mirrored in a ₹1,06,530 crore allocation within the Union Finances FY27. The mixture of structural demand progress, capability constraints, and coverage help continues to offer long-term visibility for organised hospital operators.

Development Drivers

- Capability Shortfall & Infrastructure Hole – India continues to face a scarcity of hospital infrastructure relative to its inhabitants, with mattress availability remaining under international benchmarks and coverage targets. This structural hole, mixed with rising utilisation of organised healthcare, helps sustained demand for capability growth by non-public hospital operators.

- Coverage Assist & Public Healthcare Spending – Authorities initiatives comparable to Ayushman Bharat and PM-ABHIM, together with a ₹1,06,530 crore allocation within the Union Finances FY27, proceed to enhance healthcare affordability and utilisation throughout private and non-private programs.

- Personal Capital & FDI Inflows – The sector advantages from liberal funding norms, with 100% FDI permitted underneath the automated route for greenfield initiatives, and cumulative FDI inflows of US$ 12.73 billion into hospitals and diagnostics between January 2000 and December 2025.

Peer Evaluation

Opponents: World Well being Ltd, Krishna Institute of Medical Sciences Ltd, and so forth.

In contrast with its friends, Rainbow stands out as the one listed pure-play pediatric and women-and-child hospital chain, with sector-leading EBITDA margins, a net-cash stability sheet, and wholesome, un-levered return ratios.

Outlook

Rainbow is at an inflection level – the capital-heavy build-out section is full, and the following two to a few years are about changing put in capability into earnings. With mature hospitals focused at ~60% occupancy in FY27 and a blended community occupancy steering of 56–57%, working leverage is the pure subsequent leg of the story. Past the core pediatric and perinatal enterprise, Rainbow is intentionally broadening its income combine by means of fertility and IVF companies – a phase that contributed ₹61 crore in FY26 and is predicted to develop at ~25% yearly, including a high-margin, much less seasonal earnings stream that structurally de-risks the enterprise over time. Geographic diversification into NCR, Maharashtra, and Central India by means of the ~900-bed pipeline additional reduces the South India focus that has traditionally outlined the corporate. Administration’s steering of ~17–18% income CAGR over a four-year interval, backed by a zero-debt stability sheet and self-financing progress plan, supplies a reputable and low-risk path to worth creation.

Valuations

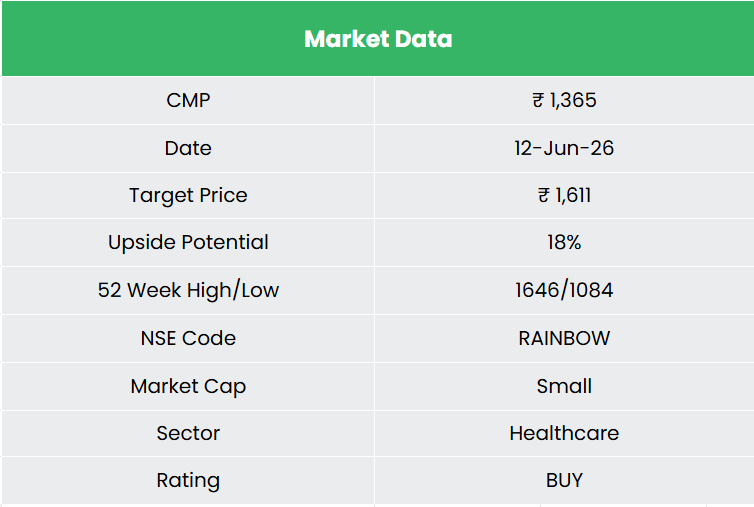

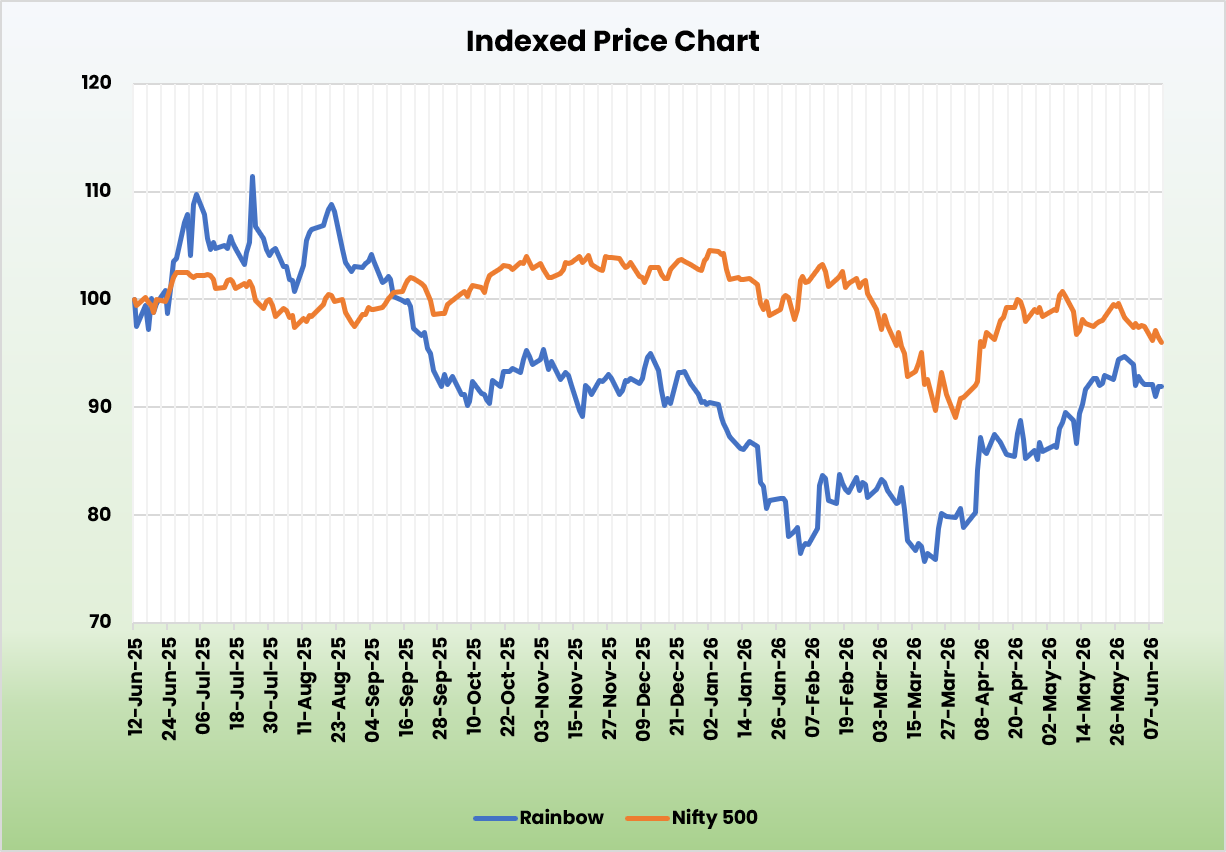

The paediatrics and maternity care market is poised for sturdy long-term progress, and Rainbow is predicted to learn from this pattern given its management place and growth-focused enterprise technique. We advocate a BUY score within the inventory with the goal worth (TP) of ₹1,611, 50x FY28E EPS. We additionally encourage sustaining a stop-loss at 20% from the entry worth to handle potential draw back threat successfully.

SWOT Evaluation

| Energy | Weak spot |

|

|

| Alternatives | Threats |

|

|

Disclaimer: Investments within the securities market are topic to market dangers, learn all associated paperwork fastidiously earlier than investing. Securities quoted listed below are exemplary, not recommendatory. Please seek the advice of your monetary advisor earlier than investing. Please be aware that we don’t assure any assured returns for the securities quoted right here.

Analysis disclaimer: Funding within the securities market is topic to market dangers. Learn all of the associated paperwork fastidiously earlier than investing. Registration granted by SEBI, and certification from NISM under no circumstances assure the efficiency of the middleman or present any assurance of returns to traders.

For extra particulars, please learn the disclaimer.

Different articles you could like

Submit Views:

222