{kind=link}

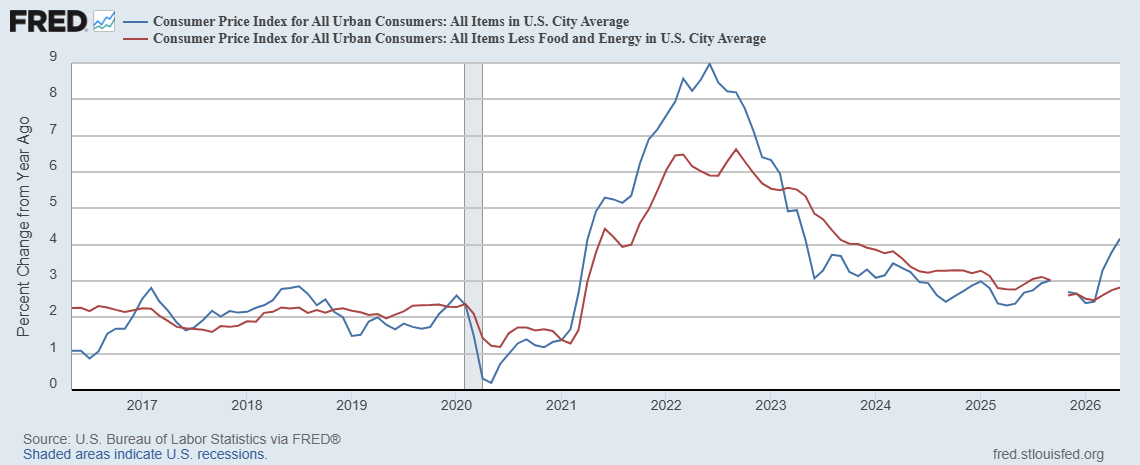

Inflation remained elevated in Could, the Bureau of Labor Statistics (BLS) reported yesterday. The Shopper Worth Index (CPI) rose 0.5 % final month, down barely from 0.6 % in April. However on a year-over-year foundation, headline inflation climbed once more, rising to 4.2 % from 3.8 % — the fourth straight month-to-month improve within the annual price and the very best studying in additional than a yr.

Core inflation advised a extra reassuring story. Excluding unstable meals and power costs, CPI rose simply 0.2 % in Could, half the 0.4 % tempo recorded in April. On a year-over-year foundation, core inflation ticked up solely barely, to 2.9 % from 2.8 %.

As in March and April, the hole between headline and core inflation got here right down to power. The power index rose 3.9 % in Could — after climbing 3.8 % in April and 10.9 % in March — and, based on the BLS, “accounted for over sixty % of the month-to-month all objects improve.” Gasoline costs rose 7.0 % over the month and are actually up 40.5 % over the previous yr, whereas the broader power index is up 23.5 %, reflecting the cumulative impact of the oil shock tied to the battle involving Iran and the disruption to transport by means of the Strait of Hormuz. Outdoors of power, the month-to-month positive aspects had been comparatively muted. Shelter, which accounts for about one-third of the index, rose 0.3 % in Could and is up 3.4 % over the previous yr, whereas meals costs rose 0.2 % over the month and three.1 % over the yr.

Inside the core, the large strikes largely canceled out. Airline fares jumped 2.7 % in Could and are up 26.7 % over the previous yr, whereas motorized vehicle insurance coverage fell 1.7 % and is down 2.0 % from a yr in the past. With little motion elsewhere, core inflation slowed to 0.2 % even because the headline determine stayed elevated.

In brief, the classes excluded from core — power above all — pulled the general index up, whereas underlying value pressures eased.

The three-month development underscores how a lot of the latest acceleration is an power story. From March by means of Could, headline CPI averaged about 0.67 % per thirty days, equal to roughly an 8 % annual price — effectively above the 4.2 % year-over-year determine. However that tempo is nearly fully a product of the power spike. Strip out meals and power, and the image modifications sharply: core CPI rose 0.2 % in March, 0.4 % in April, and 0.2 % in Could, a median of roughly 0.27 % per thirty days, or a few 3.3 % annual price. That’s solely modestly above the two.9 % year-over-year core tempo, and effectively under what the headline development implies.

Though the Federal Reserve formally targets the private consumption expenditures value index (PCEPI), CPI information stay a well timed and related gauge for policymakers, for the reason that two measures usually observe each other intently. In line with the CME Group’s FedWatch device, markets are assigning a 98.4 % chance that the Fed will maintain charges regular at its assembly subsequent week.

The labor market information give policymakers no motive to ease within the face of that elevated inflation. Employers added 172,000 jobs in Could, and the unemployment price held at 4.3 %, the BLS reported final Friday. The Bureau additionally revised March and April payrolls up by a mixed 93,000, lifting April’s acquire to 179,000 from the 115,000 first reported. With labor-force progress held down by an getting older inhabitants and lowered immigration, the participation price regular at 61.8 %, and the employment-population ratio little modified at 59.2 %, the financial system seems to be close to full employment — a setting wherein even modest month-to-month job positive aspects now not sign a weakening financial system.

Taken collectively, the Could information level to one thing greater than a passing power shock. Above-target inflation that retains drifting larger, alongside a labor market close to full employment, is tough to sq. with the view that oil alone is in charge. Provide shocks change relative costs; they don’t, by themselves, push the general value stage up yr after yr. That requires extra nominal spending, which grew 5.9 % over the yr by means of the primary quarter — effectively above the roughly 4 % tempo that prevailed earlier than the pandemic. By that customary, the latest run of inflation seems much less like a brief disruption and extra like a financial phenomenon.

Governor Christopher Waller, a number one voice on the FOMC, made an identical case in a latest speech. With the labor market secure and inflation elevated, he stated he would drop the “easing bias” from the Fed’s coverage assertion and maintain the speed regular, warning that value pressures had been broadening past power — about half of client costs have risen 3 % or extra this yr, a traditionally giant share. He additionally famous that, with workforce progress close to zero, “little or no job creation is now in keeping with a secure labor market,” and he declined to rule out a price improve if inflation didn’t recede.

The Could CPI report, even with its softer core studying, matches that analysis. The one-month deceleration in core costs is welcome, however it doesn’t change the broader image: inflation stays above the Fed’s two-percent goal, and it’s being pushed by demand that’s nonetheless operating too sizzling. For now, the case for slicing charges is weak — and if nominal spending fails to sluggish, the tougher query dealing with the Fed might not be when to chop, however whether or not it should transfer within the different course.