{kind=link}

Persistent Techniques Ltd – Re(AI)magining the World

Included in 1990 and headquartered in Pune, Persistent Techniques Restricted is an AI-led, platform-driven digital engineering and enterprise modernization firm that companions with international enterprises throughout the software program growth and know-how transformation lifecycle. Its enterprise is organised throughout three {industry} verticals – Software program, Hello-Tech & Rising Industries; Banking, Monetary Companies & Insurance coverage (BFSI); and Healthcare & Life Sciences – and is anchored on three AI pillars: Engineering Hyper-Productiveness, Enterprise Hyper-Productiveness, and Enterprise Knowledge Readiness, underpinned by proprietary platforms SASVA, iAURA and GenAI Hub. Persistent serves 20 of the Fortune 50, together with 7 of the highest 10 know-how firms and 4 of the highest 5 banks in each the US and India, delivered by means of a 27,502-strong workforce unfold throughout North America, India, Europe and the remainder of the world. As of March 31, 2026, the corporate held a portfolio of 121 patents spanning AI infrastructure, knowledge intelligence and autonomous brokers.

Merchandise and Companies

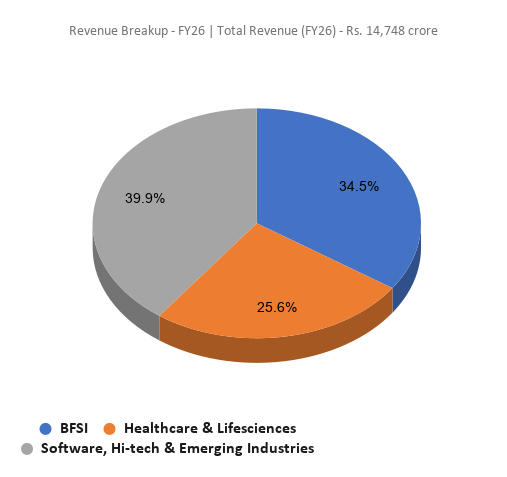

- Banking, Monetary Companies & Insurance coverage (BFSI) — The biggest and fastest-growing vertical, contributing 34.5% of Q4FY26 income (FY26: 34.6%), up from 31.6% in FY25. Persistent serves 4 of the highest 5 banks in each the US and India and prime 3 of the highest 5 fintechs. Service choices inside BFSI span core banking and insurance coverage platform modernization (together with COBOL-to-cloud migration), funds infrastructure (FedNow, real-time settlement), enterprise knowledge modernization for regulatory compliance (BASEL, AML, KYC, DORA), and agentic AI-led digital underwriting and price transformation.

- Healthcare & Life Sciences (HL&S) – Contributing 26.3% of Q4FY26 income (FY26: 25.6%), Persistent works with 2 of the highest 5 well being suppliers and payors, 3 of the highest 5 pharmaceutical firms, and 4 of the highest 5 scientific analysis organizations. Choices embody care administration platform engineering, scientific and analysis knowledge unification, AI-driven drug discovery (protein construction prediction, molecular simulation by way of NVIDIA BioNeMo), and cloud-native CRO platform transformation.

- Software program, Hello-Tech & Rising Industries – The biggest vertical by income at 39.2% of Q4FY26 (FY26: 39.8%), serving 7 of the highest 10 international know-how firms. This vertical anchors Persistent’s AI-led SDLC proposition – engineering hyper-productivity by way of SASVA – alongside product engineering, platform carve-outs, SAP providers, and software-to-cloud transformation for know-how and industrial firms.

Subsidiaries: As of FY26, the corporate has 21 subsidiaries and one managed ESOP belief.

Funding Rationale

- AI-led, platform pushed mannequin – Persistent’s defining characteristic is its capacity to place the GenAI/SDLC disruption as a web tailwind reasonably than a risk. The “Sixth Orbit” technique is anchored on three AI pillars — Engineering, Enterprise Hyper-Productiveness and Enterprise Knowledge Readiness — operationalised by means of proprietary platforms SASVA, iAURA and GenAI Hub, a 500+ agent portfolio, and 121 patents. Critically, SASVA runs as a model-agnostic native layer integrating Anthropic, OpenAI, Copilot and Gemini, letting Persistent monetise shopper instrument decisions reasonably than be disintermediated. Administration has guided a $2 billion income for FY27, with the June 2026 AI Investor Day serving as a near-term catalyst.

- Regular margin enlargement underpinned by working leverage and capital effectivity – Past progress, the standard of earnings is bettering. FY26 EBIT margin expanded 90bps YoY to fifteen.6% (EBIT +31.5%, PAT +33.2%), with administration reaffirming a 16-17% aspiration whereas explicitly prioritising progress and functionality funding over near-term margin seize. The corporate demonstrates disciplined execution: ROCE of 44.4% and ROE of 26.3% rank among the many greatest within the sector, whereas OCF/PAT strengthened to 94.7% in FY26 from 82.6% in FY25, indicating robust money conversion.

- Development unfold throughout many purchasers and a powerful deal pipeline – Persistent’s progress is broad-based reasonably than depending on a handful of accounts. Its banking and monetary providers (BFSI) vertical led the way in which in FY26 with 28.4% progress, supported by regular momentum in healthcare and know-how. The shopper base can also be deepening — the variety of purchasers producing over $5 million in annual enterprise rose from 55 to 62, and people above $1 million grew from 191 to 201 over the 12 months. The deal pipeline backs this up: complete contract worth (TCV, the price of all offers signed) reached about $2.4 billion for FY26, and headlined by a marquee new SAP providers deal price over $50 million. With its largest purchasers steadily increasing whereas general focus stays managed, the enterprise appears to be like well-diversified and resilient.

- Q4FY26 – In the course of the quarter, Persistent reported consolidated income of ₹4,055.9 crore, up 25.1% YoY, marking its twenty fourth consecutive quarter of progress. The upper rupee-terms progress was partly helped by a weaker rupee, with the common alternate fee at ₹93.0 per greenback versus ₹86.4 a 12 months earlier. Working revenue (EBIT) rose 30.5% YoY to ₹659.2 crore, with the EBIT margin bettering 70 foundation factors YoY to 16.3%. Web revenue grew 33.7% YoY to ₹529.3 crore translating to a web margin of 13.1%.

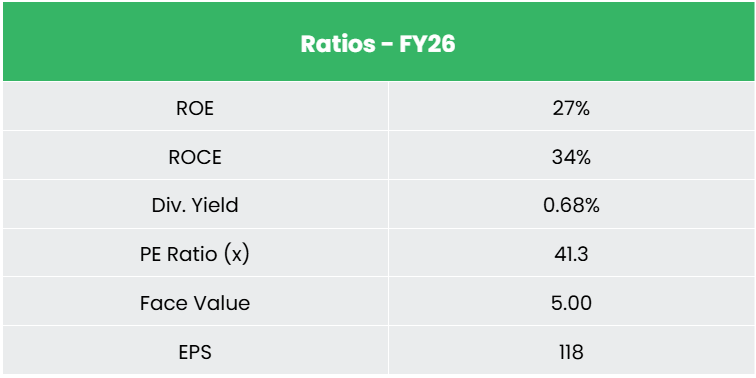

- FY26 – For the total 12 months, consolidated income stood at ₹14,748.4 crore, up 23.5% YoY in rupee phrases (17.4% in greenback phrases). Working revenue (EBIT) grew 31.5% YoY to ₹2,303.5 crore, with the EBIT margin increasing 90 foundation factors to fifteen.6% (together with a small ~0.6% one-time influence from the brand new labour codes). Web revenue rose 33.2% YoY to ₹1,865.1 crore, with the online margin at 12.6% and EPS at ₹119.7. The Board really helpful a last dividend of ₹18 per share, taking the entire FY26 dividend to ₹40 per share, up from ₹35 in FY25.

- Monetary Efficiency – The three-year income and web revenue CAGR stands at 21% and 28% respectively between FY24-26. The corporate has a debt-to-equity ratio of 0.06. The three-year common ROE and ROCE are round 25% and 31%.

Trade Overview

The Indian IT-BPM sector has emerged as a essential pillar of the economic system, with income estimated at ₹25,68,159 crores (US$297 billion) in FY25, rising at a CAGR of ~9.2% from ₹10,42,915 crores (US$167 billion) in FY18. Export income reached ₹20,14,751 crores (US$233 billion) in FY25, registering 16.5% progress from US$200 billion in FY24, with IT providers accounting for 66% of complete exports, adopted by Enterprise Course of Administration at 26% and Engineering R&D and software program merchandise at 8%. The sector instantly employs 5.8 million professionals, with India rating third globally amongst startup ecosystems with over 68,000 tech startups and bettering seven locations to thirty eighth within the 2024 International Innovation Index. The pc software program and {hardware} sector attracted cumulative FDI inflows of ₹8,31,772 crores (US$110.16 billion) between April 2000–June 2025, rating second in sectoral FDI and contributing 15.54% of complete cumulative FDI fairness inflows. India’s IT sector is on monitor to double income to ₹43,23,500 crores (US$500 billion) by 2030, pushed by AI adoption, cloud transformation, and enlargement of International Functionality Facilities anticipated to generate 22–25% of web new white-collar tech jobs.

Development Drivers

- AI and rising know-how proliferation

India’s AI market is projected to succeed in US$131.31 billion by 2032 at a CAGR of 42.2%, with AI anticipated to contribute US$957 billion to GDP by 2035, supported by the IndiaAI Mission’s ₹10,300 crores (US$1.19 billion) five-year allocation underpinned by deployment of 38,000 GPUs. - Cloud adoption and knowledge middle enlargement

India’s public cloud providers market is projected to succeed in US$13 billion by 2026 and US$17.8 billion by 2027, with knowledge middle capability anticipated to triple from ~870 MW in 2023 to 2,500 MW by 2027, driving the broader market to US$15 billion by 2030 on the again of 850 million+ web customers and 10 billion+ month-to-month UPI transactions. - Increasing International Functionality Facilities and geographic diversification

GCCs are anticipated to generate 1.2 million of the 4.7 million new tech jobs projected by 2027, with the GCC workforce projected to succeed in 3.46 million by 2030, whereas non-metro cities drove over 50% IT hiring progress in H1 2025 at ~30% price financial savings over metro options.

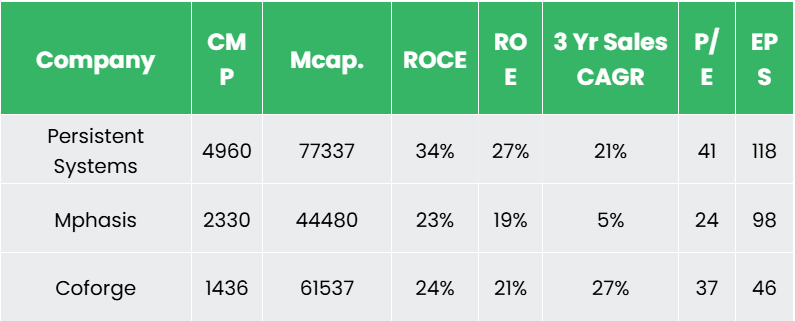

Peer Evaluation

Rivals: Mphasis Ltd, Coforge Ltd and so on.

The corporate boasts an {industry} main return profile, and demonstrates disciplined capital allocation and superior margins, whereas sustaining an unencumbered stability sheet.

Outlook

Persistent doesn’t present formal monetary steering, however administration’s commentary factors to continued wholesome progress in FY27. The corporate reaffirmed its goal of reaching a $2 billion annualised income run-rate – round ₹17,800 crore a 12 months by the tip of FY27, with healthcare & life sciences and BFSI to steer and run neck-and-neck in FY27, adopted by the know-how vertical – a modest shift from FY26, when BFSI was the clear standout. On profitability, it has reiterated an aspiration to function within the 16-17% EBIT margin vary, whereas making clear that income progress and continued funding in AI capabilities take precedence over near-term margin positive aspects. AI adoption is anticipated to speed up over the approaching quarters, led by know-how purchasers who undertake quickest, whereas regulated sectors like banking and healthcare transfer extra progressively from pilots to enterprise-wide rollouts, albeit, acknowledging that AI might compress some conventional software-development work, notably in know-how which is anticipated to be greater than offset by successful incremental market share.

Valuation

Persistent’s robust positioning within the AI adoption wave and properly diversified enterprise verticals place it to capitalize the AI pushed {industry} tailwinds. We suggest a BUY ranking on the inventory with a goal worth (TP) of Rs. 6,037, 37x FY28E EPS, an upside potential of ~20%. We additionally encourage sustaining a stop-loss at 20% from the entry worth to handle potential draw back threat successfully.

SWOT Evaluation

| Power | Weak spot |

|

|

| Alternatives | Threats |

|

|

Disclaimer: Investments within the securities market are topic to market dangers, learn all associated paperwork rigorously earlier than investing. Securities quoted listed below are exemplary, not recommendatory. Please seek the advice of your monetary advisor earlier than investing. Please word that we don’t assure any assured returns for the securities quoted right here.

Analysis disclaimer: Funding within the securities market is topic to market dangers. Learn all of the associated paperwork rigorously earlier than investing. Registration granted by SEBI, and certification from NISM by no means assure the efficiency of the middleman or present any assurance of returns to traders.

For extra particulars, please learn the disclaimer.

Different articles you could like

Put up Views:

331