{kind=link}

LIC has launched a brand new joint-life assured financial savings product referred to as LIC New Jeevan Sathi – Restricted Premium (Plan no 889) and is accessible for buy from 1 June 2026.

This can be a non-linked, non-participating, assured return joint-life insurance coverage plan the place a married particular person can purchase a single coverage overlaying each spouses.

It’s marketed as a novel joint-life conventional financial savings plan designed particularly for {couples} (“Two lives, One promise, Secured collectively”).

This publish takes a transparent, numbers-first take a look at the plan utilizing figures from the official brochure. It goes past the advertising and marketing to work out the precise IRR (Inside Charge of Return) and see whether or not it’s price including to your portfolio.

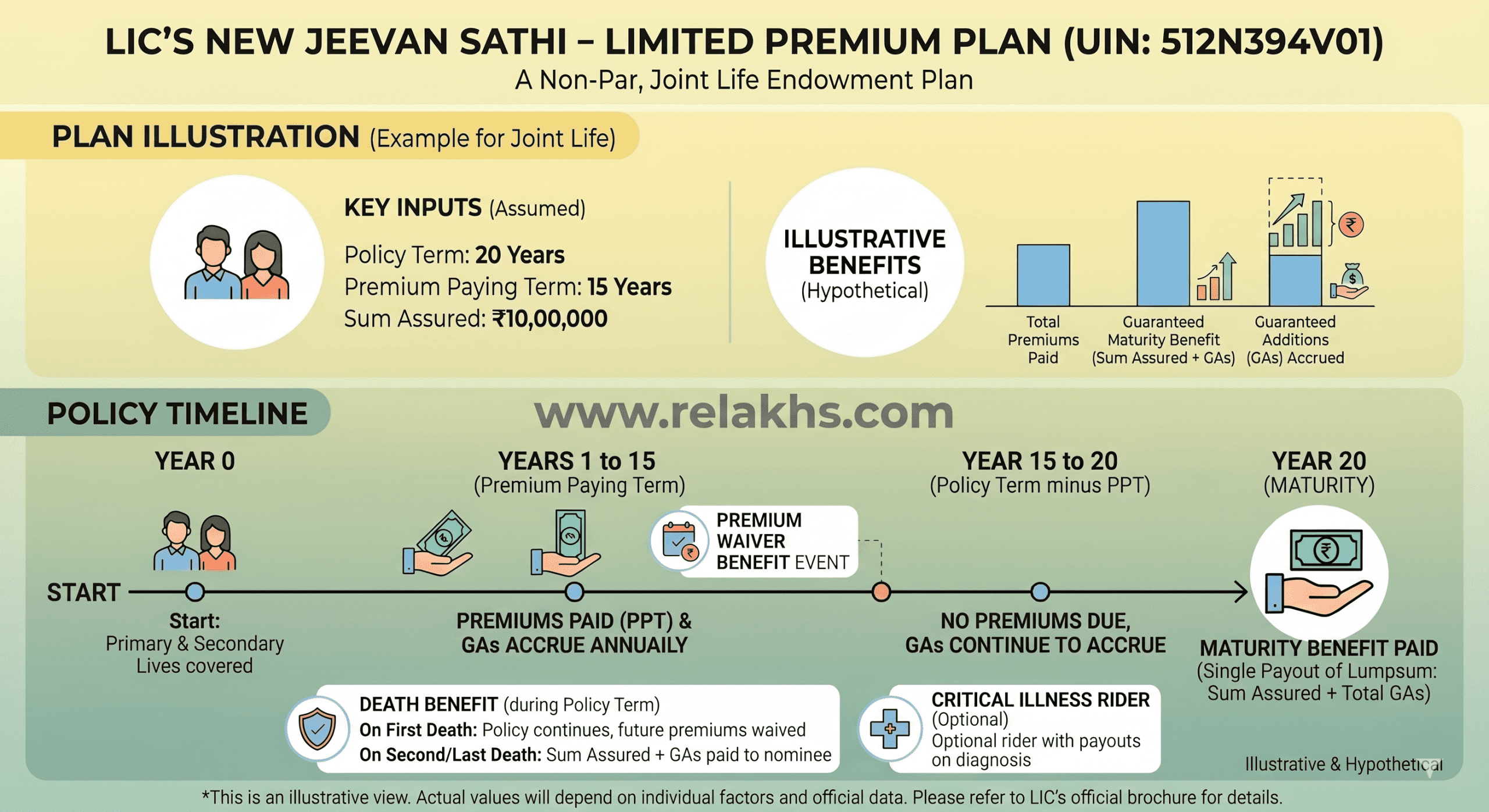

Key Options of LIC New Jeevan Sathi

This plan is a Non-Collaborating, Non-Linked, Joint Life, Restricted Premium Endowment Financial savings Plan.

- Joint Life Cowl: Each you and your partner are insured below a single coverage.

- Restricted Premium Cost Time period (PPT): You do not want to pay premiums for the whole period of the coverage. PPTs are restricted to choices like 5, 10, or 15 years for coverage phrases extending as much as 25 years.

- Assured Additions (GA): The brochure highlights a “Assured Addition of seven% on the full annual premium paid.” These accumulate yearly and are paid out on the finish of the time period.

- Premium Waiver on First Dying: If one partner passes away throughout the premium paying time period, all future premiums are fully waived. The surviving partner stays absolutely coated till the top of the coverage time period with out making additional funds.

- Maturity Payout: Paid out as a lump sum on the finish of the coverage time period if each or both of the lives survive.

LIC New Jeevan Sathi Coverage | The way it Works?

The official brochure gives two distinct pattern illustrations for a pair the place each people are 35 years outdated selecting a Primary Sum Assured of Rs. 10,00,000.

Possibility I: Longer Horizon (PT: 25 Years, PPT: 15 Years)

- Age of husband & spouse: 35 years

- Annual Base Premium: Rs. 83,650

- Coverage Time period: 25 years

- Premium Cost Interval (PPT): 15 Years

- Whole Premium Invested: Rs. 12,54,750

- Maturity Profit at 12 months 25: Rs. 27,61,669 (This contains the Rs. 10,00,000 Primary Sum Assured + Rs. 17,61,669 in gathered Assured Additions).

Possibility II: Shorter Horizon (PT: 20 Years, PPT: 10 Years)

- Age of husband & spouse: 35 years

- Annual Base Premium: Rs. 1,31,750

- Coverage Time period: 20 years

- Premium Cost Interval: 10 Years

- Whole Premium Invested: Rs. 13,17,500

- Maturity Profit at 12 months 20: Rs. 25,21,383 (This contains the Rs. 10,00,000 Primary Sum Assured + Rs. 15,21,383 in gathered Assured Additions).

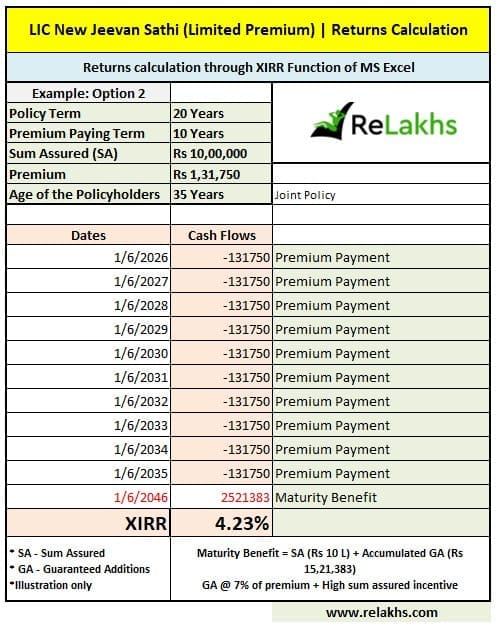

LIC New Jeevan Sathi Restricted Premium Plan – Actual Returns Defined

Whereas a headline of “7% Assured Additions” sounds engaging, it’s essential to acknowledge that this 7% is calculated on the annual premium paid, not compounded on the full gathered stability.

If we map out the precise year-by-year money flows and clear up for the Inside Charge of Return (IRR) utilizing monetary features (assuming survival of each companions), the online compounded returns are as follows:

| Parameter | Possibility I (25-Yr Time period) | Possibility II (20-Yr Time period) |

| Premium Paying Time period | 15 Years | 10 Years |

| Annual Outflow | Rs. 83,650 | Rs. 1,31,750 |

| Whole Outlay | Rs. 12,54,750 | Rs. 13,17,500 |

| Ultimate Lump Sum Return (Maturity Profit with Assured Additions) |

Rs. 27,61,669 | Rs. 25,21,383 |

| Web Compounded IRR | 4.38% | 4.23% |

Who can purchase LIC’s New Jeevan Sathi coverage?

This coverage might swimsuit:

- Extraordinarily conservative buyers: Individuals who dislike market-linked merchandise, need assured maturity, and really feel extra snug with the LIC model.

- {Couples} searching for easy property planning: A single coverage for each spouses could make nomination, liquidity planning, and household safety a bit simpler.

- Individuals who need compelled long-term financial savings: As a result of early give up penalties apply, some buyers use it as a disciplined financial savings software.

Why you ought to be cautious earlier than shopping for a joint coverage?

Joint-life insurance policies might sound engaging, however they arrive with a number of sensible drawbacks. Husband and spouse typically have completely different incomes, liabilities, and retirement objectives, so one mixed coverage might not match each wants properly. It additionally reduces flexibility, since separate insurance policies are simpler to cease, change, or change in case your scenario adjustments.

One other problem is exit planning. If priorities shift, a separation occurs, or one partner now not wants cowl, a joint coverage can change into more durable to handle. Many consumers additionally focus solely on the maturity worth and assured returns, whereas overlooking give up worth, alternative value, and the influence of inflation.

Why LIC New Jeevan Sathi Restricted Premium might not attraction to everybody

The larger concern is returns. An IRR of round 4 to five % over 20–25 years might battle to maintain up with inflation. The coverage additionally wants a protracted dedication and common premium funds earlier than it delivers significant worth.

- Sub-inflation returns: An IRR of 4.2% to 4.4% is kind of low for a 20–25 12 months horizon. Since long-term retail inflation is often round 5% to eight%, returns beneath 5% can slowly erode your buying energy over time.

- Low insurance coverage cowl: For an annual premium of Rs. 1.31 lakh below Possibility II, the life cowl is barely Rs. 10 lakh. For a main earner, that quantity will not be sufficient to assist the household, repay money owed, or fund kids’s larger schooling.

- Poor liquidity: In the event you face a money crunch and must exit early, surrendering a standard coverage might be painful. Within the early years, chances are you’ll lose a big a part of the premiums you paid.

What Concerning the Single Premium Model of New Jeevan Sathi?

LIC has additionally launched a Single Premium model of New Jeevan Sathi for buyers preferring one-time funding as a substitute of paying yearly premiums.

LIC New Jeevan Sathi – Single Premium Illustration:

- Age : 35

- Single Premium Outflow (Base): ₹8,12,750

- Primary Sum Assured: ₹10,00,000

- Assured Addition (GA) Charge: ₹70 per ₹1,000 Sum Assured every year (Mounted ₹70,000 accrued yearly)

- Coverage Time period: 20 Years

- Maturity Payout: ₹24,00,000 (₹10 Lakh Sum Assured + ₹14 Lakh gathered GA)

The anticipated IRR on single premium model is round 5.56%.

At 5.56%, the Single Premium possibility generates a structurally higher yield than the Restricted Premium variant (4.23%). It is because your complete funding quantity will get the total 20 years to expertise the mounted compounding impact, somewhat than trickling into the plan year-by-year.

The Single Premium variant might swimsuit buyers who’ve surplus lump sum cash and need a one-time assured product with out future premium commitments. The Restricted Premium model reduces upfront burden by spreading funds over a number of years. Nevertheless, in each variations, buyers ought to concentrate on precise returns, liquidity and long-term alternative value earlier than investing.

Higher options to think about

Relying in your aim, there are sometimes higher choices than a joint conventional coverage.

Purchase separate time period insurance coverage insurance policies. Every partner can take sufficient cowl on their very own, which often offers decrease value, larger protection, and extra flexibility. As an alternative of placing Rs. 1,31,750 a 12 months into LIC New Jeevan Sathi, you might use the identical price range rather more effectively.

Step 1: Safety:

Purchase two separate pure time period insurance policy (if wanted), one for every partner. A Rs. 1 crore cowl for a 35-year-old often prices round Rs. 12,000–15,000 a 12 months, so each spouses might get robust protection for roughly Rs. 25,000–30,000 a 12 months. That provides you round 10 occasions extra insurance coverage safety.

Step 2: Financial savings and funding:

Use the remaining Rs. 1 lakh+ for higher wealth-building choices.

- For assured returns: Think about PPF, VPF, or long-term NSC.

- For long-term wealth creation: Put money into diversified fairness mutual funds by SIPs. Over 20–25 years, even a 10%–11% CAGR can construct a a lot bigger corpus than a standard endowment plan.

The important thing thought is easy: separate safety from investing. That often offers you extra cowl, extra flexibility, and higher long-term progress.

Ultimate Ideas:

LIC New Jeevan Sathi is a conservative joint-life insurance coverage plan for households preferring assured returns over excessive progress. Whereas it provides simplicity and predictable advantages, it’s basically one other low-yield conventional financial savings plan packaged with a “single coverage for husband and spouse” idea, which is more likely to be aggressively marketed. Earlier than investing, evaluate it fastidiously with time period insurance coverage plus separate funding choices.

Proceed studying:

(Please notice that this text is predicated on the restricted out there data and will probably be edited/up to date, if required)

(Submit first revealed on : 128-Might-2026)