{kind=link}

An essential (albeit time-consuming) a part of operating an RIA is fulfilling the compliance obligations required by the agency’s regulator(s). Presently, companies with at the very least $100M of regulatory Belongings Below Administration (AUM) or that might be required to register with at the very least 15 states sometimes should register with and be overseen by the Securities and Trade Fee (SEC), whereas different (smaller) companies are regulated by their residence state, plus typically any extra state(s) wherein they’ve at the very least 5 purchasers. Nevertheless, the proportion of RIAs assembly the edge for SEC registration has steadily elevated through the years, owing to each the general progress of the RIA mannequin, and the event of expertise permitting RIAs to scale up quicker (whilst they continue to be comparatively “small” companies, with even most SEC-registered RIAs using solely a handful of workforce members and managing ‘simply’ a couple of hundred million in belongings, each of which pale compared to the small variety of mega-RIAs and asset managers that dominate many of the business’s AUM).

Amid this backdrop, the SEC is contemplating a pair of adjustments that might change the regulatory panorama for a lot of RIAs.

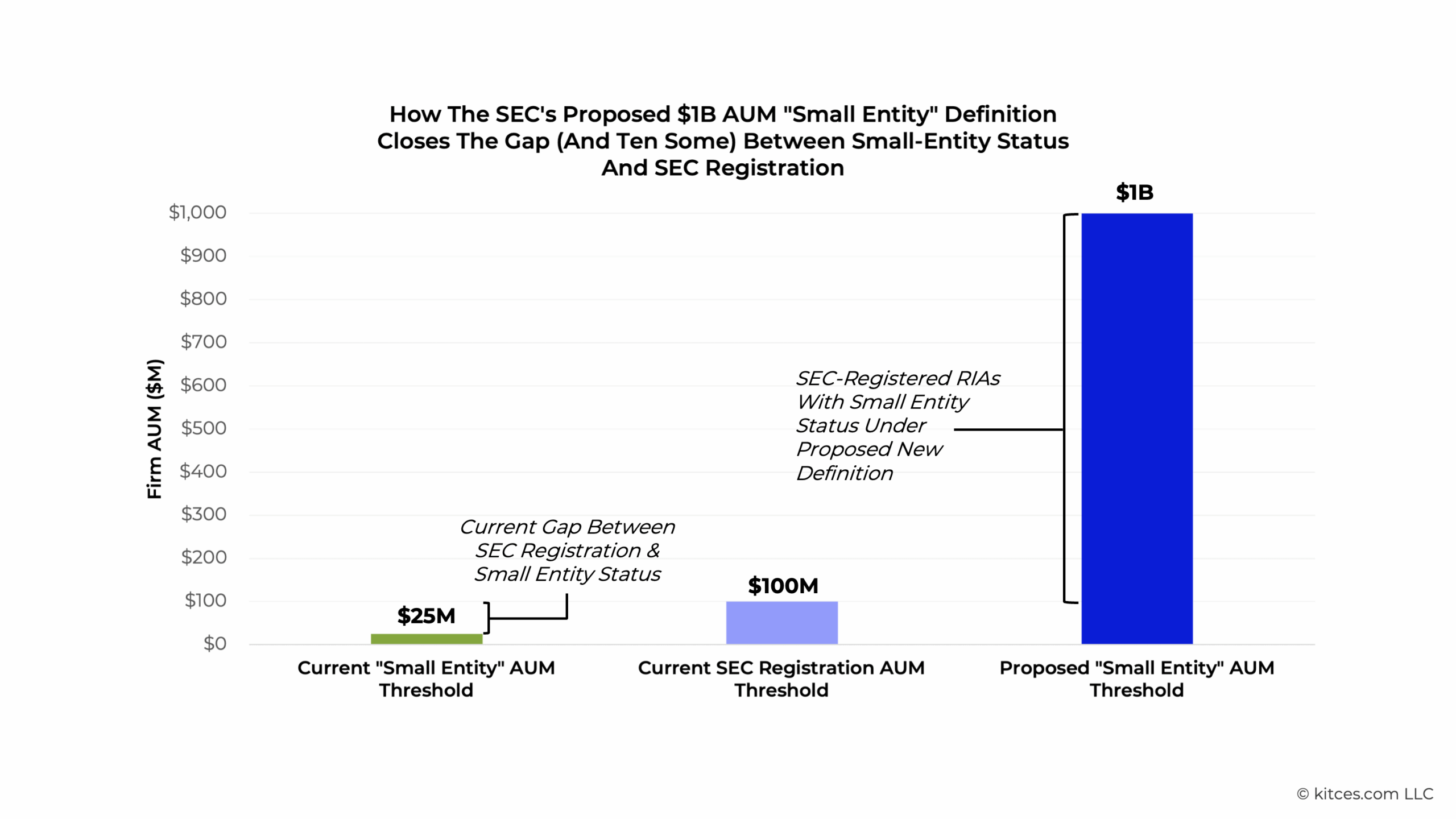

First, the SEC has issued a proposed modification that might change the definition of a “small entity” RIA for functions of the Regulatory Flexibility Act of 1980 (which is designed to forestall guidelines and laws from creating an undue regulatory burden on small companies) from $25M of AUM to $1B of AUM (whereas additionally contemplating utilizing a revenue- or worker headcount-based threshold in lieu of an AUM-based threshold). A brand new threshold of $1B of AUM would enhance the variety of SEC-registered RIAs that qualify as “small entities” from simply 3% in the present day as much as 75% (although these 75% would nonetheless solely account for 3% of all RIA-managed belongings given the focus of belongings in a couple of mega-firms!). And so if the proposed modification is adopted (as seems probably, given pretty broad assist expressed throughout the proposal’s remark interval), the tempo of SEC rulemaking would probably decelerate because it must extra fastidiously take into account and weigh the potential impression of proposed new guidelines on a drastically elevated variety of “small entities” it oversees – probably offering a stage of future regulatory reduction for comparatively smaller RIAs who haven’t got the income to assist hiring devoted compliance employees to deal with elevated regulatory obligations.

A separate (and never but formally proposed) change that was however hinted at by Performing SEC Commissioner Mark Uyeda in public feedback final yr would additionally enhance the regulatory AUM threshold for companies to register with the SEC from the present $100M to maybe $1B, which might have the results of shifting hundreds of at the moment SEC-registered companies (again) to state registration (probably with many companies needing to register in a number of states given the broader geographic distribution of purchasers for many companies, particularly within the post-COVID virtual-meeting period). Whereas such a change would cut back the variety of RIAs underneath SEC oversight (probably permitting it to deal with the biggest RIAs representing the best systemic threat for shoppers, and higher aligning the variety of companies the SEC should oversee with its Congressionally-limited price range), it may additionally considerably enhance the compliance burden on many RIAs that might be compelled to grapple with the complexity of multi-state registration, significantly when these states’ legal guidelines and laws do not totally line up with one another. Which may trigger bigger state-registered companies to flock to affiliate with SEC-registered company RIA platforms that would take sure compliance obligations off of their plates (or just render them eligible for Federal reasonably than state registration), opting to sacrifice a few of their independence to stay SEC-registered reasonably than battle with elevated compliance burdens underneath state registration.

In the end, the important thing level is that within the 15+ years for the reason that SEC final up to date its registration threshold (and almost 30 years for the reason that “small entity” threshold’s final replace), there have been sufficient adjustments within the RIA panorama – each by way of common agency measurement and the variety of states wherein companies do enterprise within the digital assembly and area of interest consumer advertising and marketing period – that it is sensible to rethink tips on how to divide between state and SEC registration. As a result of satirically, whereas most RIAs actually are “small” companies that in mixture comprise solely a small fraction of business AUM, it is maybe these companies (with much less capability for dealing with compliance burdens) that might profit most from following a single uniform SEC normal reasonably than a maze of often-conflicting state-level laws, in addition to from slower tempo of rulemaking that might probably consequence from the proposed increased “small entity” AUM threshold. So if the SEC does ultimately find yourself elevating its registration threshold, we might count on to see a much bigger push for states to additional standardize their securities laws to scale back the compliance burden on state-registered companies – or else see a flood of small- and mid-sized advisory companies affiliate with company RIAs to keep away from state-level regulation altogether!