{kind=link}

The revenue and wealth inequality that continues to develop in most superior nations has led to some new terminology being launched into the lexicon of financial phrases, the – Ok-shaped financial system: When progress strikes in two totally different instructions. When this sample of progress is recognized you understand how far out of kilter the world has grow to be. Basically, for most individuals, occasions are so robust that even important items and providers grow to be so costly that even non-discretionary spending begins to take a success. But, for the top-end-of-town, with the excessive wealth and excessive incomes, who’re boosted by rising central financial institution rates of interest and rising asset costs (monetary and actual property and so on), their spending goes loopy because the Porsches roll out the showroom door at an growing charge. The Ok-pattern pertains to the much less well-off heading south and the wealthy and excessive revenue cohorts heading north by way of prosperity and capability to devour. The most recent knowledge from the US, which exemplifies this development greater than most international locations, given its large inequality, clearly demonstrates this phenomenon.

Newest US Nationwide Accounts knowledge – March-quarter 2026

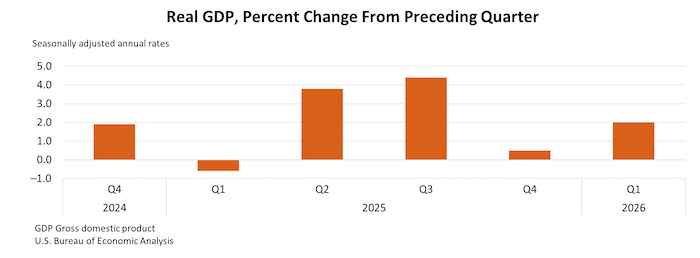

Final Thursday (April 30, 2026), the US Bureau of Financial Evaluation launched the – GDP (Advance Estimate), 1st Quarter 2026 – which reported that progress within the US was working at 2 per cent every year, up from 0.5 per cent within the December-quarter 2025.

The BEA revealed this graph to seize the annual GDP progress over the past a number of quarters:

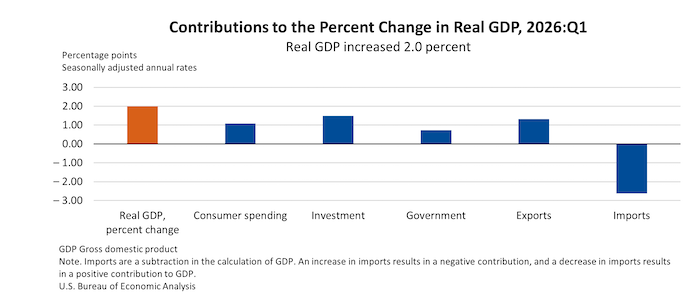

Additionally they revealed this graph, exhibiting the totally different contributions made to that progress final result from the foremost combination spending classes.

They famous that “The contributors to the rise in actual GDP within the first quarter had been funding, exports, shopper spending, and authorities spending. Imports, that are a subtraction within the calculation of GDP, additionally elevated.”

The contributions had been:

1. Private consumption expenditure 1.08 factors.

2. Gross non-public home funding 1.48 factors.

3. Authorities consumption expenditures and gross funding 0.73 factors.

4. Web exports -1.3 factors

5. Whole GDP progress 2 per cent.

So consumption expenditure accounted for simply over 50 per cent of the general final result, whereas home funding was almost 75 per cent of the overall progress.

Web exports had been a drain on progress, and that tells you that Trump’s hoped for transformation of the US into an export machine will not be working.

Nevertheless, on the face of it, these figures inform us nothing a lot concerning the presence of a Ok-shaped financial system.

They inform us that private consumption expenditure stays robust regardless of the rising prices and really modest progress in actual wages.

They inform us that home funding is booming.

If we dig somewhat deeper into the spending aggregates, the image turns into somewhat clearer.

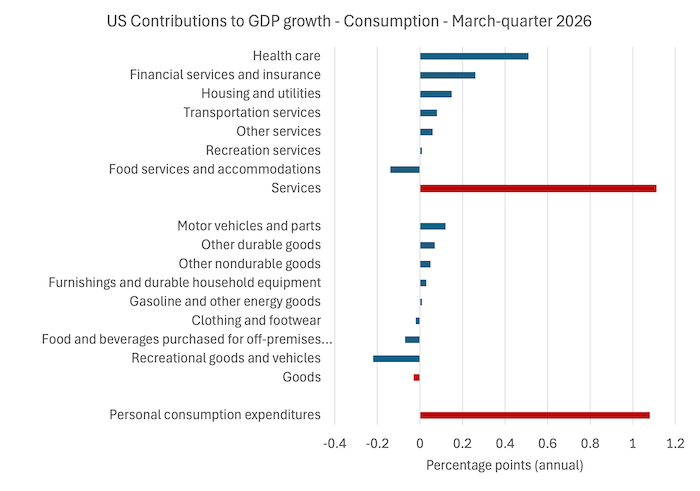

The primary graph exhibits the contributions to actual GDP progress within the March-quarter from the consumption spending parts.

The crimson bars are the combination and most important sub-aggregate totals (Items and Companies).

I sorted inside these sub-totals from strongest contributor to weakest.

For items (general destructive contributor) it’s expenditure on Motor Autos that dominate.

For providers, Well being care and FIRE dominate whereas meals and lodging had been destructive contributors.

Some additional digging discovered that – New automobiles are more and more turning into a luxurious amid Ok-shaped financial system considerations.

The truth is:

The share of new-car consumers with incomes of lower than $100,000 has dropped from 50% in 2020 to 37% final 12 months, whereas the share of consumers with incomes of greater than $200,000 has grown from 18% to 29% throughout that timeframe …

Porsches going out of showrooms!

The Boston Consulting Group launched a report on December 12, 2025 – Automotive Trade Past the Drive: The Way forward for the Luxurious Automotive Ecosystem – forecast that “the US whole addressable marketplace for automobiles priced at or above $100,000 is projected to rise by a compound annual progress charge of 5% to 7% by means of 2035”.

And “a big proportion of consumers throughout all age teams favored a few anchor manufacturers (notably Porsche and Ferrari) …”

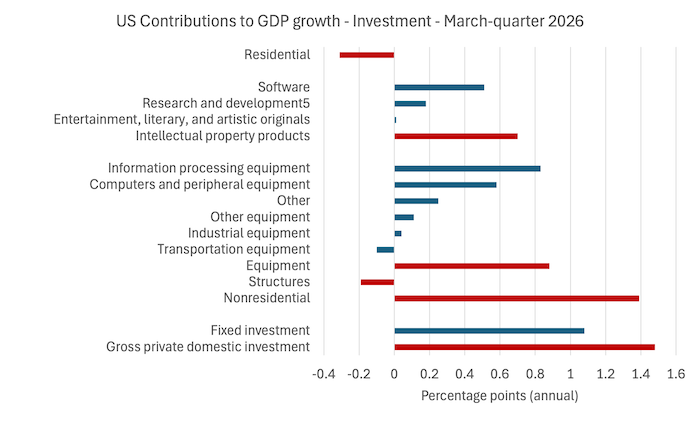

By way of funding expenditure progress, the strongest contributors are gear, particularly, Computer systems and peripheral gear (0.58 factors) and Data processing gear (0.83 factors), and in mental property merchandise, software program (0.51 factors).

What does that each one imply?

The private consumption sample is being dominated by robust expenditure by high-income households, which have reaped massive revenue boosts because of rising rates of interest and the share market progress.

In the meantime, the funding increase is being pushed by large funding by the big expertise companies in AI.

How that each one seems is anybody’s guess, however I predict that we’re approaching a particular type of Marxian realisation disaster the place AI undermines mainstream employment, notably among the many graduate positions (for instance, pc coding, methods evaluation, accounting, and so on) and makes corporations extra able to pumping out items and providers.

The query that’s staring us within the face is who’s going to purchase the stuff when unemployment rises and revenue progress will get concentrated to the top-end of the distribution.

There are solely so many luxurious automobiles that one should buy.

Newest Ok-economy analysis

What seems to be occurring within the US in the meanwhile is the expertise corporations are spending as if there isn’t a tomorrow and their wealth homeowners are shopping for a number of consumption objects with the largesse that the AI increase is offering through the share market.

That is the place Capitalism has reached.

And it’s extremely unstable.

The most recent analysis from the New York Federal Reserve Financial institution (revealed Might 1, 2026) –

Explaining the Ok‑Formed Economic system: What’s Behind the Divide? – considers the newest Nationwide Accounts knowledge:

… is per the favored press’s concept of a “Ok-shaped financial system” by which higher-income households expertise quicker progress in spending than lower-income households.

The general discovering is that:

We discover that, since 2023, wealth has elevated essentially the most for high-income households, whereas inflation has risen essentially the most for low-income households, with each elements serving to clarify the truth that actual retail spending rose essentially the most for high-income households. In distinction, earnings show a extra combined sample, although earnings of the very best earners have grown extra quickly than earnings of the bottom earners.

Their evaluation of spending patterns finds that:

1. “actual spending on luxuries elevated cumulatively since 2023 for all three revenue teams and spending on requirements declined for many teams.”

2. Notably, the expansion in retail spending has been pushed by the expansion in luxurious spending.”

3. “We additionally see that progress of each necessity and luxurious spending by revenue group displayed the identical Ok‑formed sample as seen in whole retail spending.”

Why has a divergence in consumption expenditure throughout the revenue teams occurred?

The New York Federal Reserve Financial institution researchers discover that;

1. “… though the bottom wage quartile has skilled the bottom wage progress prior to now 12 months, we see that this has not at all times been the case. The truth is, in some intervals of 2023 and 2024, this group skilled the very best progress out of all of the quartiles. On condition that the Ok-shaped spending progress appeared in late 2023 and has endured since, we propose that there are different elements apart from wages that will clarify the Ok-shaped spending sample beginning in late 2023.”

2. Have been there differential inflation impacts throughout the revenue teams? The analysis means that “starting in late 2022, low-income households persistently confronted greater inflation than middle- and high-income households did.”

The upper inflation impression on the backside of the revenue distribution has been “restraining their spending” whereas on the high, the impression of inflation is “beneath or close to the nationwide common”.

Shifts within the wealth distribution have additionally been vital.

The researchers discovered that:

… there have additionally been Ok-shaped progress patterns in family wealth … since 2023, with greater revenue teams experiencing greater cumulative wealth progress, relative to the primary quarter of 2023, than decrease revenue teams in almost each quarter …

Thus, actual web price of the highest percentile grew by greater than 25 p.c, whereas that of the center 40 p.c grew by lower than 10 p.c. This progress in web price has been pushed by massive will increase in monetary property for higher-income teams and particularly the highest percentile … Given these wealth patterns, it isn’t shocking that greater revenue teams additionally elevated their retail spending by greater than decrease revenue teams.

The general conclusion is that Ok-shaped patterns throughout wages progress, impression of inflation, and wealth shifts have emerged within the US since 2023 and are influencing the composition and extent of GDP progress.

Implications

First, like all speculative and big funding booms, this one has the potential to go bust as some AI companies discover they can’t realise the investments.

It’s a frenzy at current however a shakeout is coming and the place that lands is tough to guess – apart from nowhere good.

Second, the folly by Trump and the Israelis appears to be ongoing and can additional pressure power markets.

I’ll write about what this implies for central banks in one other weblog submit, however the coverage making house has grow to be so ideologically concentrated that governments assume that rate of interest changes (upwards) are the one technique to cope with the inflationary pressures.

Attempting to cope with a provide shock with rate of interest will increase will dramatically fail (once more) and can solely drive the Ok-shaped sample additional till the highest of the Ok can now not offset the underside arm and the consequence might be recession.

Larger inflation (and rates of interest) may also make it tougher for the AI investments to ship desired returns, which is able to then reverse the share market positive aspects to some extent.

So the inflationary pressures will proceed to dampen shopper expenditure on the backside of the revenue distribution, however the wealth shifts from inflation might ultimately additionally impression negatively on the consumption expenditure on the high.

And it’s the latter that’s driving GDP progress within the US.

Conclusion

The system can not produce steady progress beneath these circumstances.

And the long-term prospects are unsound.

Hopefully, it blows earlier than November and the Republicans are broken because of this.

That’s sufficient for as we speak!

(c) Copyright 2026 William Mitchell. All Rights Reserved.