{kind=link}

Retirement planning in India is usually misunderstood. Many individuals suppose any long-term financial savings or funding plan can provide them a pension, however that’s not true. Just a few choices are literally designed to offer you a daily earnings after retirement.

That distinction issues as a result of retirement isn’t just about constructing a corpus. It’s about ensuring cash retains coming in even after your lively earnings stops.

In India, true pension choices are restricted. There are various financial savings and funding merchandise, however solely a handful actually qualify as pure pension schemes—those who flip your contributions right into a month-to-month earnings throughout retirement. A few of these are obligatory relying in your job, whereas others are voluntary and wish you to decide in.

On this article, let’s break down the 5 essential pension schemes in India—

- Staff’ Pension Scheme (EPS)

- Nationwide Pension System (NPS)

- Atal Pension Yojana (APY)

- Insurance coverage-based pension plans and

- Superannuation schemes.

We’ll maintain it easy and canopy their options, eligibility, lock-in guidelines, and professionals and cons so you may see which of them truly suit your retirement plan.

Pension Oriented Schemes in India – Full Information

Planning for retirement is now not nearly “saving”; it’s about selecting the best car to fight inflation and guarantee a gradual earnings. Here’s a breakdown of the highest 5 pension-related schemes in India

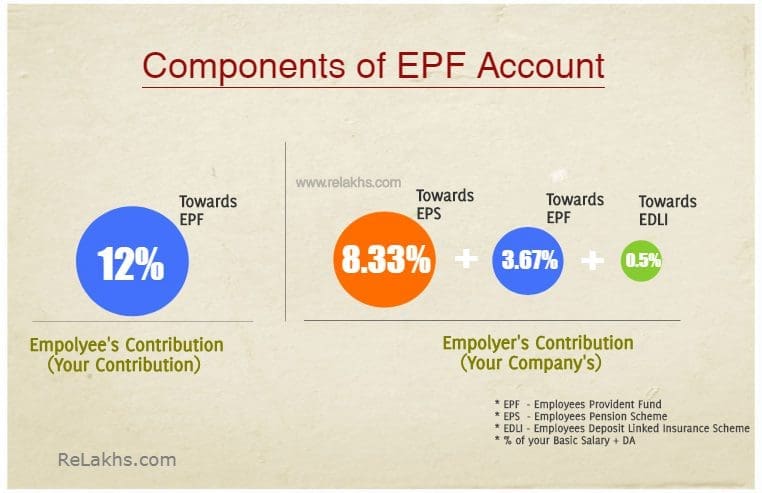

1) Staff’ Pension Scheme (EPS)

Managed by the EPFO, this can be a social safety scheme for organized sector workers.

- Who can subscribe: Any worker who’s a member of EPF.

- Key function: 8.33% of the employer’s contribution goes into this pension fund.

- Eligibility: At the very least 10 years of service and age 58.

- Lock-in / Exit: Locked until retirement, although early pension can begin from age 50 with a lowered payout.

- 2026 replace on withdrawal: The pension half can now be withdrawn solely after 36 months of leaving the job, as a substitute of two months.

- Additionally, a minimum of 25% of your PF stability should keep untouched till retirement so you retain a primary pension base.

Professionals: Assured lifelong pension, plus survivor advantages for partner and kids.

Cons: Returns are fastened and formula-based, so normally decrease than market-linked schemes. It’s obligatory for workers incomes as much as ₹15,000 primary wage.

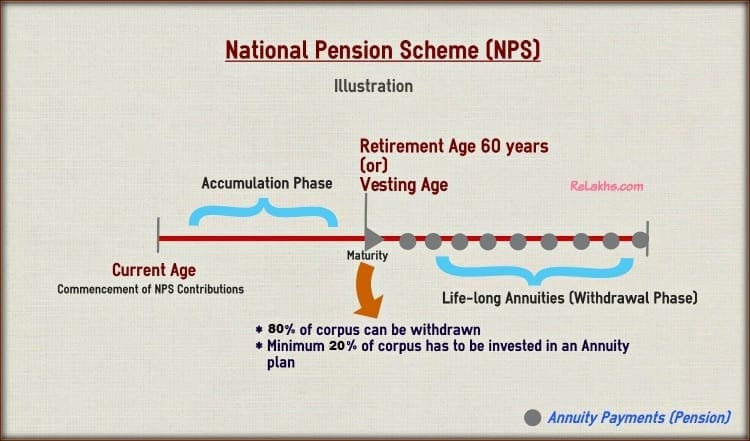

2. Nationwide Pension System (NPS)

A market-linked, voluntary retirement scheme regulated by the PFRDA. It’s broadly thought-about probably the most versatile pension software in 2026.

- Who can subscribe: All Indian residents (together with NRIs and OCIs) aged 18–85.

- Key Options: Alternative of funding (Fairness, Company Bonds, Authorities Bonds). Consists of NPS Vatsalya for minors.

- 2026 Replace – Withdrawal Guidelines:

- Maturity (Age 60): Now you can withdraw as much as 80% as a tax-free lump sum (elevated from 60%). The remaining 20% should be used for an annuity.

- Full Exit: If the whole corpus is ≤ ₹8 Lakh, you may withdraw 100% with out shopping for an annuity.

- Untimely: Partial withdrawals (as much as 25% of personal contributions) allowed for particular causes (training, sickness) after 3 years.

Professionals: Excessive return potential; additional tax deduction of ₹50,000 (Sec 80CCD(1B)); lowest administration charges globally.

Cons: Market-linked (returns aren’t assured); annuity earnings is taxable.

Necessary Be aware: Not like conventional pension schemes, NPS itself doesn’t assure a pension. It builds a retirement corpus, and you have to convert a portion of it into an annuity to generate month-to-month earnings. You must purchase an annuity plan from a life insurer. The standard of your pension underneath NPS relies upon not simply in your corpus, but additionally on the annuity charges accessible at retirement.

Replace: Unified Pension Scheme (UPS)

The federal government has launched the Unified Pension Scheme (UPS) for central authorities workers in its place framework alongside NPS. Not like NPS, which is market-linked, UPS goals to offer a extra predictable pension construction (Assured pension + contribution-based construction). Nevertheless, this scheme is at the moment restricted to authorities workers and isn’t accessible for most of the people.

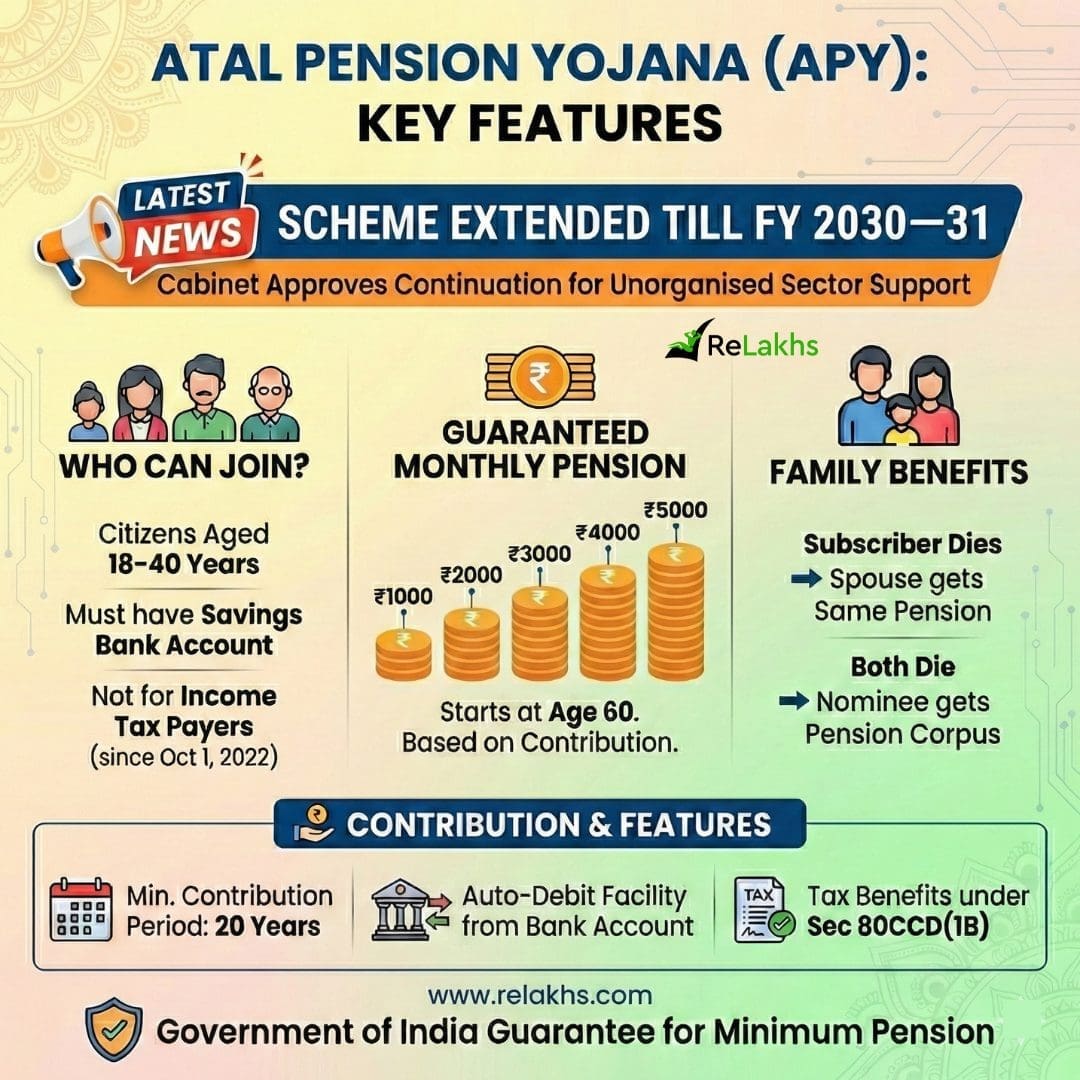

3. Atal Pension Yojana (APY)

Authorities-backed scheme primarily for unorganized sector employees, guaranteeing a minimal pension.

- Who can be part of: Indian residents aged 18–40.

- Be aware: Earnings tax payers can’t be part of since 2022.

- Key options: Fastened pension choices—₹1,000, ₹2,000, ₹3,000, ₹4,000, or ₹5,000 month-to-month.

- Withdrawal guidelines:

- Maturity: Auto-starts at age 60

- Untimely: Not allowed (besides terminal sickness or loss of life)

Professionals: Govt assure + triple profit (you → partner → corpus to nominee). Appropriate for low-income people

Cons: Entry capped at 40 years; fastened pension gained’t beat excessive inflation.

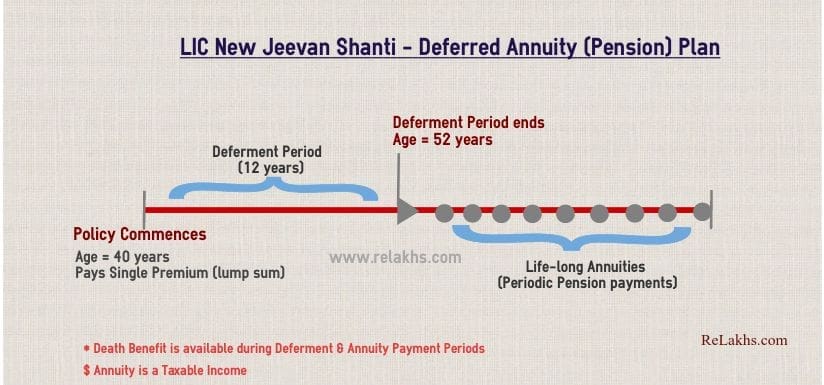

4. Life Insurance coverage Pension Schemes

Personal/Public insurance coverage firms (like LIC, SBI Life) provide “Annuity” or “Retirement” plans.

- Who can subscribe: Anybody (sometimes entry age 18–70).

- Eligibility: Based mostly on the particular coverage’s well being and age standards.

- Key Options: Two phases—Accumulation (paying premiums) and Vesting (receiving pension/annuities).

- Kinds of Annuities:

- Deferred annuity: Construct corpus first (accumulation part), then convert to pension later.

- Speedy annuity: Pension begins straight away after one-time funding.

- Withdrawal Guidelines:

- Lock-in: Usually 3–5 years.

- Maturity: Normally, 60% could be taken as a lump sum (tax-free guidelines apply per Part 10(10D)), and 40% is annuitized.

Professionals: Fastened, assured earnings choices (conventional plans); loss of life profit (life cowl) usually bundled.

Cons: Excessive give up costs if exited early; decrease returns in comparison with NPS.

5. Superannuation (Tremendous Annuity)

Employer-sponsored pension scheme managed by way of accepted superannuation funds. It’s a company pension program the place the employer contributes to a fund for the worker’s retirement.

- Who can be part of: Staff of firms providing superannuation advantages.

- Key options: Employer contributes as much as 15% of primary wage (outlined contribution or profit).

- Withdrawal guidelines:

- Retirement: Withdraw 1/third (33.3%) tax-free lump sum. Remaining 2/third → should purchase annuity. (Much like NPS construction)

- Job change: Switch to new employer’s fund or maintain till retirement or Withdraw (tax implications).

Professionals: Massive corpus from employer cash + tax-free contribution as much as ₹1.5 lakh.

Cons: Just for company workers; inflexible 1/third withdrawal rule.

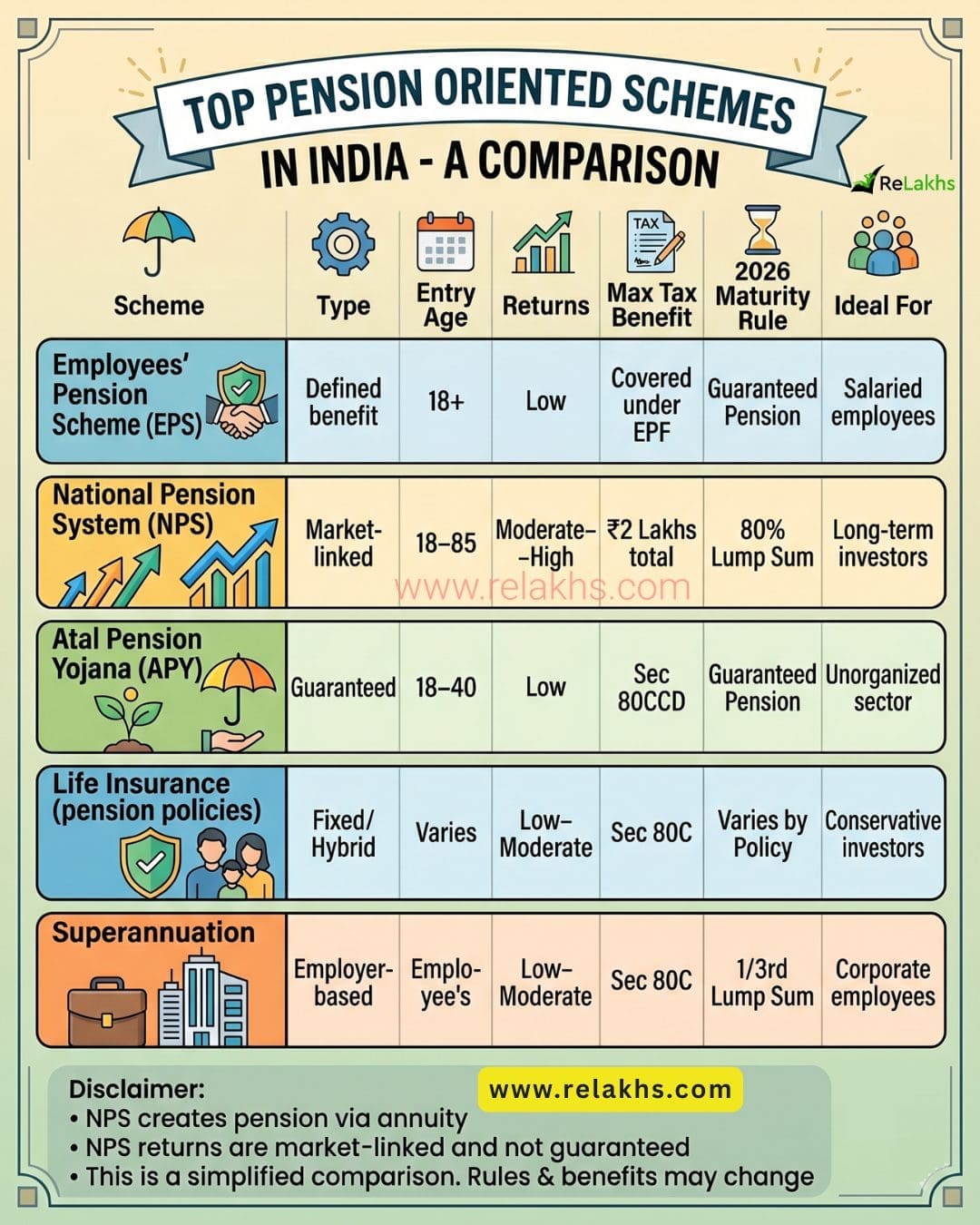

Pension Schemes – Fast Comparability Desk

| Scheme | Sort | Entry Age | Returns | Max Tax Profit | 2026 Maturity Rule | Superb For |

|---|---|---|---|---|---|---|

| EPS | Outlined profit | 18+ | Low | Coated underneath EPF | Assured Pension | Salaried workers |

| NPS | Market-linked | 18–85 | Reasonable–Excessive | ₹2 Lakhs complete | 80% Lump Sum | Lengthy-term buyers |

| APY | Assured | 18–40 | Low | Sec 80CCD | Assured Pension | Unorganized sector |

| Life Insurance coverage | Fastened/Hybrid | Varies | Low–Reasonable | Sec 80C | Varies by Coverage | Conservative buyers |

| Superannuation | Employer-based | Worker | Low–Reasonable | Sec 80C | 1/third Lump Sum | Company workers |

Different Pension-like Earnings Choices

Not Precisely Pension Schemes… However Helpful for Retirement Earnings

These aren’t true pensions (no assured lifelong payout), however they will create regular retirement money movement:

- PPF: Tax-free, protected, however 15-year lock-in (extensions attainable).

- SCSS: 5%+ curiosity for seniors (60+), 5-year tenure.

- Publish Workplace MIS: 7%+ month-to-month curiosity, low-risk.

- Mutual Fund SWP: Versatile withdrawals from fairness/debt funds (market-linked).

Key distinction: Pensions pay for all times. These have fastened tenures or versatile withdrawals.

“Whereas the above should not pure pension schemes, they play an important position in retirement planning. In actuality, a mix of pension schemes like NPS together with earnings choices like SCSS or SWP can create a secure and inflation-beating retirement earnings.”

Closing Ideas

No single scheme can deal with your complete retirement. A stable retirement plan is all the time a mix of progress, security, and earnings methods.

Probably the most sensible method for Indian buyers is to mix:

- NPS for long-term, market-linked progress

- EPF/PPF for stability and tax effectivity

- SCSS (post-retirement) for regular earnings

When it comes particularly to pure pension oriented schemes, every serves a distinct function:

- For progress & flexibility: NPS stands out in 2026 attributable to its low value and market-linked returns

- For security & assured earnings: APY and EPS provide predictable pension, although with limitations

- For top-net-worth people: Life insurance coverage pension plans can present structured, assured annuities together with legacy planning advantages

Finally, there isn’t any “one-size-fits-all” resolution. The right combination is dependent upon your age, threat urge for food, earnings stability, and retirement targets. The sooner you intend and diversify throughout these choices, the safer and stress-free your retirement could be.

Proceed studying:

(Publish first printed on : 24-April-2026)