{kind=link}

Financial institution Failures in the US, 1863–2024

Financial institution Failures: The Concept

Financial institution failures can stem from two associated however distinct sources. Below the liquidity view, a sudden wave of withdrawals forces a financial institution to liquidate belongings at fire-sale reductions, rendering it bancrupt. Runs can thus set off the failure of in any other case wholesome banks (Diamond and Dybvig, 1983) or of weak however nonetheless solvent banks (Goldstein and Pauzner, 2005).

Below the solvency view, losses on loans or investments erode a financial institution’s fairness. As soon as financial institution belongings will not be value sufficient to completely repay depositors, the financial institution is basically bancrupt. A run might then be the ultimate set off that forces closure. The run can decide when and the way the financial institution fails, however it isn’t the basis reason for the issue.

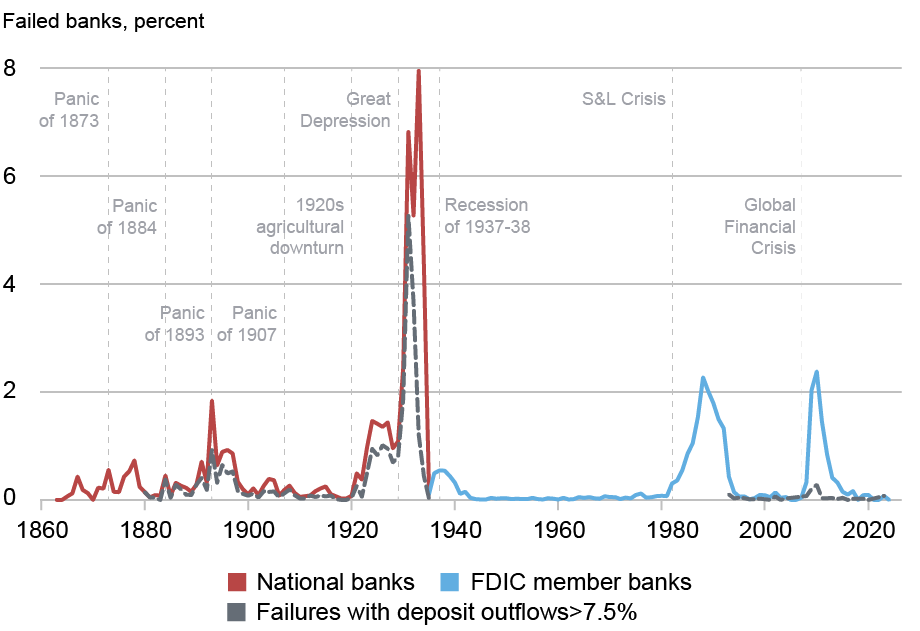

Financial institution Failures: The Proof

Discovering 1: Financial institution failures are at all times and in all places associated to weak financial institution fundamentals.

The talk over whether or not financial institution failures are attributable to insolvency or illiquidity has an extended historical past. In A Financial Historical past of the US, Friedman and Schwartz (1963) argued that many financial institution failures throughout the Nice Despair resulted from “self-justifying” runs on solvent banks. Nonetheless, subsequent empirical work has positioned extra emphasis on poor financial and bank-level fundamentals. Research utilizing regional and bank-level information discover that banks that failed throughout the Despair had been extra uncovered to declining native financial circumstances, had been much less nicely capitalized, held extra illiquid belongings, and relied extra on wholesale funding than surviving banks (White 1984, Calomiris and Mason 2003).

The essential function of poor financial institution fundamentals extends nicely past the Nice Despair. In a current paper, we lengthen these findings throughout 160 years of U.S. banking information, overlaying over 5,000 financial institution failures (Correia, Luck, and Verner, 2026b). Failing banks constantly exhibit declining revenue and capitalization, rising asset losses, and rising reliance on costly funding within the years earlier than failure. A typical precursor to failure is fast asset progress, often from aggressive lending. These patterns maintain for financial institution failures with and with out runs. In addition they maintain throughout institutional regimes with and with out deposit insurance coverage or a public lender of final resort. Consequently, financial institution failures are considerably predictable based mostly on weak financial institution fundamentals. Extra broadly, crises by which many banks fail are sometimes a predictable consequence of deteriorating fundamentals.

Discovering 2: Restoration charges recommend most, however not all, failed banks topic to runs had been basically bancrupt.

Are most failures attributable to runs on weak-but-solvent banks or on basically bancrupt financial institution? Restoration charges on failed financial institution belongings present new insights into this query. Earlier than the introduction of federal deposit insurance coverage in 1934, general collectors recovered, on common, solely 75 cents on the greenback, whereas unsecured depositors recovered solely 66 cents on the greenback (Correia, Luck, and Verner 2026a, 2026b). Because of this failed financial institution belongings fell considerably wanting overlaying debt claims, indicating that almost all failed banks had been basically bancrupt. Runs on weak-but-solvent banks due to this fact accounted for under a modest share of nationwide financial institution failures, until one assumes that receivership itself destroyed substantial worth. Whereas runs had been an essential set off of failure at bancrupt banks, low restoration charges recommend they had been much less typically the reason for failure for in any other case solvent banks.

Discovering 3: Financial institution examiners emphasize poor asset high quality and barely attribute failures to runs.

What do financial institution examiners say concerning the situation of failed banks and the causes of financial institution failure? Within the pre-deposit-insurance U.S. banking system, OCC examiners’ assessments point out that almost all failed banks held belongings uncovered to substantial losses. On common, examiners categorised solely 36 p.c of failed financial institution belongings as “good,” whereas 47 p.c had been thought-about “uncertain” and 18 p.c “nugatory.”

Moreover, U.S. financial institution examiners traditionally categorised the reason for loss of life for banks. Within the OCC’s bank-specific cause-of-failure stories, the most typical causes had been poor native financial circumstances, asset losses, and fraud. Runs and liquidity points had been cited in fewer than 20 out of over 2,000 instances.

The Nice Despair is a partial exception. Federal Reserve Board’s classifications of Despair-era suspensions recommend that liquidity points performed a bigger function than in different durations (Richardson 2007). However even then, examiners’ assessments remained pessimistic about asset high quality. As a 1936 Federal Reserve report put it, “In our lengthy, failure-studded historical past of banking, a lot of the establishments which suspended enterprise had been subsequently proved to be bancrupt.”

Discovering 4: Robust banks often survive runs by means of varied mechanisms, together with interbank cooperation, suspension, and examination.

Why don’t runs trigger solvent banks to fail? A part of the reply is that runs are extra widespread at weak banks. However sturdy banks do generally expertise runs (Correia, Luck, and Verner 2026c). These runs hardly ever result in failure as a result of sturdy banks can make use of a number of mechanisms to keep away from pricey failure.

First, in some instances, homeowners would supply money to credibly sign confidence of their financial institution, very similar to how George Bailey stops the run in It’s a Great Life. Second, interbank lending can present wanted liquidity, as banks are sometimes higher knowledgeable a couple of peer’s true situation (Blickle, Brunnermeier, and Luck 2024). Third, within the historic U.S. banking system, clearinghouses acted as quasi-central banks, issuing mortgage certificates to offer liquidity. Lastly, throughout extreme runs, banks would briefly droop convertibility, each to chill panics and to permit examiners to audit their monetary statements and assess solvency. Collectively, these mechanisms scale back the scope for runs to drive wholesome banks into pricey failure.

Coverage Implications

The discovering that almost all financial institution failures stem from solvency issues has essential implications for monetary stability coverage.

Deposit insurance coverage, launched on the federal degree with the creation of the FDIC in 1933, sharply lowered failures with runs. Nonetheless, as a result of pre-FDIC failures had been hardly ever attributable to runs on wholesome banks, deposit insurance coverage has not eradicated waves of financial institution failures altogether. What it did change was the way in which banks fail. Within the absence of depositor self-discipline, financial institution failure is now extra typically the results of supervisory interventions (Correia, Luck, and Verner 2025). This framework reduces the prevalence of doubtless pricey runs, but it surely additionally reduces the ex put up self-discipline that runs impose on bancrupt banks. With out this self-discipline, there may be extra onus on supervisors to establish potential bancrupt banks after which to mitigate the related losses over time.

Lender-of-last-resort coverage can even assist solvent banks survive panics. A pure experiment from the Despair, evaluating the Atlanta Fed’s beneficiant lending with the St. Louis Fed’s extra restrictive strategy, exhibits that liquidity assist can scale back failures (Richardson and Troost, 2009). However liquidity provision can not repair insolvency. Worldwide proof exhibits that even banking misery with out financial institution runs can produce extreme contractions in credit score and output (Baron, Verner, and Xiong, 2021). Likewise, focused liquidity interventions within the twenty first century have by no means resolved financial institution misery on their very own; balance-sheet restructuring was at all times required (Kelly et al., 2025).

If most financial institution failures are finally pushed by insolvency, then increased fairness capital performs a key function in making the banking system extra resilient (Admati and Hellwig 2014). Higher capitalization reduces each the probability of failure and the scope for runs to trigger injury. Efficient supervision additionally performs a central function by guaranteeing that banks acknowledge losses and by figuring out when recapitalization is required. In crises rooted in weak solvency, recapitalization is arguably the simplest strategy to restore confidence within the banking system.

Summing Up

The long-run proof on financial institution failures factors in a single course: Financial institution failures often start with dangerous belongings, weak earnings, and deteriorating solvency. Runs can speed up failure and worsen the injury, however by the point depositors head for the exit, the deeper drawback is often baked into financial institution steadiness sheets. Historical past has proven that guaranteeing banks are funded with enough capital and avoiding reckless lending booms are probably the most dependable methods to forestall failures from reaching that stage.

Sergio Correia is a senior economist on the Federal Reserve Financial institution of Richmond.

Stephan Luck is a monetary analysis advisor within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Emil Verner is the Lemelson Professor of Administration and Monetary Economics and a professor of finance at MIT Sloan Faculty of Administration.