{kind=link}

Smaller is best. A minimum of that’s what many buyers consider in relation to fairness investing in India.

And the information does appear to assist this view. Over the past twenty years, mid and small cap indices have delivered considerably increased returns than Nifty 50. Effectively, at the very least on the floor.

However is it actually that straightforward? Does going smaller at all times imply increased returns? And extra importantly, are you able to deal with the journey?

What Does This Publish Cowl?

On this put up, allow us to examine the efficiency of 8 cap-based indices over the past 21 years (April 1, 2005, to March 31, 2026). I’ve thought-about the Worth index (and never the Whole Returns index) for the evaluation. Have thought-about 250-day 12 months for evaluation on this put up. We are going to take a look at calendar 12 months returns, CAGR, rolling returns, and danger metrics to know how these indices have really behaved.

The 8 cap-based indices thought-about for this evaluation:

- Nifty 50

- Nifty 100

- Nifty 500

- Nifty Massive & Midcap 250

- Nifty Subsequent 50

- Nifty Midcap 150

- Nifty Smallcap 250

- Nifty Microcap 250

Disclaimer: I’ve used Claude AI extensively for this efficiency evaluation. Whereas I’ve finished just a few pattern checks and the findings look high-quality directionally, it could nonetheless include inaccuracies. Please do additional analysis or seek the advice of your funding adviser earlier than performing on the knowledge shared on this put up.

The Fundamentals: How Are These Indices Totally different?

Earlier than we get to the numbers, a fast refresher.

Nifty 50 tracks the 50 largest firms by market capitalization. Nifty 100 extends this to the highest 100. Nifty 500 is a broad market index protecting the highest 500 firms. Nifty Massive & Midcap 250 combines the highest 100 giant caps and the following 150 midcaps. Nifty Subsequent 50 tracks firms ranked 51-100 by market cap. Nifty Midcap 150 covers firms ranked 101-250. Nifty Smallcap 250 covers firms ranked 251-500. And Nifty Microcap 250 goes even additional down the market cap spectrum.

Word that as you progress down the market cap ladder, you’re primarily investing in smaller and fewer liquid firms. As an investor, the expectation is that you just get compensated for this extra danger via increased returns. However does the information assist this? Let’s discover out.

Calendar Yr Returns

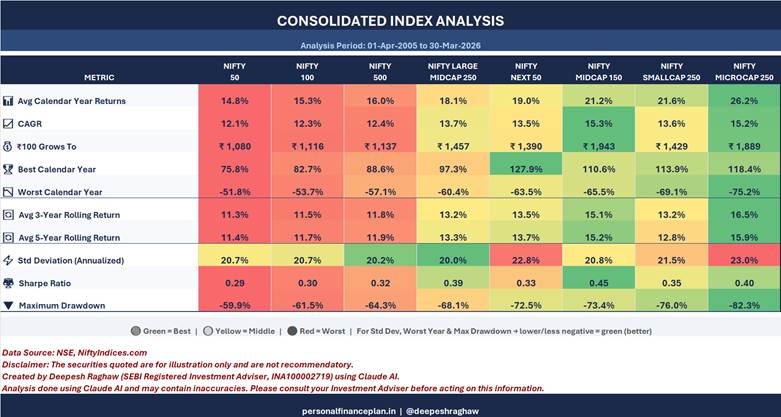

Take a look at the common calendar 12 months returns throughout these 21 years. Nifty 50 delivered 14.8%. Nifty Midcap 150 delivered 21.2%. And Nifty Microcap 250 delivered 26.2%. The sample is evident. Smaller the shares, increased the common returns.

However now take a look at the person years. In 2008, Nifty 50 fell 51.8%. Nifty Smallcap 250 fell 69.1%. Nifty Microcap 250 fell 75.2%. In 2018, Nifty 50 was up 3.2% whereas Nifty Microcap 250 was down 27.7%. And in 2011, Nifty 50 fell 24.6% whereas Nifty Microcap 250 fell 41.6%.

The journey will get considerably rougher as you go smaller, proper?

Within the good years, the smaller indices ship glorious returns. In 2009, Nifty Subsequent 50 delivered 127.9%. Nifty Microcap 250 delivered 118.4%. In 2014, Nifty Microcap 250 was up 103.3%. And in 2007, Nifty Smallcap 250 was up 94.9%.

Good years are high-quality, however in the course of the funding journey, dangerous years matter too.

Consolidated Efficiency: The place the Actual Story Lies

Common Returns vs CAGR: Thoughts the Hole

The typical calendar 12 months return for Nifty Microcap 250 is 26.2%. However the CAGR is just 15.2%. That’s an enormous hole of about 11 proportion factors.

For Nifty 50, the common return is 14.8% and the CAGR is 12.1%. The hole is just about 2.7 proportion factors.

Why does this occur? Due to volatility drag. The extra unstable the returns, the bigger the hole between common returns and CAGR. Therefore, whereas the common returns for smaller indices look spectacular, the precise wealth creation (captured by CAGR) is just not as dramatic because it seems.

Rs 100 Grows To…

In the event you had invested Rs 100 in April 2005, right here’s what it might have turn into by March 2026:

- Nifty 50: Rs 1,080

- Nifty Midcap 150: Rs 1,943

- Nifty Smallcap 250: Rs 1,429

- Nifty Microcap 250: Rs 1,889

Nifty Midcap 150 really created extra wealth than Nifty Microcap 250. Sounds a bit unusual. Doesn’t it? Regardless of Microcap 250 having increased common returns. That is the volatility drag at work.

Danger: The Uncomfortable Fact

Nifty 50 has a typical deviation of 20.7% and a most drawdown of -59.9%.

Nifty Microcap 250 has a typical deviation of 23% and a most drawdown of -82.3%. An 82% fall means your Rs 1 lac turns into Rs 17,700. And you then want a 449% rise simply to get again to the place you began.

Now to the Sharpe ratio (danger adjusted returns). Increased the higher.

Nifty Midcap 150 has the very best Sharpe ratio at 0.45. Nifty 50 has the bottom at 0.29.

Nifty Small Cap 250 at 0.35. Nifty Microcap 250 sits at 0.40, decrease than Midcap 150.

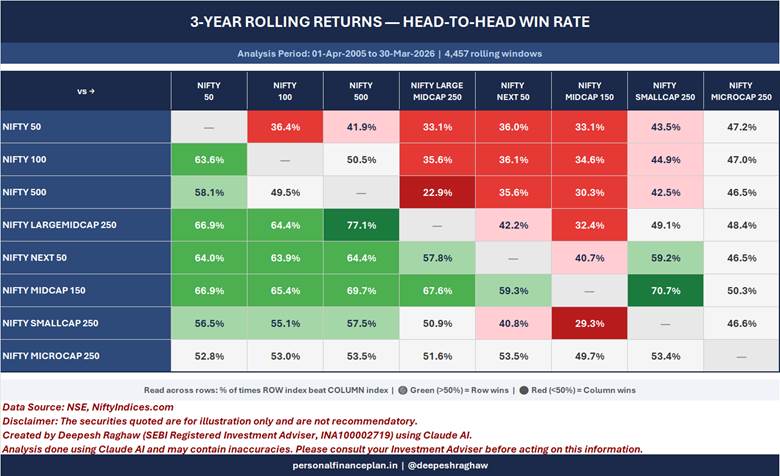

Rolling Returns: Consistency Issues

Rolling returns offer you a way of consistency.

To me, the shock half is that Nifty Small Cap 250 shedding out to Nifty Midcap 150 over 80% of the time in 5-year rolling returns. 70% in 3-year rolling returns.

You’d have anticipated Nifty Small Cap 250 to beat Nifty Midcap 150 over the long-term. In any case, it has even smaller shares. It does appear to outperform point-to-point over 21 years, in the event you take a look at simply the common calendar 12 months returns. Nonetheless, while you take a look at the CAGR, rolling returns and so forth., the small cap index falls behind fairly a bit.

And that’s not it. On 5-year rolling returns, Nifty Smallcap 250 beat Nifty 50 solely about 48.9% of the time. Lower than half. So, regardless of the upper common returns, in the event you had invested in Nifty Smallcap 250 for any random 5-year interval, there was an excellent probability Nifty 50 would have finished higher.

How do you utilize this info?

- Don’t belief the information blindly. There could also be errors in my evaluation.

- The intent of this put up is NOT to show superiority of 1 index over one other. And also you also needs to NOT overview this evaluation on this context. You don’t must be the perfect to be comfortable.

- Don’t simply deal with the returns. I’ve proven long-term knowledge. Therefore, for among the indices, the long-term knowledge could look very spectacular. Firstly, previous efficiency doesn’t assure future efficiency. Secondly, the long-term knowledge normally seems to be fairly clean. It can conveniently cover the unstable journey {that a} specific index would have taken you thru. Or reasonably you are inclined to ignore these features and focus merely on the returns. Lengthy-term, for many buyers, is only a sequence of short-term investments. Therefore, earlier than contemplating any of the indices chosen for this put up, you need to look past the returns knowledge as effectively.

- Conviction in an funding technique is essential. No funding technique, regardless of how good, works on a regular basis. No funding technique, regardless of how dangerous, fails on a regular basis. The ups and downs will take a look at your endurance. In the event you lack conviction, you’ll principally doubtless leap the ship on the improper time.

- Concentrate on constructing a low-cost diversified long-term portfolio.

The Caveats

- Previous efficiency (or outperformance) doesn’t assure future efficiency (outperformance).

- Whereas I’ve thought-about the information from April 1 2005, many of those indices had been launched a lot later. Therefore, the outperformance by these issue indices could merely be a results of back-fitting. I wrote a put up in early 2025 the place I in contrast the efficiency of issue indices since launch.

- I’ve proven returns for indices. You don’t put money into indices. You put money into index funds or ETFs. Such merchandise may have monitoring distinction for numerous causes and can decrease your returns. The monitoring distinction could improve if the underlying shares are much less liquid.

Supply

Disclaimer: Registration granted by SEBI, membership of BASL, and certification from NISM on no account assure efficiency of the middleman or present any assurance of returns to buyers. Funding in securities market is topic to market dangers. Learn all of the associated paperwork rigorously earlier than investing.

This put up is for schooling goal alone and is NOT funding recommendation. This isn’t a advice to speculate or NOT put money into any product. The securities, devices, or indices quoted are for illustration solely and should not recommendatory. My views could also be biased, and I’ll select to not deal with features that you just contemplate essential. Your monetary objectives could also be completely different. You will have a unique danger profile. Chances are you’ll be in a unique life stage than I’m in. Therefore, you need to NOT base your funding choices based mostly on my writings. There is no such thing as a one-size-fits-all answer in investments. What could also be an excellent funding for sure buyers could NOT be good for others. And vice versa. Subsequently, learn and perceive the product phrases and circumstances and contemplate your danger profile, necessities, and suitability earlier than investing in any funding product or following an funding strategy.