The previous couple of days are tremendous busy with 8 (or extra ?) of my firms reporting 2025 numbers. That’s why I do solely the primary 4 proper now, the others (Jensen, SFS, Bois Sauvage and Italmobiliare) will observe quickly.

EVS Broadcast 2025 preliminary outcomes

EVS launched preliminary numbers final Friday. At first sight, they had been just a little little bit of a “combined bag”. Income was up which is sweet for an “odd” 12 months, EPS barely down.

EVS defined that that they’ve invested into individuals to penetrate particularly the US market. The second half of the 12 months was actually good, the primary 6 months had been weaker, primarily due to the “Tarif tantrum” from Uncle Donald.

The outlook for 2026 was fairly good:

Within the name, the CFO talked about that for 2026 they don’t plan huge extra investments into workers and that extra M&A could possibly be attainable.

In response to TIKR, analysts count on EPS of three,36 for 2026. Thus far, the event is roughly inside the initially anticipated case from 2024. Figuring out EVS, there’s additionally a great likelihood that they’ll revise 2026 numbers upwards throughout the 12 months.

The 1,20 EUR dividend will compensate for ready just a little bit longer though Belgian withholding tax isn’t good.

Thermador 2025 preliminary outcomes

Thermador adopted this week with 2025 outcomes. As to be anticipated, gross sales had been barely damaging y-oyy as building and modernization continues to be weak in France:

What I discover very shocking is how properly the consequence saved up:

They managed to cut back working capital in order that they have an honest internet money place which ought to enable them once more some M&A. And possibly, possibly the sector appears just a little bit higher in 2026. Analysts are fairly constructive. Thermador itself mentions a few Authorities packages which could possibly be constructive for them.

Thermador is a “maintain” for me for the time being. Nothing to vary right here.

Eurokai preliminary outcomes 20025

Eurokai additionally got here out with an “Estimate” of the 2025 consequence. Sometimes for Eurokai, the consequence for 2025 can be considerably higher than the revised estimates throughout the 12 months.

They estimate now that 2025 Earnings can be above the 2024 earnings of 88 mn EUR (which included a 19 mn Non-cash constructive one off).

Relying on what allocation the Golden share will get at Holdco stage, this may end in an EPS of as much as 6 EUR . Which signifies that regardless of the numerous enhance within the share worth, Eurokai continues to be very low-cost.

Traders ought to put together as soon as once more for a really cautious outlook for 2026, though in my view, there are a number of components which point out that 2026 could possibly be as soon as once more higher than 2025, even earlier than any “juicy” one-off earnings from partial gross sales to Container shippers.

The share worth is now slowly approaching the historic ATHs from 2006/2007.

Eurokai is now by far my largest place however I depart that one untouched.

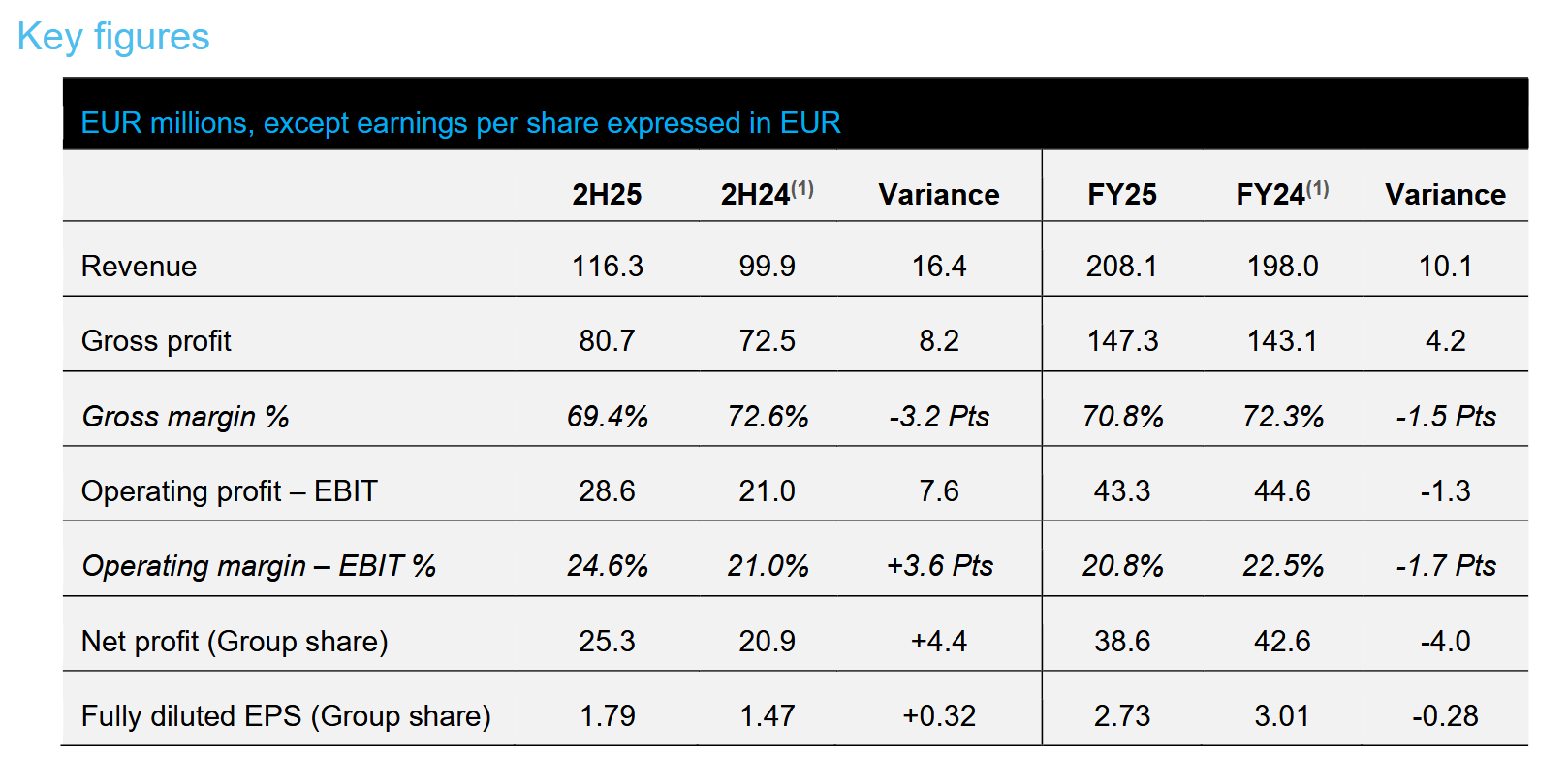

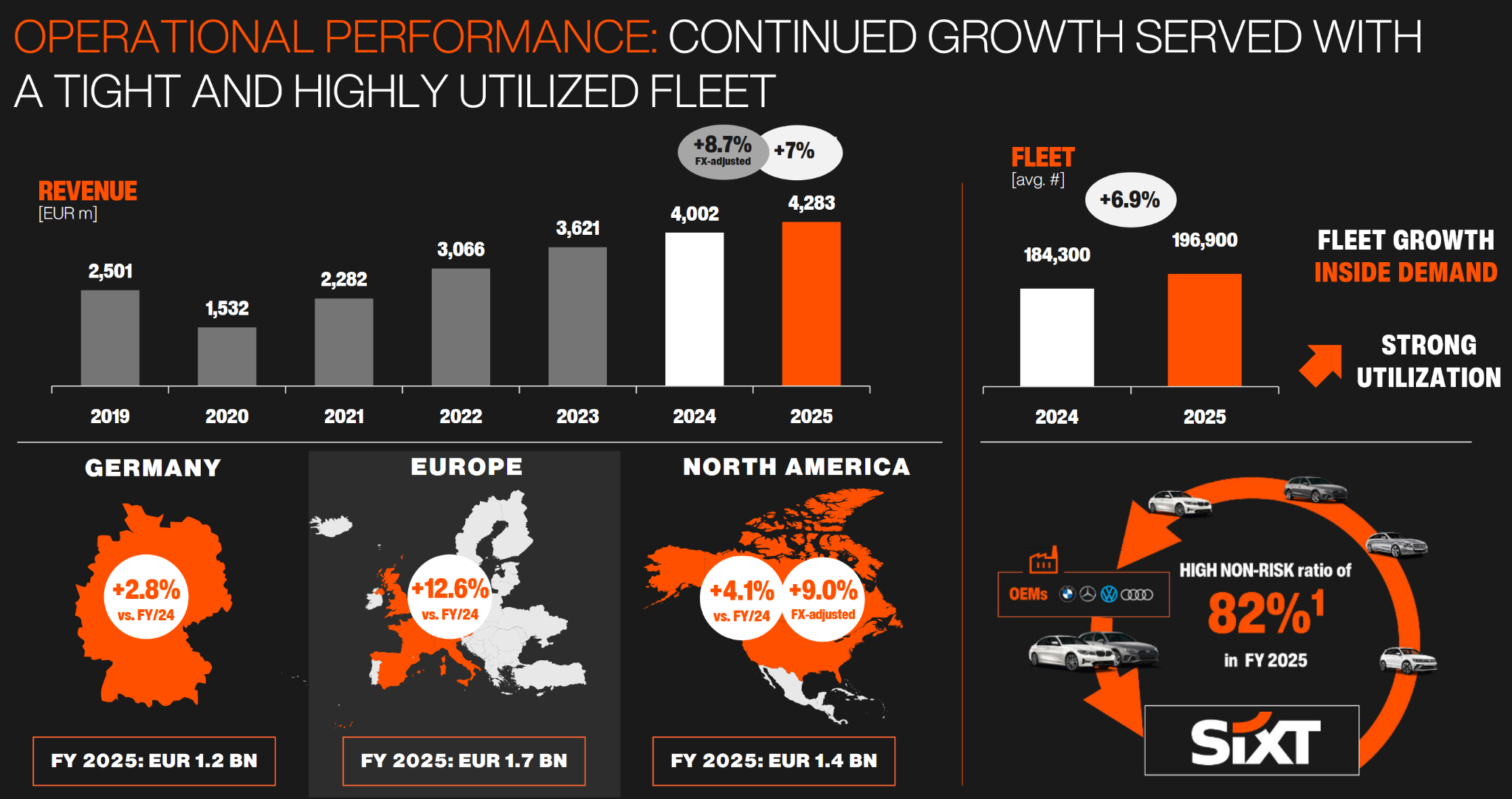

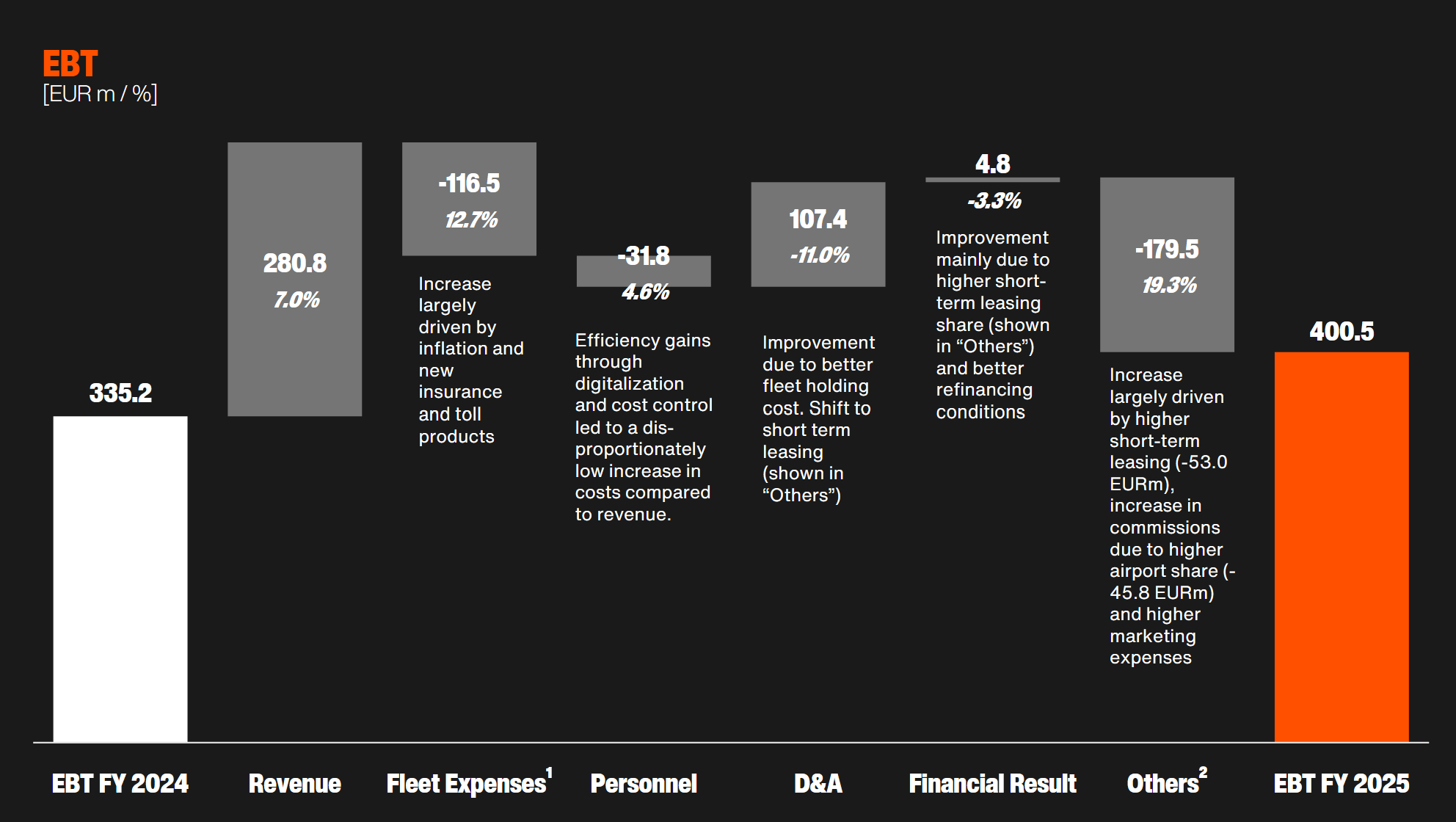

Sixt Preliminary outcomes 2025

Sixt was the fourth firm that week that launched 2025 outcomes. Though the outcomes ended as much as be just a little bit beneath the forecast from Q3, it clearly appears that analysts have anticipated worse as Avis and Hertz each confirmed big losses and declining revenues.

Sixt in distinction managed to develop additionally within the US:

And a big enhance in Income:

What analysts appeared to have actually appreciated was a fairly optimistic outlook for 2026:

That appears to have stunned analysts and led to a “decoupling” of the share worth from these of the weaker US opponents:

{kind=link}

With a trailing P/E of 9 and a dividend yield of 5,8%, the pref shares are actually “good worth” in my view.

To be continued quickly….