{kind=link}

Once you make investments your hard-earned cash, there’s one query that usually will get neglected: “Will I be capable of withdraw my cash once I want it?”

Many traders focus solely on returns and overlook an equally vital issue—liquidity, or how simply you possibly can entry your cash. However the actuality is, some investments lock your cash in for years, and exiting early may be troublesome, costly, or typically not attainable in any respect.

Let’s make sense of lock-in intervals and withdrawal guidelines throughout widespread funding choices in India.

What’s a Lock-in Interval?

A lock-in interval is the minimal time it is advisable keep invested earlier than you possibly can withdraw your cash.

Early withdrawal is probably not allowed, and in some instances, it could additionally entice a heavy penalty. However, in case you keep invested for the complete lock-in interval, you possibly can benefit from the full advantages.

In easy phrases, consider it as a “no exit” rule for a hard and fast interval.

Why Lock-in Interval Issues

Ignoring lock-in guidelines can create money circulate issues throughout emergencies, result in penalties or decrease returns, and even power you to remain invested in merchandise you not need. That’s why liquidity is simply as vital as returns when selecting an funding.

In style Investments | Lock-in Durations & Their Exit Guidelines

Earlier than you commit your hard-earned money, it is advisable know precisely when you will get it again. Here’s a breakdown of the lock-in and exit guidelines for India’s hottest funding choices;

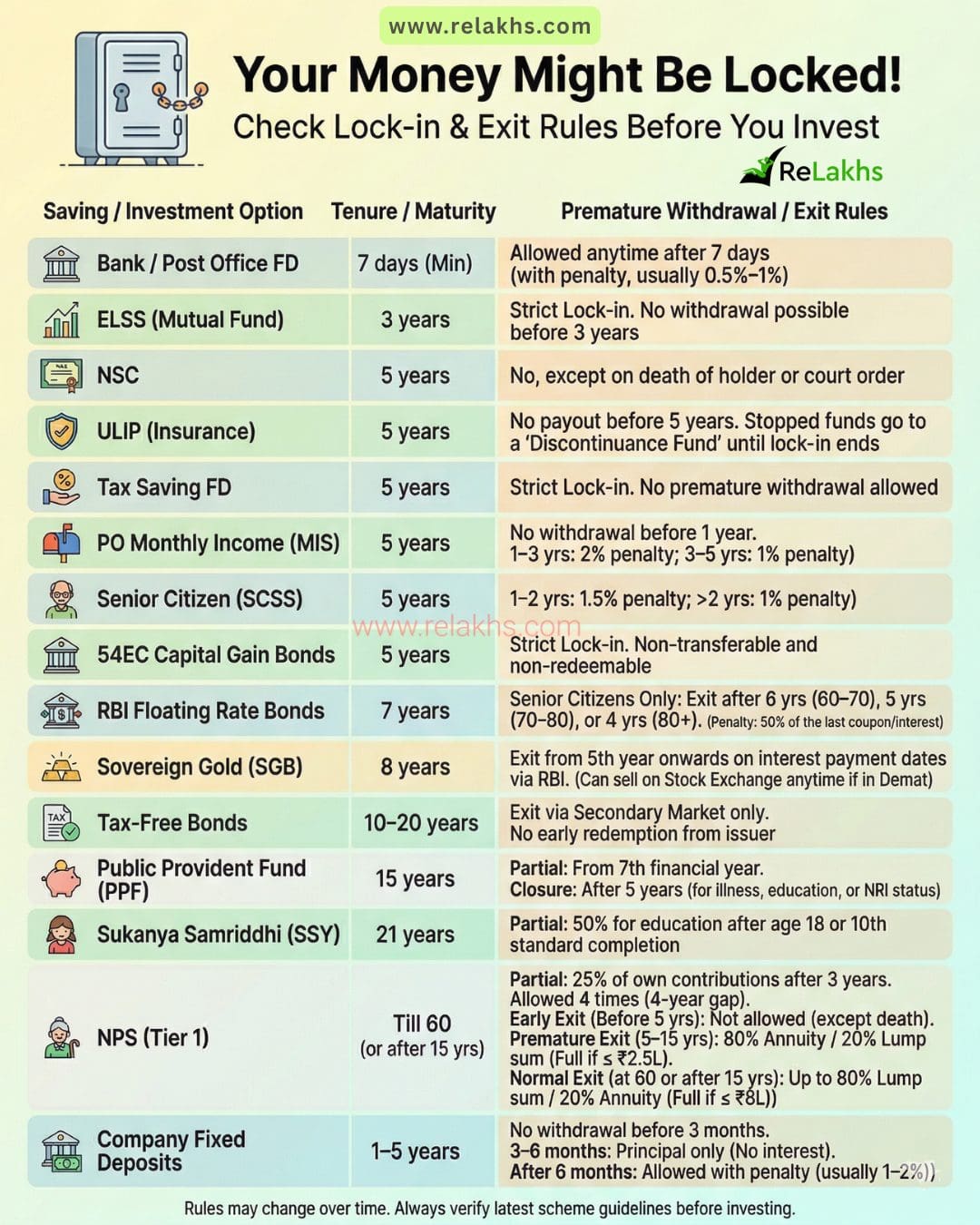

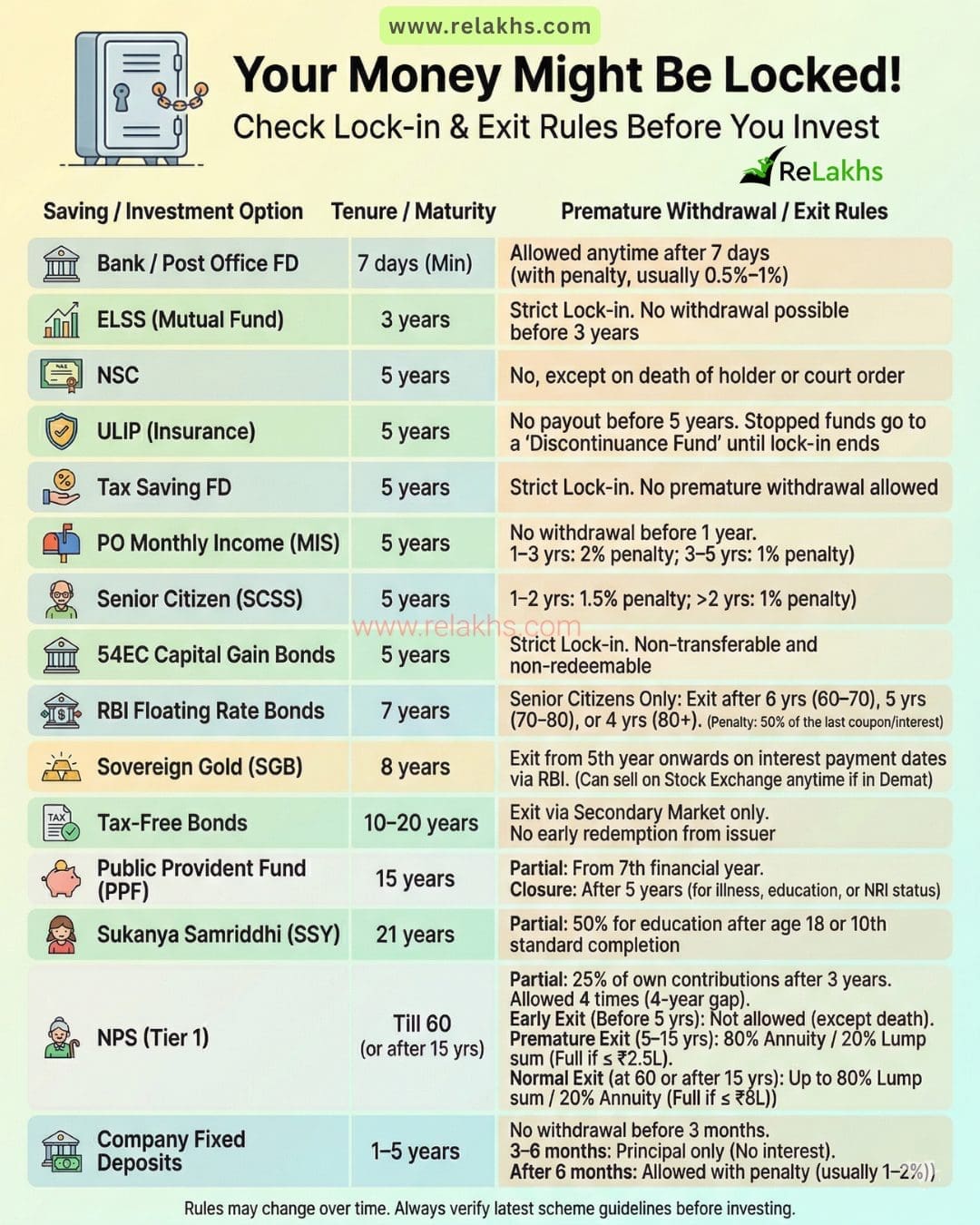

Mounted Deposits (Financial institution / Publish Workplace)

Lock-in is usually a minimal of seven days. You may withdraw earlier than the interval ends, however a penalty will apply (0.5%–1% penalty on the curiosity). Total, it presents good liquidity.

ELSS (Tax Saving Mutual Funds)

ELSS funds include a 3-year lock-in interval, and early withdrawal shouldn’t be allowed. They’re good for combining tax financial savings with long-term wealth creation.

Public Provident Fund (PPF)

PPF comes with a 15-year lock-in interval, although you may make partial withdrawals from the seventh 12 months and shut the account early after 5 years below particular situations. It’s superb for long-term, disciplined financial savings.

Sukanya Samriddhi Yojana (SSY)

The Sukanya Samriddhi Scheme has a tenure of as much as 21 years, with partial withdrawal (as much as 50%) allowed after the woman youngster turns 18. It’s an ideal goal-based financial savings choice on your woman youngster’s future.

Senior Citizen Financial savings Scheme (SCSS)

SCSS has a 5-year lock-in interval, with no exit allowed earlier than 1 12 months, and early withdrawal thereafter comes with a penalty. It prices you: a 1.5% penalty in case you depart inside 2 years, and 1% after that. It’s a super selection for retirees looking for regular revenue.

Publish Workplace Month-to-month Earnings Scheme (PO MIS)

POMIS has a 5-year tenure, however untimely withdrawal comes with guidelines: no exit earlier than 1 12 months, a 2% penalty if withdrawn between 1–3 years, and 1% penalty between 3–5 years. Good for normal month-to-month revenue seekers, retirees, or low-risk traders—however it’s not very liquid within the first 12 months.

Kisan Vikas Patra (KVP)

KVP has a tenure of ~115 months (round 9 years 7 months), designed to double your funding. Untimely withdrawal isn’t allowed earlier than 2 years 6 months (30 months), however after that, it’s attainable with no main penalty—although your efficient returns shall be decrease. Early exit is just permitted in distinctive instances like a court docket order or the holder’s loss of life.

Nationwide Financial savings Certificates (NSC)

NSC comes with a 5-year lock-in interval, and untimely withdrawal shouldn’t be allowed besides in uncommon instances. A protected, fixed-return choice for medium-term targets.

Tax Saving Mounted Deposits

Tax-saving FDs have a strict 5-year lock-in interval, and untimely withdrawal shouldn’t be allowed. A safe choice for many who can decide to the complete tenure.

Tax-Free Bonds

Tax-free bonds usually have a protracted 10–20 12 months tenure. The issuer received’t allow you to exit early, so your solely choice is to promote them on the secondary market. Nice for regular tax-free revenue, however plan for low liquidity.

54EC Capital Acquire Bonds

These are the last word dedication—with a strict 5-year lock-in interval, and so they’re utterly non-transferable. When you make investments, you’re in it for the lengthy haul!

ULIP (Insurance coverage + Funding)

ULIPs include a 5-year lock-in interval, and you can’t withdraw funds earlier than it ends. With ULIPs, payouts are solely attainable after the 5-year lock-in—any stopped funds go right into a Discontinuance Fund. Many suppose ULIPs are versatile—they’re usually not!

Sovereign Gold Bonds (SGB)

SGBs have an 8-year tenure, although you possibly can exit after 5 years on particular curiosity fee dates. You may exit by way of the RBI after the fifth 12 months, or promote them on the Inventory Trade anytime in case you maintain them in a Demat account. A wise technique to spend money on gold with some flexibility inbuilt.

RBI Floating Fee Bonds

RBI Floating Fee Bonds have a 7-year lock-in interval, with early exit allowed just for senior residents (with a penalty of fifty% of the final curiosity fee) below particular situations. A secure choice for these snug with the longer tenure.

NPS (Tier 1) – Up to date Guidelines

NPS Tier 1 has a lock-in till age 60 (extendable as much as 85), however it’s now extra versatile: partial withdrawals are allowed after 3 years, untimely exit is feasible after 5 years (with annuity guidelines), and at retirement, you possibly can take as much as 80% as a lump sum.

Firm Mounted Deposits

Firm FDs usually have a minimal 3-month lock-in interval, with no withdrawal allowed earlier than that. In the event you exit between 3–6 months, you may solely get your principal again with zero curiosity. Appropriate in case you’re okay with barely greater returns however decrease liquidity.

Remaining Ideas

A superb funding isn’t nearly excessive returns—it’s additionally about entry, flexibility, and ideal timing.

- Earlier than you make investments, all the time double-check these:

- Lock-in interval

- Exit guidelines

- Penalties concerned

- Whether or not it matches your monetary targets

As a result of typically, the most important threat isn’t dropping cash…it’s not having the ability to entry it once you want it most.

Earlier than investing in any product, comply with this straightforward rule: “No readability on exit = No funding”

Proceed studying:

(publish first printed on : 07-April-2026)