As promised final week, half 2 of the updates from the very busy week in the past. Let’s go.

Jensen Group

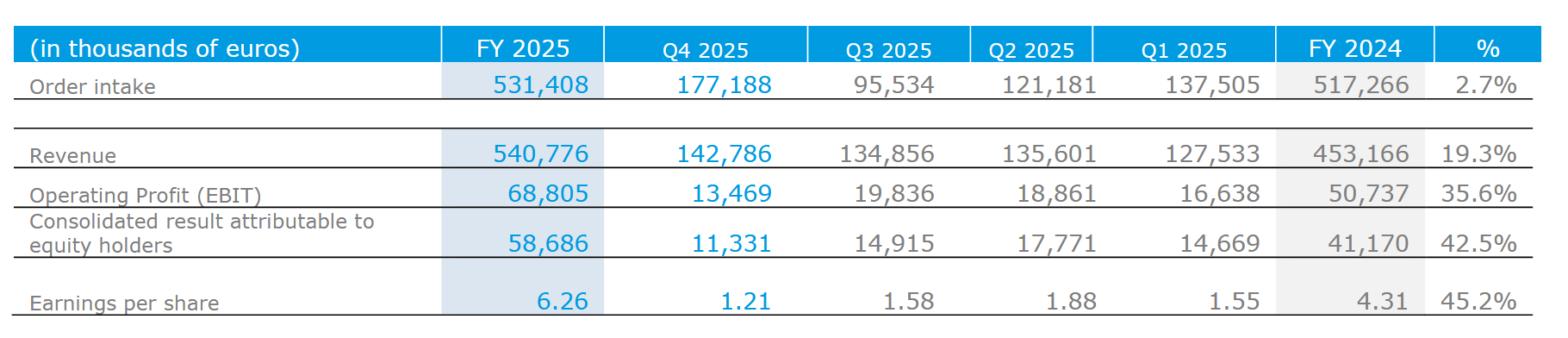

Let’s begin with a particularly constructive one. Jensen Group had a “blowout 12 months” in 2025.

Gross sales up 19,3%, EPS up +45%. The Dividend might be 1,50 EUR, up 0,50 EUR from the 12 months earlier than. The one not extraordinarily constructive quantity was order consumption which was solely barely up. I feel it could be silly to suppose that Jensen can develop 20% gross sales yearly, however Administration sounded fairly assured for 2026 as properly:

At a trailing PE of 11, the inventory is now precisely as low cost (LTM) as once I revealed the preliminary evaluation in January 2025, regardless of a 50% plus share value improve.

I’ve added just a little (0,4% of portfolio) to my place at Friday’s value as I feel the inventory continues to be approach too low cost given the standard. I ought to have waited till right now, however such is life.

SFS

SFS, the Swiss components and instruments producer/distributor additionally revealed preliminary outcomes final week. Given the troublesome state of lots of its finish markets, natural development of ~3% earlier than FX is kind of spectacular.

Sadly, revenue suffered just a little extra as we are able to see on this desk (earlier than “normalisation”):

To be sincere, SFS is kind of behind towards my expectations from 3 years in the past, even factoring in CHF/EUR growth.

I feel again in 2023, I used to be too optimistic about manufacturing in Europe which actually is struggling:

The inventory is now rather more costly regardless of EPS being decrease. So I really want to consider whether or not I ought to proceed to carry the inventory.

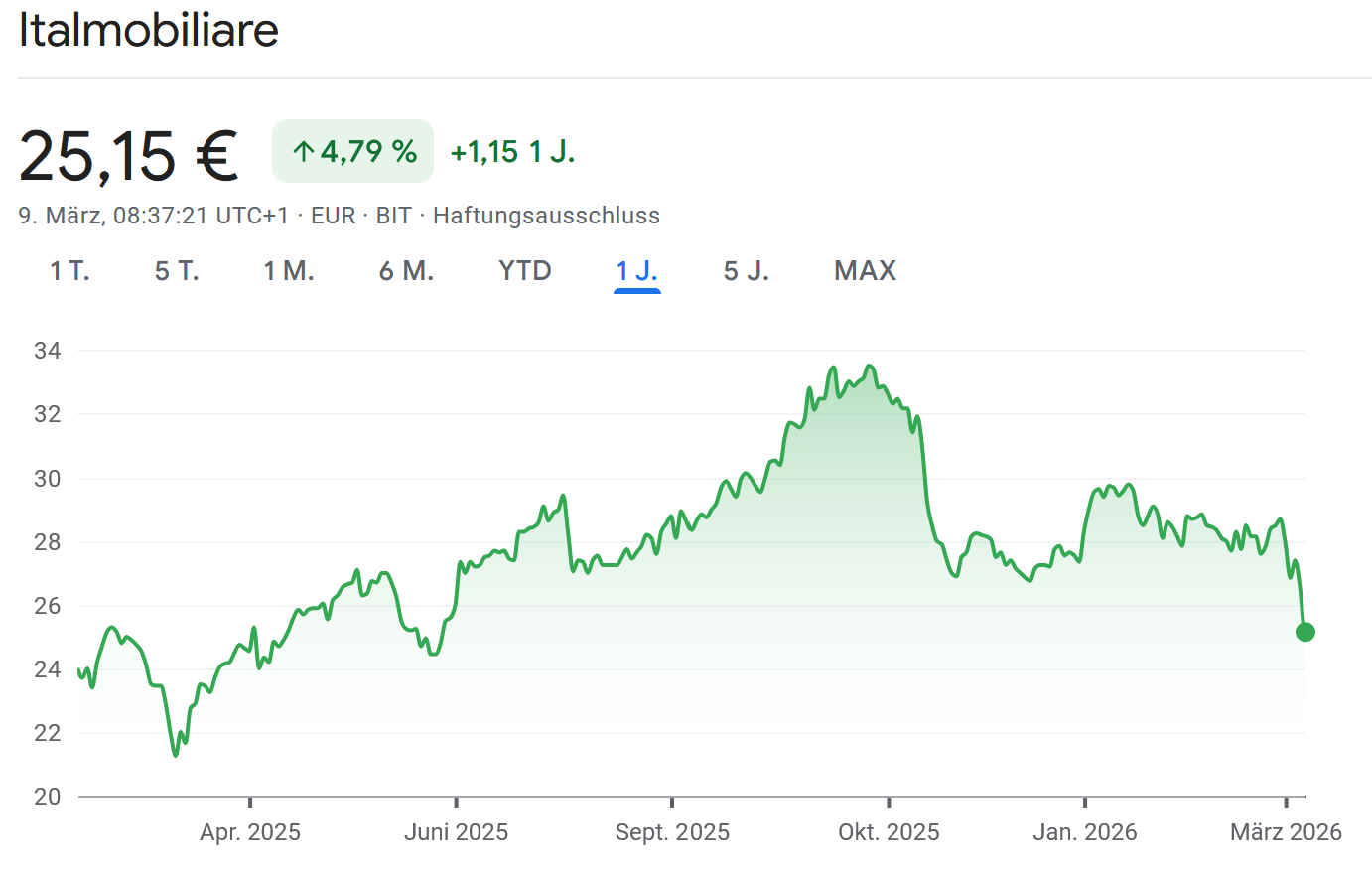

Italmobiliare

Italmobiliare’s preliminary 2025 numbers have been a “combined bag”. NAV elevated (incl. dividends) by 6%, however for the 2 largest stakes, Borbone (Ebitda down due to excessive Espresso costs) and Santa Maria Novella (solely single digit development), the outcomes have been just a little bit disappointing.

On the plus facet, they managed to amass an extra 5% stake in Bene and Casa de Salute grows properly.

The inventory reacted fairly negatively which result in a rise in low cost to NAV.

At the least for Borbone, issues ought to look rather a lot higher in 2026 as Espresso costs have come down once more:

It is going to be attention-grabbing to see if SMN can develop double digit once more.

Cie Bois Sauvage

Lastly, my “particular scenario” Cie Bois Sauvage introduced preliminary 2025 earnings and the results of their “strategic evaluation”.

On the plus facet, the NAV elevated by 10% in 2025, primarily pushed by the Chocolate enterprise:

{kind=link}

Additionally constructive is that they may purchase the remaining 34% of Jeff De Brugges, their second Chocolate Model.

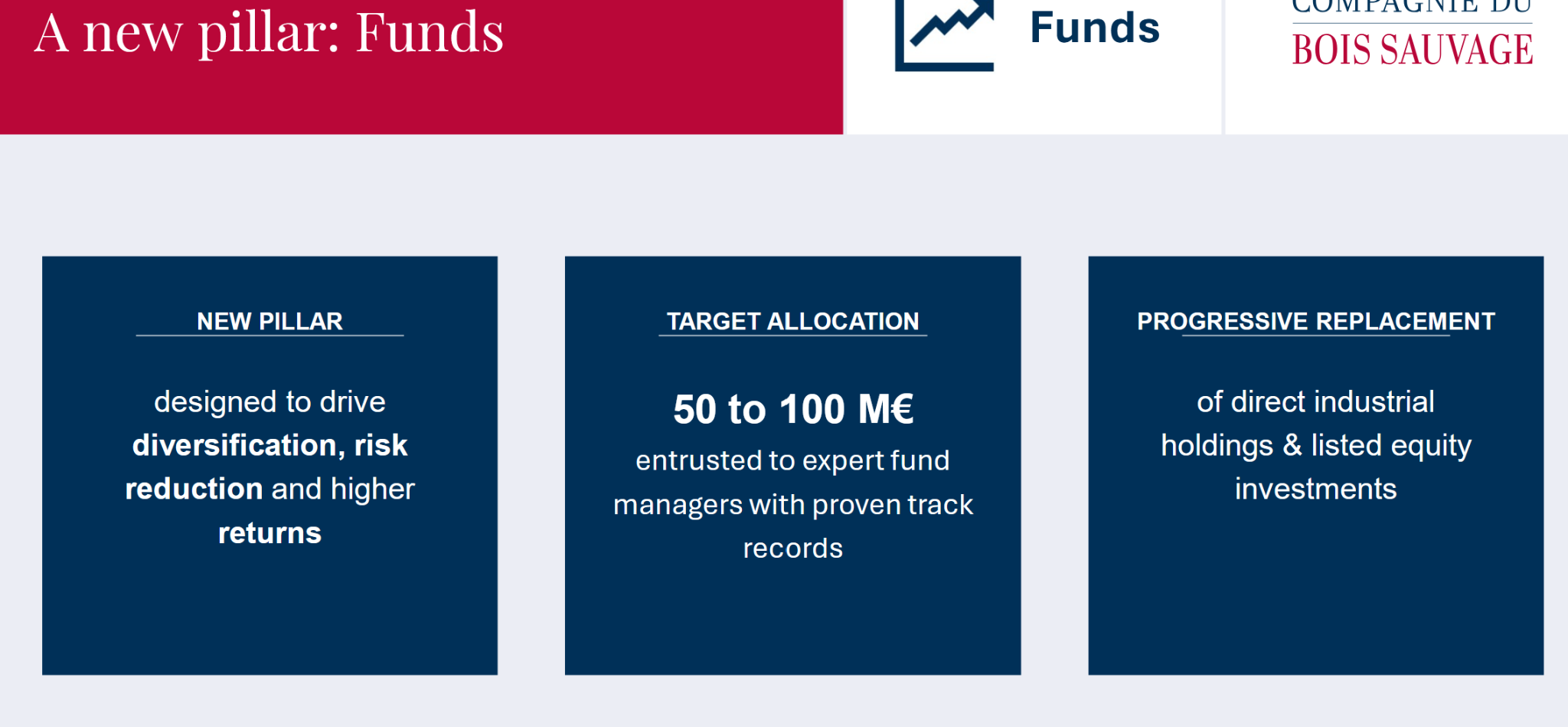

Much less constructive was the disappointing growth of the Actual property pillar (NAV -10%) and the choice to discontinue industrial participations and make investments into PE funds as a substitute:

That is actually a downer for my part. As a lot as I just like the Chocolate enterprise, I don’t perceive this “new pillar”. As I discussed within the preliminary publish, this was meant to be a brief time period particular scenario. Subsequently I made a decision to exit the inventory at present costs (318 EUR). This was an honest Brief time period particular scenario with a 20% plus return in 3 months.