{kind=link}

Many trendy banking organizations are extremely advanced. A “financial institution” is usually a bigger construction made up of distinct entities, every topic to completely different regulatory, supervisory, and reporting necessities. For researchers and policymakers, understanding how these establishments are structured and the way they’ve advanced over time is important. On this put up, we illustrate what a contemporary monetary holding firm seems to be like in apply, doc how banks’ organizational constructions have modified over time, and clarify why these particulars matter for conducting correct analyses of the monetary system.

Observe: As of March 2026, the New York Fed will discontinue the Quarterly Developments for Consolidated U.S. Banking Organizations report. As a replacement, workers economists will start producing periodic weblog posts that spotlight evolutions and developments within the banking sector; this marks the primary put up in that collection.

Inside a Monetary Holding Firm

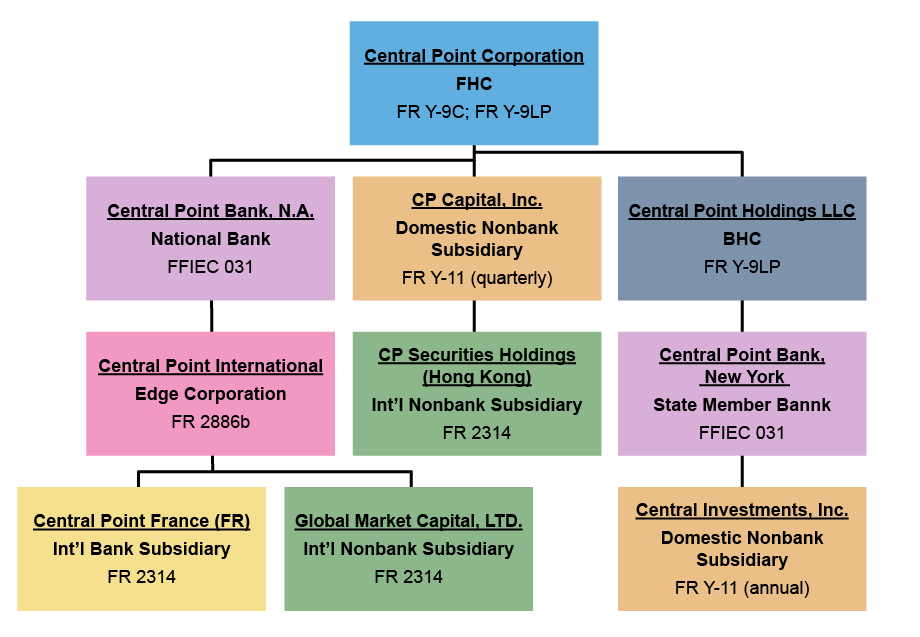

As an example the construction of a holding firm in sensible phrases, we current a stylized instance: the fictional “Central Level Company.”

Central Level Company’s Organizational Hierarchy

Observe: The related regulatory submitting is indicated for every entity sort.

On the prime of the organizational construction is the mum or dad, or top-tier, holding firm. That is Central Level Company (blue field).

The commonest sort of holding firm is a financial institution holding firm (BHC) which is Central Level Holdings LLC (gray field) in our diagram, which information an FR Y-9LP. These are holding firms that personal or management a number of industrial banks or different BHCs. The BHC construction was first established by the Financial institution Holding Firm Act of 1956.

The highest-tier holding firm, Central Level Company, nonetheless, is assessed as a monetary holding firm (FHC), and these submit FR Y-9C and FR Y-9LP filings. Monetary holding firms had been launched as a part of the Gramm-Leach Bliley Act (GLBA) of 1999 as a particular sort of holding firm that may have interaction in a broader vary of monetary actions past conventional banking, resembling insurance coverage and securities underwriting. To qualify as an FHC, an organization should derive a minimum of 85 % of its consolidated gross revenues from monetary actions. As you’ll be able to see from our instance, although, an FHC could itself maintain a BHC.

Holding firms can have many varieties of subsidiaries. A few of these are home industrial banks, resembling nationwide banks and state-chartered member banks (which each file an FFIEC 031). Central Level Company owns a nationwide financial institution (Central Level Financial institution, N.A.) and a state-chartered member financial institution (Central Level Financial institution, New York). Holding firms may also comprise nonbank monetary establishments (NBFIs, which file an FR Y-11 if home, and an FR 2314 if worldwide), companies that have interaction in monetary actions apart from banking. For instance, CP Capital, Inc. and Central Investments, Inc. are NBFIs.

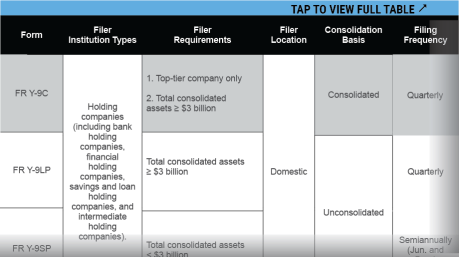

Different subsidiaries could also be international. These subsidiaries could also be positioned in an edge company (which information an FR 2886b) that’s allowed by its constitution to interact in international enterprise. In our instance, Central Level Company owns an edge company (Central Level Worldwide), which in flip holds a international financial institution (Central Level France (FR)) and a international nonbank (World Market Capital Ltd). This organizational construction has direct implications for a way establishments are noticed within the information. Completely different entities inside the similar holding firm are topic to completely different reporting necessities, file completely different regulatory kinds, and should seem (or not seem) in generally used datasets. To help analysis on these establishments, the desk under (full model out there for obtain) summarizes a number of generally used U.S. regulatory kinds and the varieties of entities required to file them. Whereas not exhaustive, it offers a powerful place to begin for navigating the regulatory reporting panorama and figuring out applicable sources for given analysis questions.

Preview: U.S. Regulatory Types and Corresponding Entities

DOWNLOAD FULL TABLE

The Evolution of Monetary Establishments

Banking organizations weren’t all the time as advanced as Central Level, and actually had been beforehand all organized as BHCs. How did banking organizations change over time? And what had been the regulatory developments related to these modifications?

Subsequent, we conduct an evaluation to indicate how the composition of holding firm sorts has advanced over time. Along with FHCs and BHCs, we will even focus on the event of financial savings and mortgage holding firms (SLHCs) and intermediate holding firms (IHCs), which have developed as various holding firm constructions in latest many years. SLHCs personal or management a number of financial savings associations or different SLHCs, whereas IHCs are established by giant international banking organizations to carry all of their U.S. non-branch subsidiaries. All through our evaluation, we’ll describe how these holding firm sorts differ from each other, and the regulatory developments which have inspired their development.

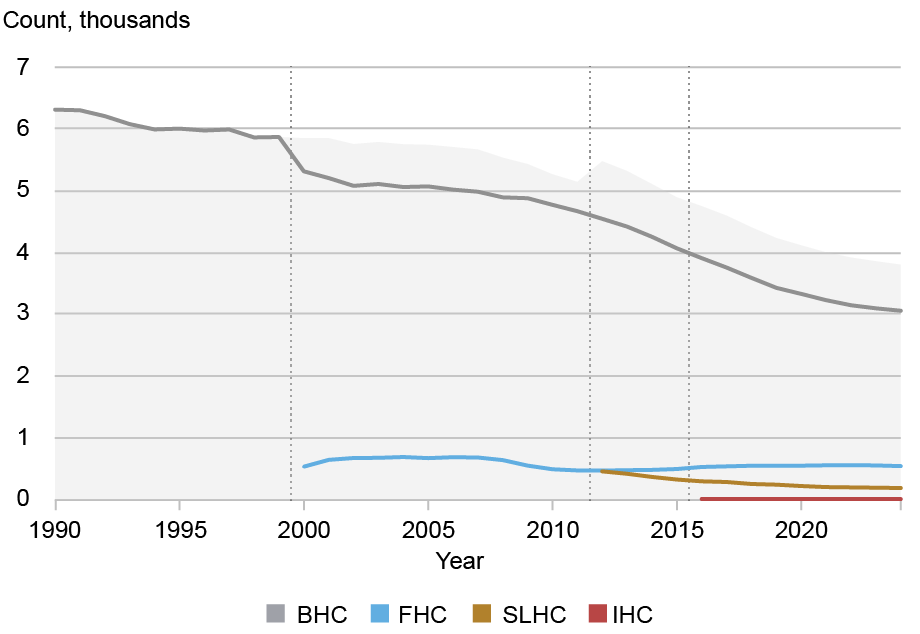

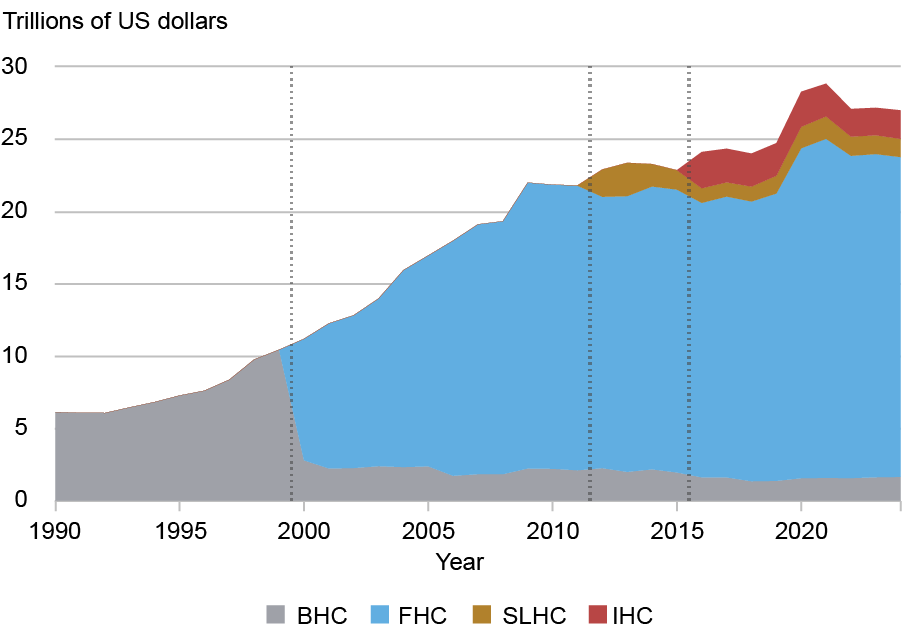

The chart under exhibits each the quantity and share of holding firm sorts (BHCs, FHCs, SLHCs, and IHCs) from 1990 to 2024.

Evolution of U.S. Holding Firm Sorts

Notes: The chart exhibits the evolution of U.S. Holding Firm sorts from 1990 to 2024 on the annual frequency. The highest panel exhibits the depend of establishments by entity sort for financial institution holding firms (BHC, darkish gray), monetary holding firms (FHC, blue), financial savings and mortgage holding firms (SLHC, brown), and intermediate holding firms (IHC, crimson). The sunshine gray shaded space exhibits the whole throughout all holding firm sorts. The underside panel exhibits consolidated belongings of top-tier holding firms that file the FR Y-9C, in trillions of 2024 U.S. {dollars}, utilizing the identical colours for every group. Vertical strains characterize key regulatory milestone: the GLBA of 1999 (creation of FHCs), the 2012 switch of SLHC supervision to the Federal Reserve below Dodd-Frank, and the 2016 implementation of the IHC requirement for sure international banking organizations.

Two patterns stand out. First, the whole variety of holding firms declined considerably from 6,307 in 1990 to three,801 in 2024, reflecting consolidation within the banking sector. Regardless of this decline, BHCs stay essentially the most prevalent holding firm sort, accounting for roughly 80 % of all regulated holding firms.

Second, modifications in holding firm sorts have been intently tied to regulatory developments. The introduction of the FHC following the GLBA of 1999 allowed BHCs to broaden right into a broader vary of monetary actions. Whereas FHCs characterize lower than 20 % of all regulated holding firms, the underside panel of the chart above exhibits that they maintain a disproportionately giant share of whole belongings.

SLHCs have remained comparatively small in depend, falling from 459 in 2012 (after they had been first integrated into the Federal Reserve reporting framework) to 190 in 2024. IHCs are few in quantity (solely 11 as of 2024), however account for a significant quantity of belongings given the dimensions of their mum or dad organizations.

To know shifts within the composition of holding firm sorts, the chart under tracks modifications in holding firms’ designations over time.

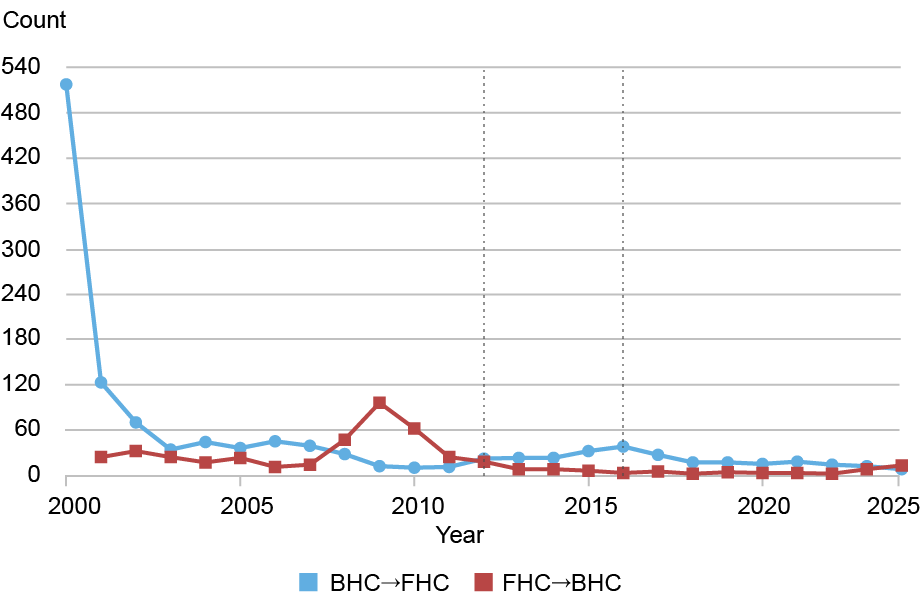

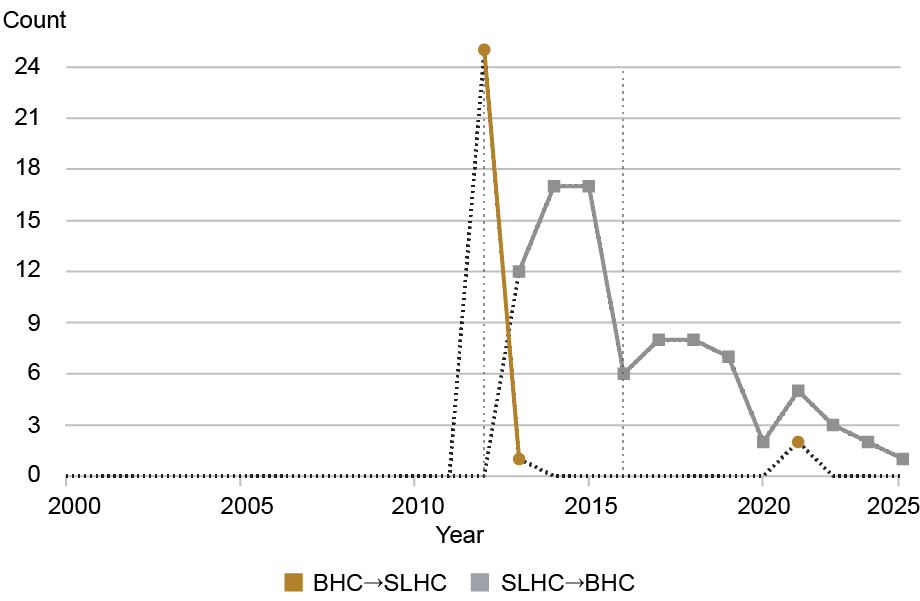

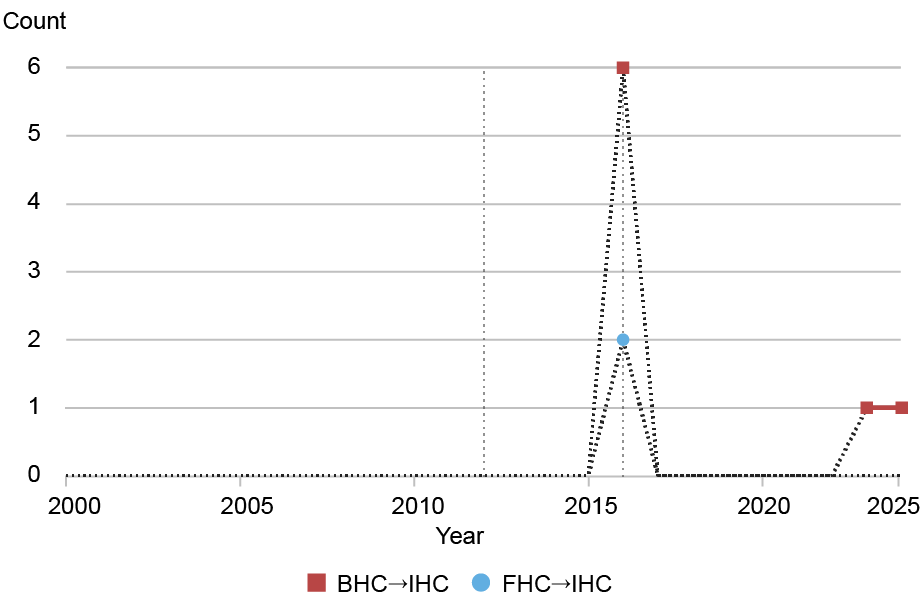

Entity-Kind Switches by Yr

Notes: The chart exhibits the quantity of holding-company-type switches from 2000 to 2024 on the annual frequency. The highest panel studies switches between financial institution holding firms (BHC) and monetary holding firms (FHC). The center panel studies switches between BHCs and financial savings and mortgage holding firms (SLHC). The underside panel studies switches involving intermediate holding firms (IHC), together with switches from BHCs and FHCs. Vertical strains characterize key regulatory milestone: the GLBA of 1999 (creation of FHCs), the 2012 switch of SLHC supervision to the Federal Reserve below Dodd-Frank, and the 2016 implementation of the IHC requirement for sure international banking organizations.

The commonest swap is from BHC to FHC, as proven within the prime panel. 518 conversions occurred instantly upon the passage of the GLBA in 2000. One other 123 companies transformed in 2001, after which the tempo of conversions slowed significantly. After the worldwide monetary disaster (GFC) in 2008, BHC-to-FHC conversions dipped whereas FHC-to-BHC reversions spiked, as establishments switched their charters. One cause for these conversions could also be that Dodd-Frank elevated the regulatory necessities and reporting burdens for giant FHCs, making it comparatively extra expensive to have this construction.

The center panel exhibits switches between BHCs and SLHCs, and the underside panel exhibits conversions into IHCs. Whereas the conversions to SLHCs and IHCs occurred after the introduction of the respective holding firm sorts in 2011 and 2016, these switches are much less frequent than these between BHCs and FHCs. One driving pressure behind the shifts between BHCs and SLHCs is the switch of supervisory authority over SLHCs from the Workplace of Thrift Supervision (OTS) to the Federal Reserve in 2012, which made such switches simpler. The switches from BHCs to IHCs occurred as soon as the IHC construction was first mandated below the 2016 intermediate holding firm rule, which requires any FBO with greater than $50 billion in whole world consolidated belongings and a minimum of $50 billion in U.S. non-branch belongings to ascertain an IHC to accommodate its U.S. subsidiaries.

Why This Issues

The organizational construction of monetary organizations is vital for researchers and different analysts to know, because it shapes each what banks do and what we observe within the information. Ignoring this info can result in mismeasurement, pattern choice errors, and deceptive conclusions.

For instance, think about a researcher making an attempt to know variations between banking and non-banking actions of holding firms utilizing FR Y-9C filings. In our stylized instance, the top-tier entity, Central Level Company, information the FR Y-9C however is designated a monetary holding firm quite than a financial institution holding firm. If the researcher identifies banking actions as solely these associated to BHCs, they might inadvertently underestimate the quantity of banking actions carried out by Central Level Company and different economically related establishments. As a result of these companies are usually the most important and most advanced, such misclassifications can systematically bias outcomes.

As a second instance, think about an analyst monitoring the actions of a single group over time. Suppose Central Level Company initially operated as a BHC and later reclassified itself as an FHC. Such a change would broaden the vary of actions that the group is ready to conduct, thus altering the way it seems in regulatory information. The analyst would possibly observe abrupt modifications in reporting variables that replicate reclassification quite than true modifications in conduct. With out accounting for organizational transitions, these reporting shifts may be misinterpreted as behavioral results. We’d encourage researchers to make use of the Nationwide Data Middle database to verify the construction of holding firms of their information, which may stop the misclassifications described right here.

Summing Up

On this weblog put up, we described the construction of recent monetary establishments with the assistance of a stylized instance, documented how holding firm sorts and designations have advanced, and defined why this data is essential for banking evaluation. Understanding these organizational selections clarifies how establishments match inside the broader regulatory framework and is important for researchers concerned in banking evaluation.

Lily Gordon is a analysis analyst within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Lee Seltzer is a monetary analysis economist within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

How you can cite this put up:

Lily Gordon and Lee Seltzer, “Behind the ATM: Exploring the Construction of Financial institution Holding Firms,” Federal Reserve Financial institution of New York Liberty Road Economics, March 31, 2026, https://doi.org/10.59576/lse.20260331

BibTeX: View |

Disclaimer

The views expressed on this put up are these of the writer(s) and don’t essentially replicate the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the duty of the writer(s).